The result landed on 4 May 2026 and came with a headline that looked softer than the story underneath. Strip out a $949 million accelerated amortisation charge tied to a change in the bank’s software capitalisation policy, and NAB’s cash earnings rise to $3,558 million, up 2.3 per cent on the prior half.

CEO Andrew Irvine framed the result around execution rather than optics.

“Continued disciplined execution of our strategy and ongoing momentum across our business is reflected in NAB’s 1H26 operating performance,” Irvine said.

He acknowledged the notable item, but pointed to underlying profit growth of 6.4 per cent across all core divisions as the truer measure of where the bank is tracking.

NAB Half Year Results 2026: Breaking Down the Key Numbers

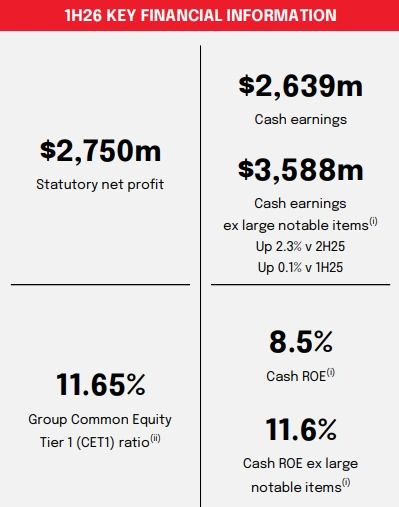

NAB 2026 Half Year Results summary. [National Australia Bank]

The headline figures for the six months ended 31 March 2026:

- Cash earnings (reported): $2,639 million

- Cash earnings (ex large notable item): $3,558 million, up 2.3% on 2H25

- Statutory net profit: $2,750 million

- Revenue growth:1%

- Net Interest Margin (NIM):81%, up 3 basis points

- Underlying profit growth (ex large notable item):4%

- Group CET1 ratio:65%

- Interim dividend: 85 cents per share, fully franked

The 85-cent interim dividend returns approximately $2.6 billion to shareholders, including around 500,000 direct holders and millions of Australians with superannuation exposure to NAB.

A partially underwritten dividend reinvestment plan at a 1.5 per cent discount is expected to raise roughly $1.8 billion, pushing the pro forma CET1 ratio to 12.05 per cent.

Business Banking Drives the Strongest Divisional Performance

NAB’s Business and Private Banking (B&PB) division was the clear standout, posting cash earnings of $1,850 million for the half, up 9.9 per cent on the prior period.

Australian business lending grew 5.6 per cent, with NAB reporting market share gains in both small-to-medium enterprise (SME) and total business lending categories.

Proprietary home lending drawdowns improved from 41.4 per cent in 2H25 to 47.7 per cent in 1H26, a meaningful shift that points to NAB winning back ground in owner-occupier channels.

Deposit balances across B&PB and Personal Banking grew 4.7 per cent, with transaction accounts (excluding offsets) up 8.0 per cent.

Personal Banking earnings were broadly stable at $700 million, while Corporate and Institutional Banking fell 2.6 per cent to $921 million, weighed down by higher credit impairment charges on a small number of individual clients.

New Zealand Banking contributed NZD 728 million, up 3.4 per cent on the prior half.

Provisions Rise Sharply Amid Geopolitical Uncertainty

The credit impairment charge jumped to $706 million for the half, compared with $485 million in 2H25.

The increase reflects both individual assessments across the business lending and unsecured retail portfolios, and a deliberate decision to build forward-looking provisions.

NAB increased collective provisions by $300 million, citing risks stemming from the Middle East conflict.

Affected sectors include Agriculture, Transport and Storage, Manufacturing, Construction, and Commercial Property, with the bank also lifting the weighting of its downside economic scenario to 45 per cent.

The ratio of collective provisions to credit risk-weighted assets rose 2 basis points to 1.35 per cent.

Non-performing exposures as a percentage of gross loans fell 3 basis points to 1.52 per cent, a small sign of underlying portfolio resilience despite the broader provision build.

The Rate Cycle Has Turned and Not in the Way Borrowers Hoped

The Australian economy entered 2026 in stronger shape than many expected, finishing 2025 with real GDP growth of 2.6 per cent. But that strength fed back into inflation, with core CPI rising to 3.4 per cent year-on-year by late 2025.

The Reserve Bank of Australia responded by lifting the cash rate 25 basis points in both February and March 2026, returning the rate to 4.10 per cent. A further hike is forecast for May.

That is a sharp reversal from the rate-cutting cycle that dominated much of 2025. Colitco previously covered NAB’s business loan rate cuts following the RBA’s 2025 easing cycle and the RBA’s first rate cut in four years, which now looks like a brief window that has closed.

NAB’s NIM rising 3 basis points to 1.81 per cent in this environment reflects the benefit of repricing on the deposit replicating portfolio, partially offset by mortgage competition and lower margins in offshore units.

GDP growth is forecast to slow to 1.5 per cent in 2026, with unemployment expected to peak at around 4.75 per cent before moderating. The Middle East conflict remains a significant and hard-to-quantify wildcard.

Costs, Technology, and the Software Write-off Explained

The $949 million large notable item deserves context. It stems from a change in NAB’s software capitalisation policy, accelerating amortisation of previously capitalised development costs.

It is a non-cash accounting adjustment tied to the rapidly changing technology environment, not an operational loss.

Excluding this item, NAB’s total expenses fell 0.5 per cent for the half, reflecting $199 million in productivity savings that the bank says are tracking toward its full-year target of more than $450 million.

The bank expects total cost growth to remain below 4.6 per cent for FY26, excluding the notable item.

Irvine flagged that investment in artificial intelligence remains a core focus.

“We are investing in areas such as artificial intelligence to grow, be more productive, and build skills for the future,” he said.

NAB also launched 24/7 fraud detection tools during the half, including real-time SMS alerts for business cardholders and a live chat fraud assist service.

What This Means for Investors

The result is best read as a bank in reasonable shape navigating a genuinely difficult macro environment. The software write-off is a one-off. The underlying profit trajectory is positive.

The dividend is maintained. And the balance sheet, with a CET1 ratio above 11.6 per cent and liquidity coverage at 132 per cent, is not under pressure.

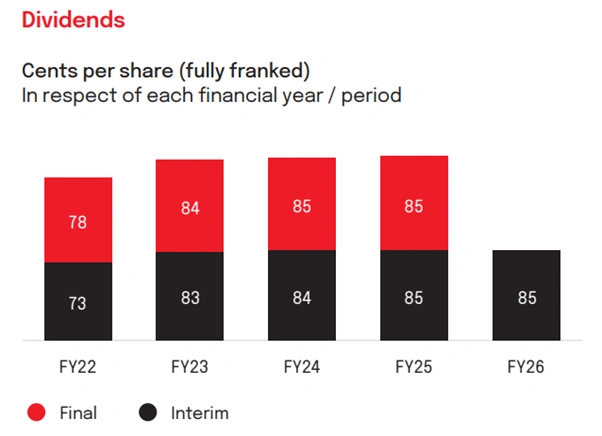

NAB interim and final dividends per share from FY22 to FY26 [National Australia Bank]

The risks are real, however. A rising cash rate, elevated credit impairment charges, and geopolitical uncertainty all point to a more cautious second half.

NAB has front-loaded its provision build, which may provide some buffer, but it has also acknowledged that forecasting visibility is lower than usual.

For shareholders, the 85-cent fully franked interim dividend provides steady income in an uncertain environment.

For the broader market, the result tells a story of a major Australian bank managing cost discipline and business lending growth while absorbing some genuine headwinds.

Also Read: How Beginner Investors Can Start on the Australian Stock Market in 2026

FAQs

Q: What were NAB’s cash earnings for the 2026 Half Year Results?

A: National Australia Bank reported statutory cash earnings of $2,639 million for the six months to 31 March 2026. Excluding a large one-off software capitalisation charge, cash earnings were $3,558 million, up 2.3 per cent on the prior half.

Q: What dividend did NAB declare for the first half of 2026?

A: NAB declared a fully franked interim dividend of 85 cents per share, returning approximately $2.6 billion to shareholders.

Q: Why did NAB’s reported profit fall compared to expectations?

A: A $949 million large notable item related to a change in the bank’s software capitalisation policy reduced reported cash earnings. This is a non-cash accounting charge, not an operating loss.

Q: How did NAB’s business banking division perform?

A: Business and Private Banking was the standout division, with cash earnings of $1,850 million, up 9.9 per cent on the prior half. Australian business lending grew 5.6 per cent, with market share gains in SME and total business lending.

Q: What is NAB’s outlook for the Australian economy in 2026?

A: NAB expects real GDP growth to slow to around 1.5 per cent in 2026, with unemployment peaking at approximately 4.75 per cent. The RBA is expected to continue raising interest rates, with the Middle East conflict adding significant uncertainty to forecasts.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Colitco does not recommend buying or selling any asset. Readers should conduct independent research or consult a qualified financial advisor before making any investment decision.

Source:

Last modified: May 4, 2026