South32 dropped its March 2026 quarterly report today, and the numbers tell a story of resilience, record alumina production in Brazil, a landmark distribution from Sierra Gorda, and meaningful cash generation, all while the company navigated cyclones, floods, and the tragic death of a worker at Worsley Alumina.

For investors watching the South32 share price Australia closely, today’s update lands with a market cap just north of $20 billion and the stock sitting at $4.48 (as at 1 pm AEST, 22 April 2026), up $0.07 or +1.59% on the day.

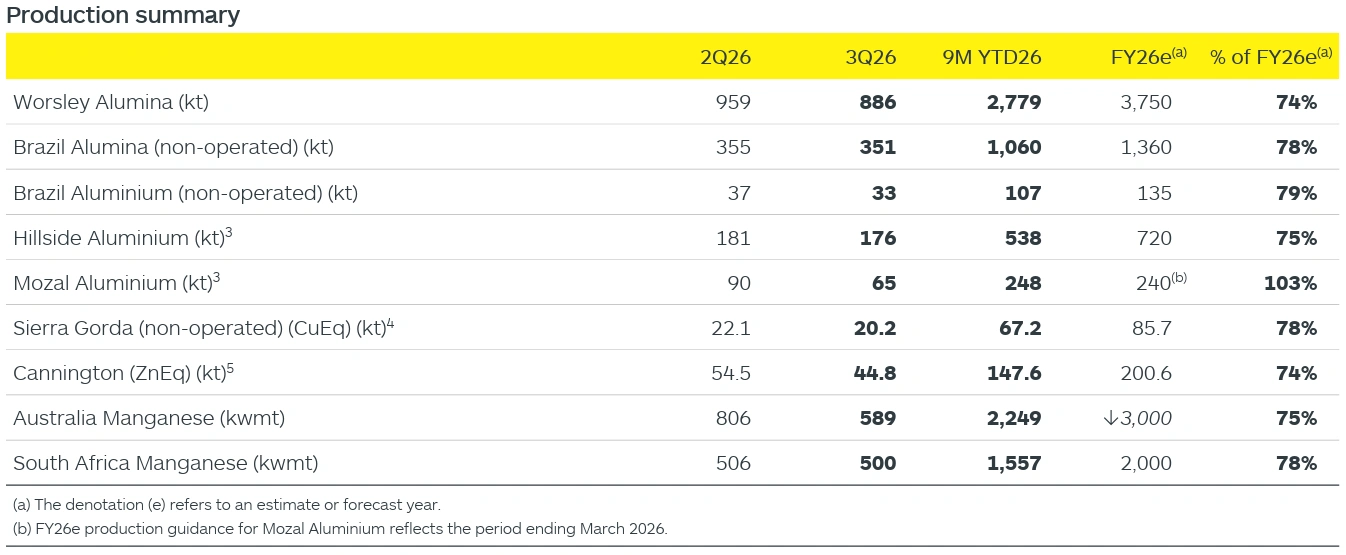

Figure 1: Production summary of South32 as mentioned in the March 2026 Quarterly Results [South32]

A Tragedy at Worsley That Can’t Be Overlooked

Before diving into the numbers, the report opens on a sober note.

CEO Graham Kerr led his statement with condolences for Mr Simon Mukwarami, who suffered fatal injuries on 14 March during routine plant maintenance at Worsley Alumina in Western Australia. Non-critical work at the site was temporarily suspended, and the relevant authorities continue their investigation with South32’s full cooperation.

“There is no acceptable outcome other than our people going home safe and well at the end of every shift,” Kerr said.

It’s a necessary reminder that behind the quarterly production tables, real people run these operations, and safety must always come first.

Financial Snapshot: Net Cash Climbs to US$96M

Strong Cash Generation Despite Heavy Growth Capex

South32 generated net cash of US$121M during the March quarter, lifting the group’s net cash position to US$96M.

That result came despite the company investing US$158M into growth capital expenditure at the Hermosa project in Arizona, its flagship zinc-lead-silver development.

Key financial highlights for the quarter and nine months to March 2026:

- Net cash position: US$96M (up US$121M in the quarter)

- Hermosa growth capex (9M YTD): US$496M

- Total group capex (excluding EAIs and Hermosa): US$239M over 9 months

- Tax payments (excluding EAIs): US$170M over 9 months

- Interim ordinary dividend paid post-quarter: US$175M, fully franked, for the December 2025 half year

- Share buy-back (9M YTD): US$35M; 17 million shares at an average of A$3.08 per share

The company also added approximately US$100M in lease liabilities to its balance sheet across the nine-month period.

Sierra Gorda Delivers a Record Distribution

One standout moment of the quarter was Sierra Gorda, South32’s Chilean copper mine (45% share), delivering a record quarterly distribution of US$135M.

That pushed total net distributions from equity accounted investments (EAIs) to US$375M for the nine months to March 2026, comprising US$315M from Sierra Gorda and US$60M from the manganese business.

Operations Update: Records, Weather, and a Few Headwinds

Alumina and Aluminium: Broadly on Track

Brazil Alumina was the standout performer. The refinery hit a record 1,060kt in the nine months to March 2026, up 5% year-on-year, running above nameplate capacity on the back of improved plant availability. Annual guidance of 1,360kt remains unchanged.

Worsley Alumina held steady at 2,779kt for the same period despite Tropical Cyclone Narelle disrupting gas supply and plant availability during the quarter. Production fell 8% quarter-on-quarter in March, but the annual guidance of 3,750kt stays in place.

Hillside Aluminium in South Africa continued testing its maximum technical capacity, producing 538kt for the nine months, broadly flat year-on-year. The operation pushed through load-shedding challenges, and FY26 guidance of 720kt holds.

Brazil Aluminium had a tougher quarter after pot outages and energy disruptions in late 2025 hit output. Production fell 11% quarter-on-quarter to 33kt in March, though all three potlines demonstrated improved stability by quarter-end. FY26 guidance of 135kt remains intact.

Mozal Aluminium in Mozambique transitioned to care and maintenance on 15 March 2026, as previously flagged to the market. The operation exceeded its revised production guidance by 3% before the wind-down.

Also Read: Emerald Resources Delivers High-Grade Gold Results in Growth Push

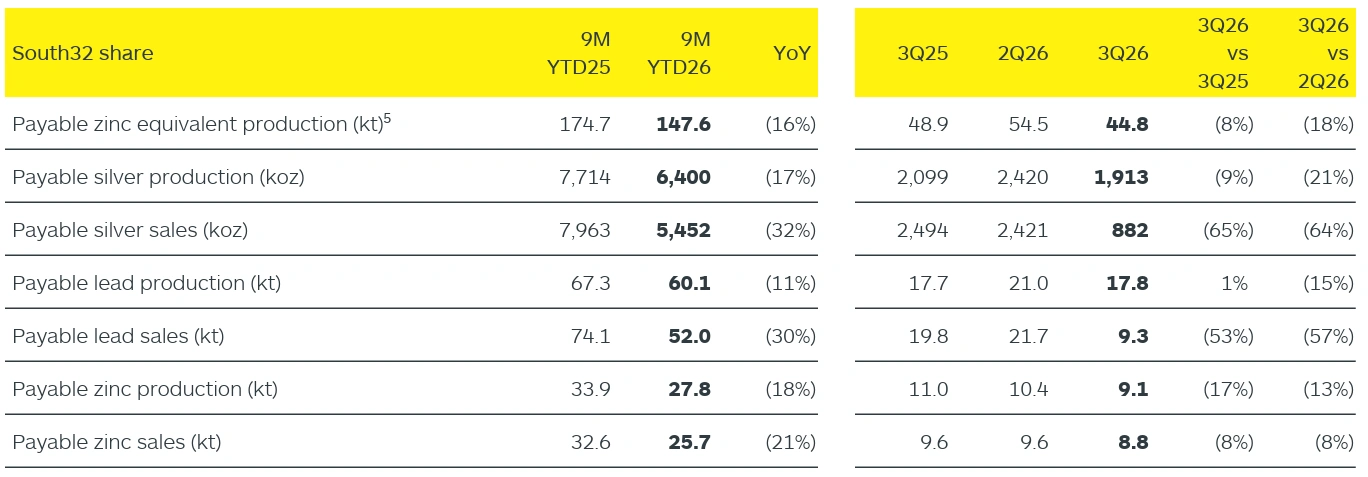

Cannington Battles Floods in Queensland

South32’s Cannington silver-lead-zinc mine in northwest Queensland copped significant flood damage during the quarter. Extended outages on a third-party rail line hammered sales, silver sales dropped 64% quarter-on-quarter, and lead sales fell 57%.

But the mine kept running. Ore processed actually ticked up during the quarter, and with rail access restored by the end of March, South32 expects to draw down stockpiled inventory through the June 2026 quarter. FY26 production guidance of 200.6kt (zinc equivalent) remains unchanged.

This kind of operational resilience matters for anyone tracking the South32 share price Australia through commodity cycles, as it shows the company can manage logistics disruptions without derailing core output.

Figure 2: Cannington (100% share), production and sales data for the nine months to March 2026 versus the prior year, showing significant weather-related sales declines across silver, lead and zinc in the March 2026 quarter. [South32]

Sierra Gorda — Copper Steady, Costs Set to Rise

Sierra Gorda maintained copper equivalent production at 67.2kt for the nine months to March — essentially flat year-on-year. Heavy rainfall during the March quarter temporarily suspended processing and cut into a key mining area, pulling quarterly output down 9% from the prior quarter.

The bigger news for investors: FY26 operating unit costs are expected to run 5–10% above current guidance of US$17.0 per tonne of ore processed. That reflects one-off workforce payments under new industrial agreements (now locked in until 2029), higher diesel prices, and a stronger Chilean peso.

The operation is also progressing a feasibility study for a fourth grinding line, with a potential joint final investment decision from the joint venture partners targeted for mid-CY26.

Australia Manganese — The Only Guidance Cut

Australia Manganese was the one operation that couldn’t hold its line. Elevated site water levels, wet season rainfall, and Tropical Cyclone Narelle in the quarter forced a 6% downgrade to FY26 production guidance, now set at 3,000kwmt. Water management will remain a key operational focus heading into FY27.

South Africa Manganese held its ground, sitting at 1,557kwmt for the nine-month period, with FY26 guidance of 2,000kwmt unchanged.

For context on other Australian resource companies navigating similar commodity environments, see Resolution Minerals’ antimony trioxide production update and CarbonXT’s $750K funding and growth strategy.

Also Read: Ora Banda Advances Golden Pole and Waihi Gold Development

South32 Share Price Australia: A Strong 2026 So Far

Investors keeping tabs on the South32 share price Australia have had plenty to smile about in 2026. The stock has surged on the back of stronger commodity prices, solid operational execution, and a cleaner balance sheet after South32’s exit from coal and other non-core assets in recent years.

| Metric | Value |

| Last Price (ASX: S32) | $4.48 (1 pm AEST, 22/04/2026) |

| Day Change | +$0.07 (+1.59%) |

| 1 Week | -4.07% |

| 1 Month | +12.56% |

| 2026 YTD | +25.84% |

| 1 Year | +71.65% |

| vs Sector (1yr) | +20.22% |

| vs ASX 200 (1yr) | +58.17% |

| Market Cap | ~$20.1B |

The 71.65% one-year return is striking, it outpaces the broader ASX 200 by more than 58 percentage points, a significant outperformance that reflects both company-specific execution and a strong commodity tailwind.

What Analysts Think

Analysts carry a consensus Strong Buy rating on S32 stock, with an average 12-month price target of around AU$4.87, implying roughly 7–8% upside from current levels. The high-end analyst target sits at AU$5.80. South32 has coverage from more than 10 Wall Street and Australian brokers, the majority of whom lean bullish heading into the June 2026 half-year.

For broader context, South32’s investment narrative centres on its transition-metals portfolio, copper, zinc, silver, and aluminium, which positions it alongside the global decarbonisation theme. The Hermosa project, if delivered on time and within budget, is widely viewed as a major long-term value driver for the South32 share price Australia.

Frequently Asked Questions (FAQs)

What does the company South32 do?

South32 is a diversified metals and mining company headquartered in Perth, Western Australia. It produces alumina, aluminium, copper, silver, lead, zinc, and manganese from a portfolio of operations across Australia, Southern Africa, South America, and the United States.

Is South32 a good share to buy?

South32 carries a consensus Strong Buy rating from analysts, with an average 12-month price target of around AU$4.87, implying approximately 7–8% upside from the current price. The company’s diversified commodity exposure, improving balance sheet, record distributions from Sierra Gorda, and the long-term potential of Hermosa are among the factors analysts point to as positives. Risks include:

- Commodity price volatility,

- Project execution risk at Hermosa,

- Rising input costs from global freight and energy disruptions, and

- Ongoing water management challenges at Australia Manganese.

This article is not financial advice; investors should conduct their own research or seek professional guidance before making any investment decisions.

Where is South32 located?

South32 is incorporated in Australia and headquartered in Perth, Western Australia.

Disclaimer

This article is produced for informational and educational purposes only. It does not constitute financial product advice, an investment recommendation, or a solicitation to buy or sell any security. The information contained in this article is based on publicly available sources, including South32’s March 2026 Quarterly Report and third-party analyst data. Past performance is not a reliable indicator of future results. Share prices and market data cited were accurate at the time of writing (22 April 2026, approximately 1 pm AEST) and may have changed. Readers should always conduct their own independent research and, where appropriate, seek advice from a licensed financial adviser before making investment decisions. Colitco and its contributors do not hold positions in S32 at the time of publication.

Sources

- https://www.south32.net/docs/default-source/all-financial-results/quarterly-report-march-2026.pdf

- https://www.south32.net/investors

- https://www.tipranks.com/stocks/au:s32/forecast

- https://simplywall.st/stocks/au/materials/asx-s32/south32-shares

- https://stockanalysis.com/quote/asx/S32/

Last modified: April 23, 2026