The Australian Government overhauled the country’s wealth taxation framework during the presentation of the 2026-27 Federal Budget. Treasurer Jim Chalmers announced the removal of the 50 per cent Capital Gains Tax (CGT) discount for individuals, trusts, and partnerships. The federal executive will replace this flat discount with a cost base indexation method that utilizes the Consumer Price Index to calculate real gains.

The Treasury also introduced a strict 30 per cent minimum tax floor on all net capital gains. This baseline rate guarantees that high-wealth individuals contribute a fixed minimum percentage on their investment profits regardless of offsetting deductions. The government framed the policy as a direct measure to “improve the fairness of the tax system, support home ownership and help fund new tax cuts for workers.”

The legislative package includes a strategic exemption for the residential construction sector to protect the national housing pipeline. Investors in newly built residential properties can choose between the traditional 50 per cent discount and the new inflation-indexed calculation. The administration aims to steer private capital away from speculative trading and toward new housing supply.

Figure 1: Treasurer Jim Chalmers and Prime Minister Anthony Albanese [ABC News: Callum Flinn]

The newly introduced Working Australians Tax Offset will operate alongside these adjustments to provide direct relief to low and middle-income earners. The federal budget papers reveal that the combination of these tax measures will generate significant revenue over the forward estimates period. This strategy allows the government to rebalance the tax mix without increasing baseline personal income tax brackets.

The budget document outlines several key structural elements of the reform:

- The replacement of the flat 50 per cent discount with cost base indexation for assets held over 12 months.

- The enforcement of a 30 per cent minimum tax rate as an absolute floor on net capital gains.

- The preservation of the full exemption for primary residential properties.

- A specific alternative choice for individuals who invest in new housing builds.

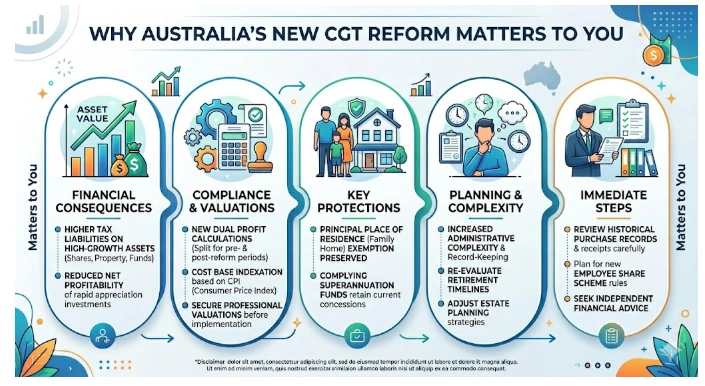

Why It Matters to Readers

This significant policy shift alters the financial projections for everyday wealth creators and property owners across the nation. Average citizens who sell shares, managed fund allocations, or real estate assets will experience higher tax liabilities if their assets grow faster than inflation. The new calculation methodology reduces the net profitability of high-growth investments.

Taxpayers must maintain meticulous financial records and secure professional asset valuations before the implementation date. The transition requires individuals to split their profit calculations into two distinct historical periods. While the policy protects long-term, slow-growing assets from inflationary taxation, it reduces the immediate cash flow advantages of short-term property flipping.

The package preserves the full Capital Gains Tax exemption for the principal place of residence, which protects the family home. Complying superannuation funds also escape these specific changes because they retain their current one-third tax concession. However, the added administrative complexity means that ordinary families must re-evaluate their long-term retirement timelines and estate planning structures.

Independent financial advisors recommend that investors review their historical purchase records and improvement receipts immediately. Failure to document these expenses will result in a lower cost base calculation and an inflated tax bill under the new indexation rules. Australians who use Employee Share Schemes must also adjust their expectations because the new rules alter the taxation of capital account interests.

Figure 2: Why Australia’s new reform matters

The new framework will affect everyday investment decisions through several practical channels:

- Higher compliance costs due to mandatory professional asset valuations.

- Increased taxation on assets that experience rapid capital appreciation.

- Additional record-keeping requirements for historical improvement costs and purchase records.

Key Stakeholders And Affected Industry Groups

The legislative changes directly affect millions of individual taxpayers, small business owners, and trust beneficiaries. Treasurer Jim Chalmers led the design of the economic package alongside key Treasury officials to fund the new Working Australians Tax Offset. The Australian Taxation Office holds the responsibility for enforcing compliance and distributing new digital calculation tools.

Major financial institutions, including the Commonwealth Bank of Australia, have initiated comprehensive portfolio reviews for their wealth management clients. Accounting firms face a significant surge in demand as clients seek structural advice to mitigate the new tax floor. Discretionary trusts face the most significant regulatory impact because the law applies the 30 per cent minimum tax directly at the trustee level.

The housing industry remains a central stakeholder as building associations react to the new investment incentives. The Property Council of Australia is analyzing the long-term impacts of the policy on private rental supply. Foreign institutional investors must also adapt to the expanded definitions of taxable real property, which now include large-scale renewable energy assets like wind turbines.

The federal opposition has vowed to fight the legislation in the Senate, labeling the changes as a direct attack on middle-class wealth accumulation. Minor parties and independent crossbenchers hold the balance of power and will negotiate the final amendments to the bill. Corporate leaders from the mining and renewable energy sectors are also lobbying lawmakers to clarify the treatment of statutorily severed assets.

Specific trust entities receive explicit exclusions from the new 30 per cent minimum tax floor to protect vulnerable groups:

- Complying superannuation funds and fixed testamentary trusts.

- Special disability trusts and charitable organisations.

- Deceased estates during their standard administration periods.

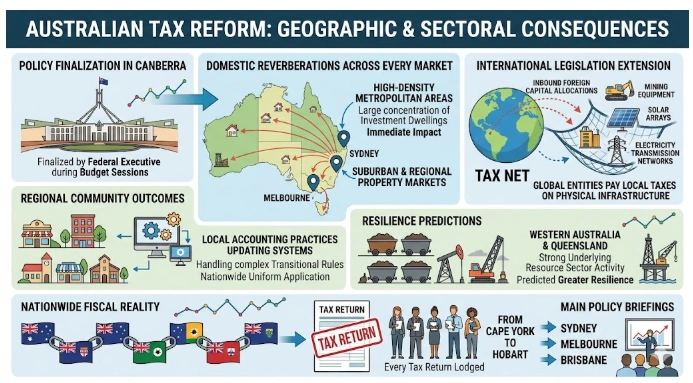

Geographic Reach And Jurisdictional Boundaries

The federal executive finalized these tax reforms in Canberra during the official budget sessions at Parliament House. The geographic consequences of the policy, however, will reverberate across every suburban and regional property market in Australia. High-density metropolitan areas like Sydney and Melbourne will feel the most immediate impact due to their large concentrations of investment dwellings.

The legislation extends its reach beyond domestic borders to modify the rules for inbound foreign capital allocations. The new statutory definitions bring assets like mining equipment, solar arrays, and electricity transmission networks into the domestic tax net. This international expansion ensures that global entities pay local taxes on profits derived from physical infrastructure on Australian soil.

Regional communities will experience varying outcomes as the policy alters the dynamics of local real estate investment. Local accounting practices in regional centres are already updating their systems to handle the complex transitional rules. The nationwide scope of the policy ensures a uniform application across all state and territory jurisdictions.

The Treasury held its main policy briefings in the commercial centres of Sydney, Melbourne, and Brisbane to address institutional concerns. Industry analysts predict that the property market in Western Australia and Queensland might show greater resilience due to strong underlying resource sector activity. Ultimately, the fiscal reality of these laws will affect every tax return lodged from Cape York to Hobart.

Figure 3: Geographic and sectoral consequences

Implementation Timeline And Crucial Deadlines

The government handed down the structural changes on 12 May 2026 as the centerpiece of the federal budget night. The announcement followed a detailed Senate inquiry by the Select Committee on the Operation of the Capital Gains Tax Discount, which tabled its final report on 17 March 2026. This legislative progression represents the first major alteration to the discount system since its introduction in 1999.

The official commencement date for the new indexation framework is 1 July 2027. This timeline grants investors a transitional window to adjust their portfolios and formalize asset valuations. The grandfathering arrangements protect all capital gains that accumulate prior to this mid-2027 deadline.

The tightening of negative gearing benefits for established properties took effect immediately at 7:30 PM Australian Eastern Standard Time on 12 May 2026. The government will implement the 30 per cent minimum tax rate simultaneously with the indexation changes in 2027. This phased rollout provides financial institutions with the necessary time to update their technological infrastructure.

The government initially flagged the expansion of non-resident capital gains rules during the May 2024 budget before releasing the exposure draft in April 2026. This multi-year policy development culminated in the definitive announcements during the 2026 parliamentary winter session. Taxpayers have exactly fourteen months from the announcement date to finalize their portfolio strategies before the new system activates.

Structural Execution And Market Adjustment Mechanisms

The implementation will introduce a dual-calculation environment where taxpayers must segregate their capital gains based on the transition date. For assets acquired before the deadline, individuals will apply the old 50 per cent discount to the profit portion accrued up to 1 July 2027. They will then apply the new Consumer Price Index indexation method to any subsequent growth.

The Australian Taxation Office will launch automated portals to help individuals navigate these multi-tiered compliance requirements. The real estate market may experience a short-term increase in listing volumes as investors lock in existing valuations before the deadline. Many wealth creators will likely transition their assets out of discretionary trusts and into corporate structures to secure stable tax rates.

Long-term economic models indicate that the policy will successfully divert capital into new residential construction projects. First-home buyers will likely face less competition from property speculators in the established housing market. The ultimate efficacy of the reform rests on its ability to pass the Senate and the future stability of national inflation rates.

The Australian Taxation Office will establish a dedicated compliance taskforce to monitor asset valuations at the transition date. This measure will prevent artificial price inflation and ensure accurate historical baselines for future indexation. The broader economy will adapt as investment funds pivot toward high-yielding corporate equities and commercial real estate assets.

The long-term transition will likely reshape the Australian investment landscape across several phases:

- An initial rush of property valuations and potential asset sales before mid-2027.

- A structural shift in capital allocation toward newly constructed residential developments.

- Increased utilization of corporate structures to bypass trust-specific tax minimums.

Disclaimer: This article serves exclusively for informational and journalistic purposes. It does not constitute professional financial, legal, or taxation advice. Readers must consult a certified Australian financial advisor or registered tax agent before executing any investment or structural modifications based on these proposed legislative developments.

Frequently Asked Questions

1. What are the core changes to the Capital Gains Tax system?

The current 50% CGT discount for assets held longer than 12 months will be replaced by cost base indexation linked to the Consumer Price Index (CPI). Additionally, a minimum tax rate of 30% will apply to net capital gains.

2. When do these new CGT rules take effect?

The reformed system is scheduled to commence on 1 July 2027. The new rules apply to capital gains that accrue after this date, subject to the passage of legislation.

3. How will investments held before the announcement be taxed?

A transitional framework will apply to existing assets. Capital gains accumulated up to 1 July 2027 will be grandfathered under the current system, allowing investors to utilize the 50% discount for that period. The new indexation and minimum tax rules will apply only to value increases that occur after 1 July 2027.

4. Do the changes affect assets acquired before 1985?

Yes. The blanket tax exemption for pre-CGT assets acquired before 20 September 1985 will conclude. Valuation profiles will be established on 1 July 2027, and any capital gains accruing after that date will become subject to the new tax laws. Gains accrued prior to 1 July 2027 remain exempt.

5. Are there exemptions for new housing investments?

Yes. Investors purchasing new residential builds maintain the option to choose either the traditional 50% CGT discount or the new indexation and minimum tax framework upon sale. These properties also remain exempt from the new restrictions placed on negative gearing.

Sources

- https://www.commbank.com.au/articles/newsroom/2026/02/cgt-capital-gains-tax-explained

- https://kpmg.com/xx/en/our-insights/gms-flash-alert/2026/flash-alert-2026-133

- https://www.pm.gov.au/media/tax-reform-workers-businesses-and-future-generations

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.