TPG Telecom Limited (ASX: TPG) has refreshed its strategic direction at an investor day presentation, setting out a comprehensive blueprint to capitalise on mobile expansion, reduce costs and balance sheet discipline. The Company is moving away from complexity and honing in on what drives true value.

![]()

Figure 1: TPG Telecom corporate logo and brand identity. [Courtesy: TPG Telecom]

This is not a dramatic reinvention. It is a careful narrowing of priorities by one of Australia’s largest listed telecommunications businesses. For investors watching the ASX: Telecommunications sector, the numbers behind this update tell a more interesting story than the headline.

What the Strategy Update Covers

As such, the ASX announcement from TPG Telecom is focused very clearly on four things: additional mobile revenue growth, more digital subscription brands, tighter fixed broadband margins and less capital expenditure in the medium term.

The Company has moved away from broad ambition and toward specific financial targets. Each pillar of the strategy carries measurable outcomes, which is exactly what investors in the ASX: Telecommunications sector want to see.

Mobile Growth and ARPU Momentum

Subscriber Numbers and Revenue Share

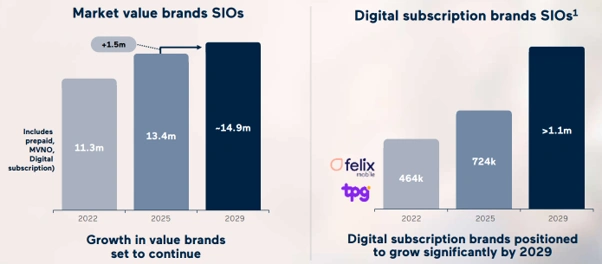

TPG Telecom’s mobile market is split between premium brands, which hold approximately 70% of revenue share, and value brands, including prepaid, MVNO, and digital subscription, which account for the remaining 30%. The subscriber data from the investor presentation tells the growth story clearly.

Figure 2: TPG Telecom mobile subscriber growth, 2022–2025. [Courtesy: TPG Telecom]

| Metric | 2022 | 2025 |

| Value brand SIOs | 11.3 million | 13.4 million |

| Premium brand SIOs | 17 million | 17 million |

| Mobile ARPU | A$32.4 | A$35.5 |

| Mobile market share | 16.0% | 16.8% |

Value brand subscribers have grown while premium subscriber numbers have held steady. Mobile ARPU has grown at a CAGR of 3.1% from 2022 to 2025, reaching A$35.5 in FY25.

The Digital Subscription Advantage

TPG Telecom’s digital subscription brands, Felix Mobile and TPG, are where the margin logic gets interesting. Digital subscription customers carry approximately 30% higher ARPU than traditional prepaid customers. At the same time, the cost to serve them is approximately 65% lower than that of postpaid customers, because the model avoids expensive retail channels and commission costs entirely.

Figure 3: Growth in value-brand and digital subscription customers. [Courtesy: TPG Telecom]

Value brand digital subscription SIOs have grown from 464,000 in 2022 to 724,000 in 2025. The Company is targeting more than 1.1 million digital subscription SIOs by 2029. That trajectory, if maintained, directly improves margin per customer without requiring proportional cost increases.

Fixed Broadband and Fixed Wireless

TPG Telecom’s Home Broadband margin improved from 618 to 628 between 2024 and 2025, a 2% gain in what the Company itself describes as an intensely competitive market. The key data points from this segment are worth noting:

- Overall, the NBN market has remained essentially flat at around 8.8 million services, growing at just 0.3% CAGR

- High-speed NBN connections have jumped from 23% of the total in 2022 to 43% in 2025

- Fixed Wireless footprint has expanded by 15 to 20% since the 5G standalone launch

- TPG Telecom’s Fixed Wireless subscriber base has grown from 410,000 (2022) to 666,000 (2025) at a CAGR of 17.5%

Fixed Wireless is establishing itself as a true NBN substitute, growing for more and more Australian homes, and TPG Telecom could be one of the strongest performers in this space.

Capex Reduction and Cash Flow Improvement

Capital Expenditure Coming Down

Group capex has been falling nd the trajectory continues well into the end of the decade:

- FY25: A$847 million

- FY26: A$750 million

- FY27: A$650 million

- FY28 to FY29 target: A$550 million to A$650 million

5G upgrades are completed, and IT modernisation is the driver of medium-term capex. As an additional positive for the outlook, 6G upgrades don’t start until after 2030, removing a near-term capital risk.

D&A Reduction from FY30

TPG Telecom is anticipating a reduction of more than A$200 million in depreciation and amortisation charges from FY30 onward. This reflects three things: CapEx peaked in FY23, customer base assets recorded at the merger will be fully amortised by mid-2028, and spectrum amortisation expenses will reduce over the medium to long term. That D&A decline flows directly to improved earnings without requiring additional revenue growth.

Free Cash Flow to Equity has been improving materially since FY25 and is forecast to continue improving through FY26, FY27, and FY28.

Balance Sheet and Debt Position

TPG Telecom is maintaining its S&P BBB investment grade credit rating, with a leverage target of 2.75x. The key balance sheet positions from the ASX announcement are:

- FY26 refinancing planned; debt maturities capped at no more than A$500 million in any single year

- FY28 debt facilities: A$796 million, to be refinanced and termed out in FY26

- FY29 Asian Term Loan: A$500 million

- Spectrum renewal in FY28 is expected to temporarily reduce headroom before recovery resumes from operating performance

The Company has funding optionality from strong operating cash flow and borrowing headroom to manage spectrum payments recommencing in FY28.

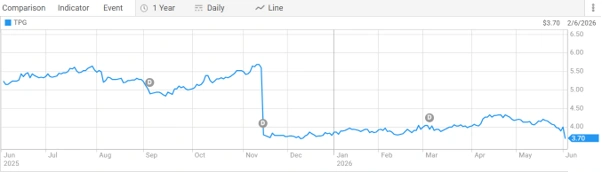

Share Price and Market Position

- Last Price: A$3.700 per share

- Market Capitalisation: A$7.85 billion

- 52-Week Range: A$3.500 and A$5.850 per share

Figure 4: TPG Telecom (ASX: TPG) one-year share price performance. [Courtesy: ASX]

About TPG Telecom

TPG Telecom is Australia’s second largest telecom Company, providing millions of customers across mobility, network broadband and business connectivity services nationwide. Specifically, it runs a suite of household name brands. These include Vodafone Australia, iiNet and Felix Mobile with both consumer and business-facing positions.

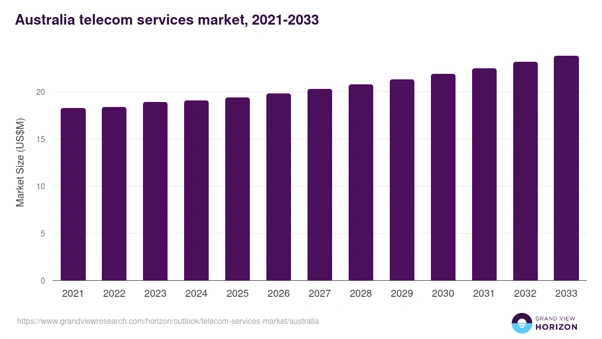

Industry Outlook

The telecom industry of Australia will continue to have steady growth in the long run. Industry expects the market to grow from US$19.4 billion in 2025 and reach $23.8 billion by 2033, at a CAGR of 2.6% between 2026 and 2033

Figure 5: Australia’s telecommunications market growth forecast. [Courtesy: Grand View Research]

For this growth, various trends are in favour, such as the increasing mobile data usage, adoption of 5G services and expansion of Fixed Wireless solutions in regional areas. Moving to higher-speed NBN tiers provides an additional layer of revenue growth opportunity, and will especially benefit operators with existing strong fixed broadband positions.

TPG Telecom’s focus on digital subscription growth and network cost efficiency places it in a reasonable position to participate in that market expansion.

Future Direction and Impact on Investor Returns

Impact on Earnings and Shareholder Value

The numbers in the ASX TPG investor update point in one direction. Falling capex, a D&A reduction of more than A$200 million from FY30, improving ARPU, and a growing digital subscription base all feed into a stronger earnings profile from FY27 onward. This strengthens the TPG Telecom share outlook Australia investors are watching closely.

Investors should track mobile subscriber net additions, digital subscription SIO growth, and cost per user figures across upcoming half-year and full-year results. Those are the metrics that will tell the real story behind the TPG Telecom strategy update.

What Could Shift the Outlook

The ASX Telecommunications sector is competitive and unforgiving. Telstra is still more difficult to beat in terms of the quality of the network. The strategy depends on the speed of recovery, and any slip in customer satisfaction, network investment timing and unanticipated spectrum costs could shackle this plan. Execution remains the risk.

ALSO READ: St George Mining Welcomes ATL as Shareholder Following Lithium Star JV Restructure

FAQs

Q1. What is the TPG Telecom strategy update about?

Ans. TPG Telecom has a multi-year plan to grow mobile ARPU, expand digital subscriptions, invest into Fixed Wireless, reduce capex, and manage its balance sheet.

Q2. What is the current ASX TPG share price?

Ans. TPG Telecom is trading at A$3.700 per share, with a 52-week range of A$3.500 to A$5.850 per share.

Q3. Why are digital subscription brands important to the TPG Telecom strategy?

Ans. They carry approximately 30% higher ARPU than traditional prepaid and cost approximately 65% less to serve than postpaid customers, making them a high-margin growth path.

Q4. How much is TPG Telecom reducing its capex?

Ans. Group capex is targeted at A$550 million to A$650 million by FY28 to FY29, down from A$1,082 million in FY23.

Disclaimer

This article is meant only for informational purposes. If you are an investor who is watching TPG Telecom closely, all the data published in this content is sourced from ASX announcements, the TPG Telecom investor day presentation, and external sources. Kindly verify all information related to the share price and market data. Any investment should be made at the investor’s own risk. Colitco does not hold any position in the above-mentioned Company.

Sources

- https://www.grandviewresearch.com/horizon/outlook/telecom-services-market/australia

- https://data-api.marketindex.com.au/api/v1/announcements/XASX:TPG:2A1674998/pdf/inline/investor-day-presentation?_gl=1*1fg4mju*_ga*MTcwODQzODA4Ni4xNzYyMjUxMTk2*_ga_R504V9JPBH*czE3ODAzNjEzMzckbzE0NyRnMCR0MTc4MDM2MTMzNyRqNjAkbDAkaDA.

- https://www.asx.com.au/markets/company/TPG