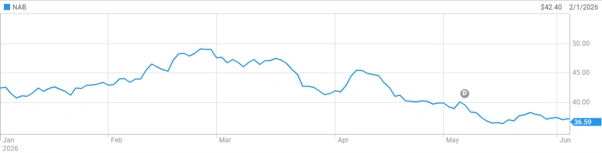

National Australia Bank (ASX: NAB) hit an all-time high of $49.45 on 27th February 2026. By early June, the stock was sitting around $37. That is a fall of roughly 25% in about 100 days, and the reasons behind it are worth unpacking carefully rather than dismissing as routine market noise.

This is not a story about one bad quarter. Several distinct problems arrived at once, and the timing matters.

What Hit the National Australia Bank Share Price in 2026

The first blow landed on 20th April 2026. NAB flagged $2.05 billion in one-off charges and a discounted dividend reinvestment plan that effectively amounts to a capital raise, sending the stock down 3.55% in a single session. Two separate hits combined to produce that number.

NAB’s H1 FY26 credit impairment charges are expected to total $706 million, driven partly by new sector overlays applied to agriculture, transport and storage, and manufacturing. In plain terms, NAB’s internal models now see more risk in those sectors than they did before.

The second hit was less obvious but arguably more significant to long-term earnings quality. A software capitalisation policy change triggered a $1.347 billion pre-tax accelerated amortisation charge in H1 FY26.

NAB changed the way it accounts for technology spending, raising the capitalisation threshold from $5 million to $20 million and shortening useful-life estimates on existing software. The result: $949 million in after-tax charges hit the first-half result directly, rather than being spread over future years.

Management framed it as aligning with a rapidly evolving technology environment. Fair enough. But investors who bought NAB expecting a clean earnings half got a reported statutory profit that fell 18%.

Revenue increased 3.1% for the half, with underlying profit up 6.4% on a cash earnings basis excluding notable items, and cash earnings grew 2.3%. Strip out the big one-offs, and the business is holding up. That context gets lost when headline numbers look alarming.

NAB share price (ASX: NAB), January to June 2026, showing the 25% pullback from the February all-time high. [ASX]

Why Analysts Are Cautious on ASX Bank Stocks Right Now

Morgan Stanley moved to a bearish Underweight rating on NAB from Equal Weight, slashing its price target to $39.80 from $43.50, warning that Australia’s major lenders are “priced for perfection” after a strong run through 2024 and early 2025. JPMorgan followed with its own downgrade, cutting to Neutral.

The Morgan Stanley call is not primarily about NAB’s fundamentals. It is a valuation argument. The bank ran hard into February, the multiple expanded, and now earnings risk has grown. That combination makes it harder to justify the price investors were paying at the peak.

Morgan Stanley shifted its view on Australian banks broadly to Cautious, citing rising risks of earnings downgrades and trading multiple de-ratings following the February reporting season.

For what it is worth, the firm frames the downgrade as primarily a valuation and relative performance call rather than a fundamental concern about business viability or systemic risk, noting capital positions are strong, provisioning levels are conservative, and dividends are likely to be maintained.

That is an important distinction. A bank with a broken balance sheet is a different problem from a bank that ran too far too fast.

The Dividend Question for Income Investors

NAB announced a temporary dividend of 85 cents per share for this half. You had to own the shares by May 7, 2026, to get it, and the payment is set for July 2, 2026. Right now, the dividend yield is about 4.2%.

At a share price near $37, that yield is getting more interesting for income-focused investors than it was at $49.

The catch: NAB expects to apply a 1.5% discount to its H1 FY26 dividend reinvestment plan and partially underwrite it, with the combination expected to raise up to $1.8 billion and contribute up to approximately 40 basis points to the CET1 ratio in the second half of FY26.

A discounted DRP means existing shareholders who reinvest dilute themselves at lower prices. It is a modest but real headwind that deserves attention from income-focused holders.

The broader case for NAB as a dividend stock is still intact. The bank’s business lending franchise remains one of the strongest in the country, the credit quality concerns are manageable, and management has been transparent about what drove the charges.

None of that changes the fact that the stock ran into February at a valuation that was difficult to defend.

Where the National Australia Bank Share Price Forecast Stands

The analyst consensus target price for NAB currently sits at approximately $38.75, which is about 3.81% above the June closing price of $37.33. That is not exactly a ringing endorsement, but it does suggest the market is closer to fair value now than it was three months ago.

The 52-week range for NAB spans $36.03 to $49.45, with the average 12-month analyst price target sitting at $38.41. With the stock near its 52-week low, patient investors are getting a very different entry point than those who chased the February peak.

The company’s ability to earn money hasn’t disappeared. Sales are growing, even if it’s just a little bit.

The software charges are a one-off, and the credit provisions, while higher, reflect a prudent read on a genuinely more uncertain macro environment. Middle East conflict volatility, a weaker New Zealand dollar, and shifting credit model assumptions all played a role in the April disclosure.

What the market is repricing is not NAB’s ability to survive; it is the premium investors were paying for it.

FAQ

Q: Why did NAB’s share price fall so much in 2026?

A: NAB shares went down in 2026 for a few reasons. They had a $706 million credit charge, and then a $1.347 billion pre-tax software charge was announced in April. Also, their dividend reinvestment plan offered a discount, which usually means they were looking to raise more cash.

Q: Is NAB still paying dividends?

A: Yes, NAB announced an interim dividend of $0.85 per share for the first half of the 2026 financial year. It will be paid on July 2, 2026.

Q: What’s the forecast for NAB’s share price in 2026?

A: Most brokers expect the 12-month target price to be between $38 and $39. This means the stock probably won’t go up much from where it is today.

Q: Is it a good idea to buy NAB shares now that the price has dropped?

A: That depends entirely on individual risk tolerance and portfolio strategy.

Disclaimer:

This article is for informational purposes only and does not constitute financial advice. The information contained herein is based on publicly available sources and is accurate to the best of our knowledge at the time of publication. Colitco does not hold a financial services licence. Past performance is not a reliable indicator of future performance. Readers should seek independent financial advice before making any investment decisions.

Source:

https://www.asx.com.au/markets/company/NAB

https://announcements.asx.com.au/asxpdf/20260420/pdf/06ymw2r2p496xg.pdf

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.