Lithium prices recovered in January 2026, following a decline in 2024 and 2025. The spot price of lithium carbonate increased from the 2025 price floor to US$24,086 per tonne, data from Shanghai Metals Market indicated.

The CME lithium hydroxide contract jumped 86 per cent since January 2026. The contract traded above US$20,000 per tonne, a milestone matching data from 2023. This price action signals a transition from a market surplus to a deficit in materials.

Between June 2025 and February 2026, lithium spot prices increased by 180 per cent. The commodity reached US$10.48 per pound during the phase of recovery. Investors renewed focus on the sector as profit margins for extraction operations expanded.

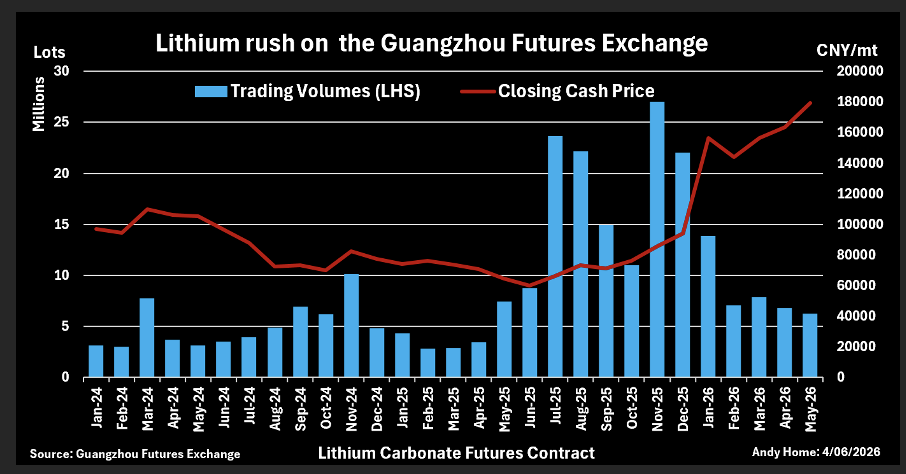

The volume of trade on the Guangzhou Futures Exchange reached 27 million contracts in November. The exchange managed speculation levels through adjustments to margins and fees. Prices remained above levels from 2025 despite a decrease in the volume of trade.

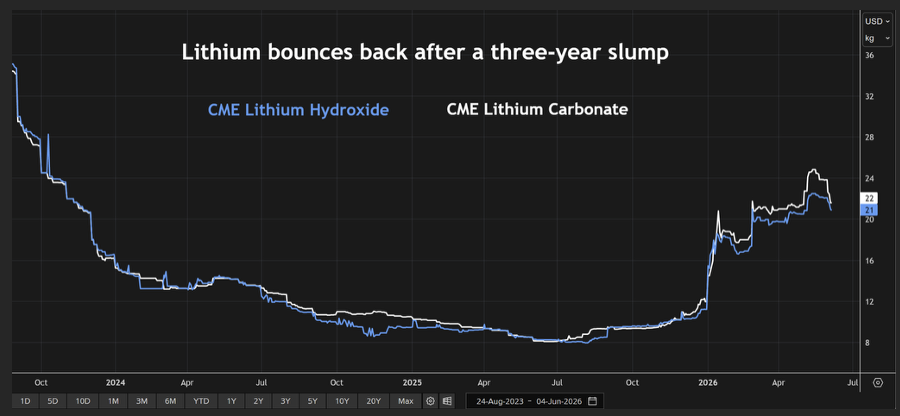

Figure 1: CME lithium hydroxide and carbonate cash prices [Mining.com]

Figure 1: CME lithium hydroxide and carbonate cash prices [Mining.com]

The market stabilisation altered expectations among commodity traders worldwide. Revenue streams for miners improved as benchmarks moved away from the cost floor. Financial indexes tracked the value recovery across asset classes.

The Strategic Importance of Lithium

Lithium supplies power batteries for vehicles and energy storage systems across the globe. Fluctuations in production costs influence the retail price of consumer transport. Buyers monitor market trends to predict the expenses of transition away from fossil fuels.

Lachlan Shaw stated, “with these current prices of diesel and petrol that we’re seeing globally, that total cost of ownership has shifted quite strongly in favour of electric vehicle ownership,” during a broadcast. Energy security concerns operators of transport fleets due to fuel variables. Vehicle drivers avoid fuel shortages at service stations by utilising battery power.

The expansion of data centres for artificial intelligence requires batteries for electricity stabilisation. Shipments of lithium batteries for data storage will rise 80 per cent over five years. Power utilities require storage systems for utilities to balance electricity grids.

Consumers pay utility rates that reflect the capital expenditure of power companies. Storage capacity installation will expand from 325 gigawatts in 2026 to 1,270 gigawatts by 2035. The cost of lithium influences the pace of infrastructure deployment worldwide.

Employment opportunities in the resource sector depend on the viability of extraction projects. Communities receive tax revenues and infrastructure benefits from operating mines. Stability in commodity pricing sustains economies in regions across Australia.

Key Players in the Lithium Market

- Companies drive adjustments across the sector. Contemporary Amperex Technology Limited suspended extraction activities at the Jianxiawo mine in Jiangxi province. This decision removed a supply source from the total worldwide.

- Research groups monitor indicators and alter projections. Benchmark Mineral Intelligence tracked market indicators and revised price forecasts. Adam Webb noted, “To all intents and purposes, lithium is basically driven by battery demand only,” during an industry presentation.

- Specialists in finance provide commentary on the economics of development. Andy Leyland described market dynamics between 2023 and 2025 as “unsustainable,” during a webinar. He noted that prices fell below requirements for asset developments.

- Exploration firms advance drilling schedules to capitalise on the price rebound. Surge Battery Metals advanced exploration activities at the project in Nevada. Fluor Corporation will complete a study of feasibility for the venture in December 2026.

- Institutions in banking allocate funds and analyse market trends. Citigroup and UBS Australia provided analysis on the pricing trajectory of the metal. EnergyX advanced operations across 100,000 acres at the Black Giant project in Chile.

Global Geography of Lithium Production

Market events occurred across manufacturing hubs and mining jurisdictions. China maintains a position as the centre for chemical refinement and futures trading. The province of Jiangxi serves as a hub for extraction activities within the country.

Australia contains rock deposits that supply spodumene concentrate to refiners. Operations at the Finniss, Bald Hill, and Mt Cattlin sites entered care and maintenance during the downturn. The assets reside in Western Australia and the Northern Territory.

The United States serves as a location for exploration and policy implementation. The government initiated actions under Section 232 to review reliance on imports of minerals. Projects receive investment to build supply chains in America.

The market dynamics extended to South America and Africa. Chile holds brine resources that attract capital from exploration entities. Zimbabwe implemented a quota regime for materials after an export ban in February.

Trading entities finalised contracts on exchanges in London, Shanghai, and Guangzhou. Refineries processed concentrates in zones of industry across Asia. Consumers purchased vehicles containing the metal in showrooms worldwide.

Timeline of the Lithium Price Cycle

The oversupply phase depressed the industry throughout 2024 and mid-2025. The price floor occurred in June 2025 when lithium carbonate traded at US$8,100 per tonne. The turnaround commenced in August 2025 when a mining licence expired in China.

Speculation peaked in November 2025 on the futures exchange in Guangzhou. Prices maintained positions through quarter one of 2026. The stability extends into June 2026 as market participants assess inventories.

Figure 2: Lithium rush on the Guangzhou Future Exchange [Source: Guangzhou Futures Exchange]

Figure 2: Lithium rush on the Guangzhou Future Exchange [Source: Guangzhou Futures Exchange]

Analysts project a market surplus from 2026 through 2029 due to a pipeline of projects. The market will transition into a deficit between 2030 and 2035 according to forecasts. This shortfall reflects the lack of investment during the downturn of 2024.

The price cycle completed a rotation over a period of five years. Boardrooms adjusted capital expenditure allocations during the months concluding 2025. The effects of these decisions manifest in the supply data of 2026.

Production pauses lasted for quarters at processing operations. Re-activation schedules require months of preparation before output matches capacity. The timeline for market equilibrium extends toward the end of the decade.

Also Read: World Oceans Day 2026: Protecting Our Seabed in an Era of Deep-Sea Mining Expansion

Market Drivers and Future Outlook

The expiration of a mining licence for Contemporary Amperex Technology Limited initiated the price recovery. This event created anxiety regarding supply availability among cathode producers. Buyers increased purchases to secure material for manufacturing requirements.

A shift in the chemistry of batteries altered consumption patterns for the metal. Lithium iron phosphate batteries increased their share of the vehicle market to 50 per cent in 2024. This change elevates the demand for lithium carbonate over lithium hydroxide.

Policy decisions by governments reshape the economics of the mining sector. Alliances and mineral agreements create a framework where countries prioritise supply security. The United States evaluates tariffs and price floors to protect extraction operations.

The industry expects a supply response despite the price increase. Developers delayed feasibility studies by 12 months during the price collapse. Companies require evaluations and financing arrangements before they resume development.

The market will experience a price retreat from July to December 2026 if operations in China resume production. Benchmark Mineral Intelligence expects a decline as capacity returns to service. Experts predict that price increases in the future will remain below the records of 2022.

Sources

- https://www.mining.com/web/column-lithium-bust-is-over-but-will-battery-metal-boom-again/

- https://investingnews.com/daily/resource-investing/battery-metals-investing/lithium-investing/lithium-forecast/

- https://carboncredits.com/lithium-prices-climb-again-in-2026-sending-stocks-skyward-nili

Disclaimer: This article provides a news report on commodity market trends only. It does not constitute financial, investment, or legal advice. Please conduct independent research and consult with licensed professionals before making any investment decisions in the resource sector.

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.