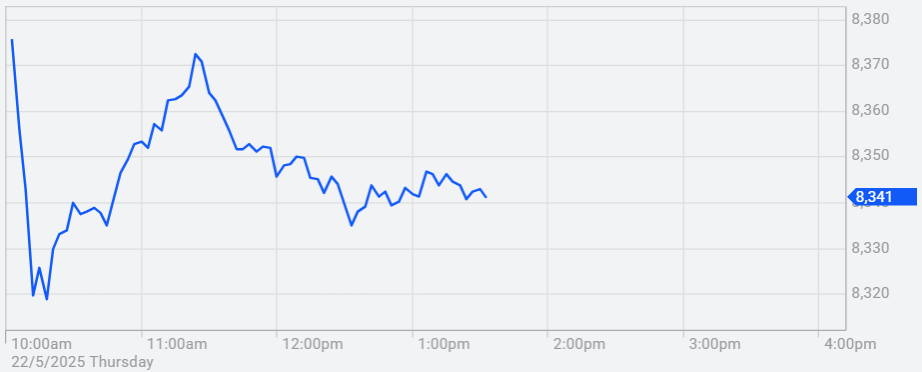

The Australian sharemarket dipped in afternoon trade today, with the S&P/ASX 200 shedding 45.60 points or 0.54% to sit at 8,341.20 as of 1:30 pm AEST. This decline came despite the index reaching a fresh 50-day high earlier in the session. Overall sentiment turned cautious as investors digested weaker sectoral performance and some sharp individual stock losses.

ASX 200 reached a fresh 50-day high earlier in the session and then declined [ASX.com.au]

Sector Weakness Dragging Broader Market

A visual snapshot of sector performance reveals a market painted almost entirely in red. Energy led the declines, dropping by 1.63%, followed closely by Information Technology at -1.42% and A-REITs at -1.23%. Even typically defensive sectors such as Utilities (-0.53%), Consumer Staples (-0.19%), and Health Care (-0.20%) could not escape the downturn.

The only sector to post a noticeable gain was Materials, which rose by 0.42%. This performance aligned with strength in the gold sub-sector, as the ASX All Ordinaries Gold Index (XGD) surged by 2.37% today. The XGD’s performance helped offset some of the broader losses but wasn’t enough to keep the main indices in the green.

Top Performers: Gold Miners Shine Bright

Gold-related stocks dominated the leaderboard, with Lynas Rare Earths Limited (LYC) rising 5.46% to $8.015. Genesis Minerals (GMD), Spartan Resources (SPR), Northern Star Resources (NST), and Ramelius Resources (RMS) also notched gains above 3.5%, buoyed by stronger gold prices and sustained investor interest in the precious metals sector.

Genesis Minerals stood out not only for price appreciation but also in trading activity, with volumes surging 98% above its 90-day average. This suggests renewed investor confidence in the miner’s fundamentals and growth outlook.

Sharp Declines in Key Names

On the downside, Nufarm Limited (NUF) was the worst performer, plunging 8.90% to $2.56 amid a massive 693% surge in trading volume, possibly indicating institutional sell-offs or disappointing market updates. ZIP Co Ltd (ZIP) followed closely, falling 6.62% to $1.867, continuing a rough streak for tech-adjacent financials.

Polynovo (PNV), Boss Energy (BOE), and Healius (HLS) also saw losses between 3.6% and 4.8%, contributing to the drag on the Health Care and Energy sectors.

Index Performance: A Widespread Pullback

The downward movement wasn’t limited to the ASX 200 (XJO), with nearly all major indices experiencing losses:

- ASX 50 (XFL): -0.54%

- ASX 100 (XTO): -0.58%

- All Ordinaries (XAO): -0.56%

- ASX 300 (XKO): -0.53%

- ASX 20 (XTL): -0.67%

- ASX 200 Banks (XBK): -0.97%

- ASX All Technology (XTX): -1.25%

The Banks and Tech sectors remain particularly under pressure, with the All Tech Index’s 1.25% slump reflecting global softness in tech stocks. The Banks index, down 0.97%, suggests investor caution over tightening credit conditions and slower consumer lending growth.

Market Context: Recent Gains at Risk

Despite today’s decline, the ASX 200 remains up 0.53% over the past five sessions and is currently 3.18% off its 52-week high. This indicates that while today’s losses are notable, they come on the back of a relatively strong recent uptrend.

Investor sentiment has been mixed, balancing optimism around strong commodity prices and resilient earnings against concerns of inflation, potential rate hikes, and global market volatility.

Currency Moves Reflect Cautious Optimism

On the forex front, the Australian dollar showed modest strength against several major currencies. As of 1:15 pm AEST:

- AUD/USD rose slightly to 0.6420 (+0.07%)

- AUD/NZD increased to 1.0841 (+0.24%)

- AUD/CNY ticked up to 4.6356 (+0.08%)

However, the Aussie weakened slightly against the yen (-0.25%) and the Swiss franc (-0.09%), reflecting mixed signals in global risk appetite. The slight gains in AUD/USD may suggest confidence in Australia’s macroeconomic resilience, though downside risks remain.

Outlook: Volatility Likely to Persist

Looking ahead, markets may remain choppy as global investors await fresh economic data out of the US and China, including inflation figures and manufacturing indices. Domestically, investors will be closely watching for updates on interest rates, labour market figures, and business sentiment surveys.

While today’s sell-off was broad-based, the resilience of gold and materials stocks highlights selective investor confidence. Resource stocks may continue to act as a hedge against macro uncertainty, especially if commodity prices remain elevated.

Yet, with banks, tech, and real estate sectors struggling, a more broad-based rally will require improvement in global economic sentiment and clarity on central bank policy paths.

Conclusion

The ASX 200’s drop today marks a pause in recent gains and reflects growing caution among investors. With nearly all sectors flashing red, it’s clear the market is navigating a more defensive phase. However, pockets of strength—particularly in gold and materials—show that selective opportunities remain for astute investors.

As the week progresses, attention will remain fixed on global cues and corporate earnings, with traders looking for signals that could either stabilise or further unsettle local markets.