South32 Limited (ASX: S32) has released a comprehensive update on its Hermosa Project in Arizona, United States, confirming major improvements to the Taylor zinc-lead-silver project. The announcement was released on 30 Apr 2026, covering expanded reserves, a longer mine life, revised capital costs, and a confirmed production timeline.

![]()

Figure 1: South32 Limited corporate logo [Courtesy: South32]

South32 mining project news from Hermosa signals a step-change in the scale and confidence of the Taylor development. The Company has confirmed first production in H2 FY28, nameplate capacity by FY31, and steady-state EBITDA of approximately US$650 million per annum based on long-term price assumptions.

Taylor’s Life Extended and Reserves Grow Substantially

South32 mining news confirms that Taylor’s initial operating life has been extended by approximately five years to around 33 years since final investment approval. This extension was driven by successful infill drilling programs that significantly upgraded both the Mineral Resource and Ore Reserve estimates.

South32 Chief Executive Officer Graham Kerr said: “Our updated assessment of project execution has reaffirmed Taylor’s potential to deliver our shareholders attractive returns from its long-life, low-cost production of zinc, silver and lead.”

Ore Reserve and Mineral Resource Growth in Detail

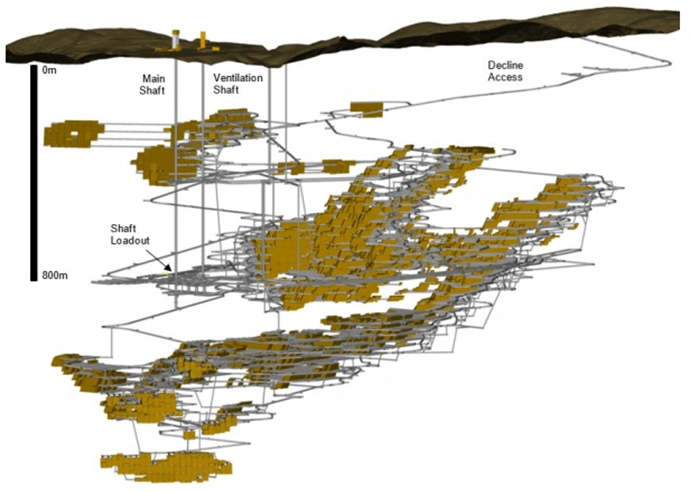

The Taylor Ore Reserve has increased by 52% to 99 million metric tons at 3.95% zinc, 4.50% lead, and 77 g/t silver as at 30 Apr 2026. This underpins approximately 25 years of Taylor’s initial operating life.

Figure 2: Technical diagram Taylor Mine Plan [Courtesy: South32]

The Taylor Mineral Resource has grown 10% to 169 million metric tons at 3.51% zinc, 3.88% lead, and 76 g/t silver. The deposit remains open in several directions, providing further South32 resource and reserve growth potential beyond the current mine plan.

Peake Deposit Adds Copper Upside

The adjacent Peake deposit has recorded a 32% increase in its Mineral Resource estimate to 33 million metric tons at 1.78% copper equivalent.

South32 expects Peake to become a future source of copper production and mine life extension within the Taylor development. Continued drilling is planned to test the potential for a continuous mineralised system connecting Peake and Taylor Deeps.

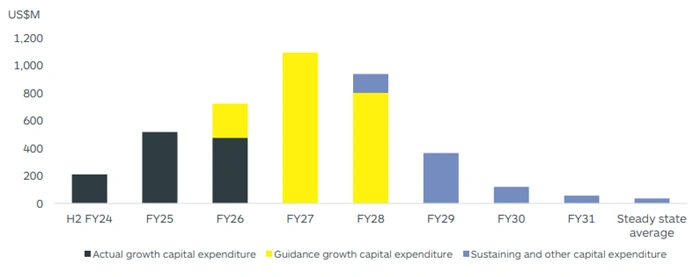

Capital Revised Higher on Scope and Inflation

South32 mining project costs have been revised upward, with expected growth capital expenditure for Taylor now set at approximately US$3,300 million. This compares to the original feasibility study estimate of approximately US$2,160 million at final investment approval in February 2024.

Figure 3: Hermosa Project construction site in Arizona [Courtesy: South32]

Breaking Down the Capital Increase

- Decline infrastructure additions account for approximately US$100 million

- Revised shaft construction costs account for approximately US$450 million

- Higher inflation, industry-wide input cost increases, and United States tariff impacts account for approximately US$500 million

- Installed prices for steel, piping, and concrete have more than doubled compared to the feasibility study estimate

- Steel requirements have been optimised and reduced by approximately 30% following detailed engineering, partially offsetting pricing impacts

- The majority of work packages are now contracted or subject to final pricing, significantly lowering the remaining capital risk profile

Figure 4: Taylor project capital expenditure profile [Courtesy: South32]

Kerr noted the impact of external factors: “Following our final investment approval, geopolitical tensions and higher tariffs in the United States have driven materially higher inflation and escalation in key input costs.”

Shaft Construction Delays and Mitigation

The South32 mining project has faced contractor performance and productivity challenges in shaft construction. The ventilation shaft is approximately 75% complete at a depth of approximately 618 metres as of April 2026.

The main shaft has reached approximately 478 metres, representing approximately 53% completion. As a result of these challenges, first production from shafts is now expected from H1 FY29.

Targeted measures, including strengthening contractor leadership, engaging specialist performance advisors, and bringing critical scope under direct owner management, have improved performance.

However, South32 has determined these measures will only partially mitigate the impact of contractor underperformance.

Clark Decline Adds Operational Flexibility and Earlier Access

South32 mining news includes a meaningful structural improvement through the Clark deposit exploration decline. Completed in the December 2025 quarter on schedule and on budget, the Clark decline provides additional access to the Taylor orebody ahead of full shaft commissioning.

This approach increases ore handling capacity by approximately 25% and enables the first ore from decline access in mid-FY28. Over the next 12 months, South32 will assess surface infrastructure de-bottlenecking options, which have the potential to increase production above current design rates.

Financial Returns Affirmed at Steady State

South32 resource and reserve growth is matched by strong financial projections. Based on updated long-term commodity price assumptions, Taylor is expected to deliver steady-state EBITDA of approximately US$650 million per annum, with an EBITDA margin of approximately 58%.

The post-tax net present value stands at approximately US$3,100 million at a 7.0% discount rate, with a post-tax internal rate of return of approximately 19%.

At spot commodity prices as at April 2026, these returns improve further to approximately US$800 million EBITDA per annum and a net present value of approximately US$4,500 million.

Total life of mine revenue is estimated at approximately US$32,600 million, with total EBITDA of approximately US$18,900 million. Silver alone is projected to contribute approximately US$12,600 million in total revenue over the mine life, reinforcing the depth of value within the Taylor orebody.

Hermosa Project Scope and Strategic Positioning

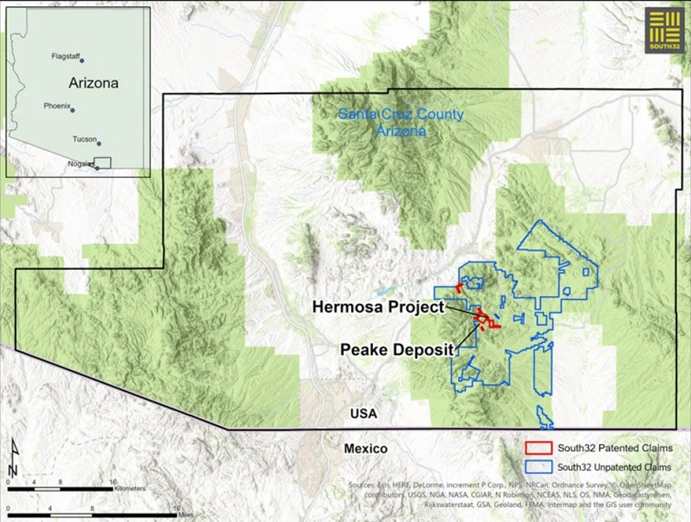

The Hermosa Project spans Santa Cruz County in Arizona and is 100% owned by South32. It hosts multiple deposits with the potential to produce critical minerals for several decades, with the Taylor zinc-lead-silver project as the first stage of development.

Figure 5: Hermosa Project location map in Santa Cruz County, Arizona [Courtesy: South32]

The Project was the first mining project added to the United States Government’s FAST-41 permitting process, reflecting its strategic importance to domestic critical mineral supply. Federal permitting is progressing to schedule, with a Final Record of Decision and notice to proceed on track for H1 FY27.

Clark Battery-Grade Manganese Adds Long-Term Option Value

The Clark deposit is currently the only advanced project in the United States with a clear pathway to produce battery-grade manganese for the domestic electric vehicle market from locally sourced ore.

South32 has received two United States Government grants for Clark, including a US$20 million grant from the Department of War and a US$166 million grant from the Department of Energy.

A pre-feasibility study confirmed potential production of approximately 185,000 metric tons per annum of high-purity manganese sulphate monohydrate over an operating life of up to approximately 70 years.

S32 ASX Share Price

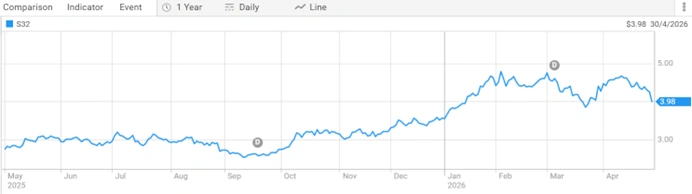

South32 Limited (ASX: S32) is currently trading at A$3.965 per share, with a market capitalisation of A$19.11 billion. The 52-week range stands at A$2.520 to A$4.910 per share.

Figure 6: South32 Limited (ASX: S32) share price performance over one year [Courtesy: ASX]

Industry Outlook

Global demand for zinc, lead, and silver continues to be underpinned by infrastructure development, energy storage, and industrial applications across key growth markets.

The critical minerals sector is attracting sustained strategic investment as governments, particularly in North America, prioritise domestic supply chains for battery materials and base metals.

Long-life, large-scale projects with established infrastructure access and multi-decade production profiles are increasingly attractive to institutional capital in this environment.

Future Direction and Impact on S32 Investors

For investors tracking South32 mining news, the Hermosa Project update removes a significant layer of uncertainty around the scale and quality of the Taylor asset.

South32 resource and reserve growth of 52% in Ore Reserves and 10% in Mineral Resources, combined with a 33-year mine life, confirms Taylor as a tier-one development among global zinc-lead-silver projects.

The revised capital of US$3,300 million is higher than the original estimate, but with approximately 80% of growth capital now invested, contracted, or subject to final pricing, the capital risk profile is materially lower.

The South32 mining project construction is progressing on two parallel fronts: decline access targeting first ore in mid-FY28 and shaft completion targeting first shaft production in H1 FY29.

With steady-state EBITDA of approximately US$650 million per annum and nameplate capacity expected from FY31, the question for investors now shifts from project definition to execution delivery.

ALSO READ: Resolution Minerals Produces High-Grade Tungsten Concentrate from Golden Gate Stockpiles

Frequently Asked Questions

Q1. What is the South32 Hermosa Project?

Ans. It is a 100%-owned regional-scale critical minerals project in Santa Cruz, Arizona, with the Taylor zinc-lead-silver project as its first development stage.

Q2. What is Taylor’s revised mine life?

Ans. Taylor’s initial operating life has been extended to approximately 33 years, up from approximately 28 years at final investment approval in February 2024.

Q3. Why has capital expenditure increased for Taylor?

Ans. The increase to approximately US$3,300 million reflects revised shaft construction costs, additional decline infrastructure, higher inflation, and United States tariff impacts.

Q4. When is first production expected at Taylor?

Ans. First production is expected in H2 FY28, with nameplate capacity of 4.3 million metric tons per annum targeted from FY31.

Q5. What is the expected steady-state EBITDA for Taylor?

Ans. South32 expects approximately US$650 million per annum at long-term price assumptions, rising to approximately US$800 million at spot prices as of April 2026.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or investment advice. All content is based on the ASX announcement released by South32 Limited on 30 Apr 2026. Share price and market capitalisation data reflect figures provided at the time of publication. Investing in securities involves risk. Readers should conduct their own research and seek independent financial advice before making any investment decisions. Colitco does not hold any position in the companies or organisations mentioned.

Sources

https://www.asx.com.au/markets/company/S32

Last modified: May 1, 2026