Australia’s economic landscape is shifting, and with it, interest rates may soon follow. NAB (National Australia Bank) has forecast a potential reduction in the official cash rate for February, which could directly impact mortgage rates across the country. Here’s what you need to know about this anticipated shift in monetary policy and how it could affect Australians with mortgages.

A Potential Rate Cut in February

This week, NAB made headlines with its updated predictions regarding interest rates. The bank now expects the Reserve Bank of Australia (RBA) to cut the cash rate by 25 basis points in February. This forecast comes in the wake of inflation data showing that price rises have slowed more than expected. NAB’s chief economist, Alan Oster, noted that the inflation data released in the last quarter suggested a more rapid moderation of inflation than the RBA had anticipated. As a result, the bank believes February is the most likely time for the RBA to start easing interest rates.

Also Read: Australian Inflation Rate Hits Three-Year Low, Raising Hopes for Interest Rate Cuts

Despite the strong performance of the labour market, with unemployment holding steady at 4%, NAB doesn’t see these conditions as inflationary. The combination of slowing inflation and a strong labour market gives the RBA enough confidence to consider cutting rates.

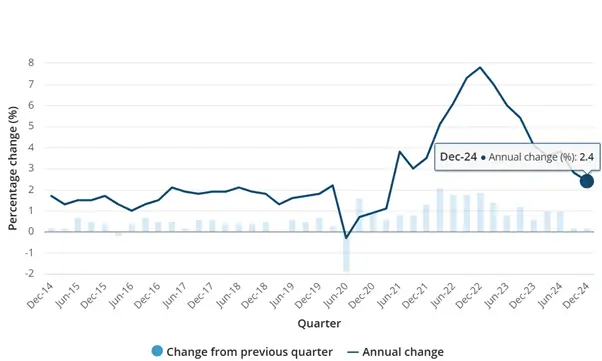

Inflation Figures Point to Easing

Inflation figures have been a key driver of the interest rate discussion. The Australian Bureau of Statistics (ABS) recently reported that inflation had moderated to 2.4% in the year to December 2024, the slowest annual rate since March 2021. The trimmed mean inflation, which excludes volatile items like food and energy, came in at 3.2% for the December quarter, slightly better than the RBA’s forecast of 3.4%.

These figures indicate that inflationary pressures are easing, which is a critical factor in the RBA’s decision-making process. As Oster pointed out, this data gives the central bank more room to revise its inflation outlook downward, which sets the stage for a possible rate cut in February.

Impact on Australian Mortgages

What does this mean for Australians with mortgages? A reduction in the official cash rate usually leads to lower mortgage interest rates. For many homeowners, this could result in lower monthly repayments, providing some relief in an environment of rising living costs.

The big four banks, including NAB, all now agree that the RBA will cut rates in February. While NAB expects the rate cut to be modest, they also foresee further reductions in 2025. The bank anticipates a total of 75 to 100 basis points in cuts over the course of the year, with the cash rate potentially stabilising at around 3.1% by February 2026.

What Other Banks Are Saying

Westpac has also adjusted its predictions following the latest inflation data. Westpac’s chief economist, Luci Ellis, has pushed forward her forecast for a rate cut to February. She noted that the inflation figures indicate a quicker-than-expected disinflationary trend, which gives the RBA confidence to start cutting rates.

The Commonwealth Bank (CBA) and ANZ had already predicted a rate cut in February, with CBA announcing this stance several months ago. Their confidence in a rate cut is based on the belief that inflation is coming under control, and the RBA will have enough evidence to start the easing process in February.

A Contrasting View: Is a Rate Cut Justified?

While there is widespread consensus among banks that the RBA will cut rates in February, not all economists are on board with this prediction. Judo Bank’s chief economic adviser, Warren Hogan, is unconvinced. Speaking to Sky News, he suggested that there is less than a 50% chance of the RBA cutting rates in February. Hogan argued that the economic case for a rate cut is not yet strong enough, citing improvements in consumer sentiment and job growth.

Hogan also pointed to rising job vacancies and low retail sales as indicators that the economy is improving, making a rate cut less urgent. He compared the situation in Australia to that of the United States, where rapid rate hikes were followed by pauses in rate cuts due to inflation fears. Hogan believes that the RBA should be cautious and learn from the US experience before proceeding with a rate reduction.

What’s at Stake for Australian Households?

If NAB’s forecast is correct, the potential rate cut could provide much-needed relief to Australian homeowners, particularly those with variable-rate mortgages. Many households have already felt the strain of rising interest rates, and a rate cut would offer some financial breathing room.

However, it’s important to remember that the rate cut may not be the cure-all for everyone. As the ABS points out, the CPI (Consumer Price Index) only provides a rough estimate of inflation, and the cost of living pressures felt by different households can vary greatly. Working households, for instance, may feel a greater pinch due to rising mortgage repayments, while self-funded retirees may have less exposure to housing costs but may still feel the impact of price rises in health and other sectors.

Looking Ahead: A Changing Economic Landscape

As February draws closer, all eyes will be on the RBA’s decision. If NAB’s forecast holds true, a rate cut could signal the start of a more gradual easing of monetary policy. For mortgage holders, this could mean lower repayments and a reprieve from the economic pressures of the past few years.

While there are differing opinions on whether the RBA should cut rates, it is clear that inflation is moderating more quickly than expected. Whether the RBA moves forward with a rate cut or holds steady, the outlook for the Australian economy remains uncertain, and much will depend on the evolving inflation data and labour market trends.

As always, Australians with mortgages should stay informed about the latest developments and be prepared for potential changes in their financial landscape in the coming months.