Mineral Resources Limited (ASX: MIN) has delivered a strong third-quarter performance for FY26, cutting net debt, lifting liquidity, and upgrading volume guidance across every major operating division. The results signal a company in the midst of a confident operational and financial turnaround, even as tropical cyclones tested its infrastructure.

Onslow Iron Powers Through Cyclone Season

Onslow Iron produced 7.8 million wet metric tonnes (wmt) and shipped 7.2 million wmt in Q3 FY26 on a 100% basis. Cyclones Mitchell and Narelle disrupted haulage, halting operations for three days in February and five days in March, but the private haul road and port infrastructure sustained zero damage.

Operations returned to nameplate capacity shortly after each weather event, demonstrating the resilience MinRes has built into Onslow Iron’s logistics chain.

Key operational highlights from the quarter include:

- 114 MinRes jumbo road trains averaged daily haulage runs to the Port of Ashburton

- Third-party contractor road trains were phased out entirely in mid-January

- The sixth transhipper, MinRes Lily, was delivered in China and is expected to arrive at Port Ashburton in May

- The seventh transhipper, MinRes Karri, remains on track for delivery by end of June

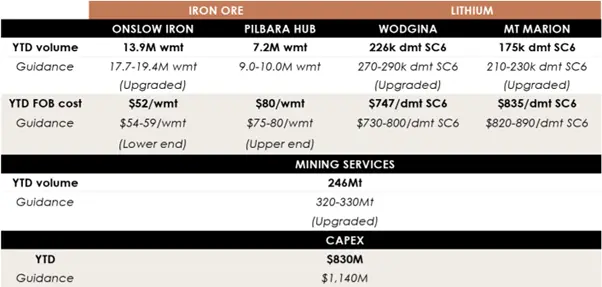

The average realised iron ore price for Onslow Iron came in at US$95/dmt, representing a 91% realisation of the Platts 61% CFR Index. The FOB cost for the quarter was $53/wmt.

MinRes upgraded Onslow Iron’s FY26 volume guidance to 17.7–19.4M wmt (previously 17.1–18.8M wmt), with costs tracking at the lower end of the $54–59/wmt guidance range.

Figure 1: FY26 Year-to-Date Performance and FY26 Attributable Guidance [Source: Mineral Resources Limited]

Pilbara Hub Transitions to Lamb Creek

The Pilbara Hub achieved a notable milestone in March, Lamb Creek’s first ore on ship. Project development is advancing on schedule, with the fly camp installed and works progressing on the permanent camp, a Great Northern Highway intersection, and a fixed crushing plant.

Production of 2.4M wmt exceeded shipped volumes of 2.1M wmt for the quarter, as MinRes deliberately builds inventory ahead of the full Lamb Creek transition.

Iron Valley continues to carry the load, accounting for 75% of shipped volumes in the quarter, up from 57% in Q2, with ore primarily sourced from the North Pit.

The average realised price for the Pilbara Hub was US$89/dmt, reflecting an 86% realisation of the Platts 61% CFR Index, boosted by a higher lump weighting of 42%.

FOB cost guidance for the full year is expected to land at the upper end of $75–80/wmt, with Q4 costs likely pressured by higher diesel prices. The Lamb Creek transition is expected to partly offset that.

Lithium Prices Surge: Wodgina and Mt Marion Upgraded

MinRes’s lithium operations delivered one of the standout results of the quarter. The combined attributable spodumene concentrate production across Wodgina and Mt Marion came in at 127k dry metric tonnes (dmt) SC6, with sales of 115k dmt SC6.

The average realised price across both sites soared to US$2,105/dmt CIF SC6 — a 92% increase quarter-on-quarter. That kind of price recovery reflects a meaningful shift in lithium market sentiment.

Wodgina

Wodgina produced 78k dmt, 8% lower quarter-on-quarter, due to a higher proportion of lower-grade Stage 3 ore, which pushed plant recoveries down slightly to 69%. An unplanned three-day gas supply outage caused by Cyclone Narelle also weighed on throughput.

The average realised spodumene price surged 87% qoq to US$2,130/dmt CIF SC6. SC6 FOB cost came in at $805/dmt, 12% higher due to lower volumes sold and reduced recoveries.

FY26 Wodgina volume guidance has been upgraded to 270–290k dmt SC6 (previously 260–280k dmt SC6), with cost guidance of $730–800/dmt SC6 held steady.

Mt Marion

Mt Marion produced 80k dmt, broadly flat on Q2. A trial of a dry high-intensity magnetic separator commenced in late March, if successful, it could increase both recovery rates and product grade, offering a meaningful production uplift.

The average realised price reached US$2,076/dmt CIF SC6, a 99% jump on the prior quarter.

FY26 Mt Marion volume guidance has been upgraded to 210–230k dmt SC6 (previously 190–210k dmt SC6), with cost guidance of $820–890/dmt SC6 maintained.

Mining Services Volumes Upgraded

MinRes’s mining services division processed 80Mt in Q3 FY26, 6% lower quarter-on-quarter, primarily reflecting the impact of reduced Onslow Iron volumes during the cyclone-affected period.

Despite the softer quarter, the full-year Mining Services production volume guidance has been lifted to 320–330Mt (previously 305–325Mt). Two external contracts were renewed during the quarter — covering crushing and haulage — with one contract completing.

Debt Comes Down, Liquidity Strengthens

MinRes made substantial progress on deleveraging in Q3:

- Net debt reduced to approximately $4.5 billion (from $4.9 billion at 31 December 2025)

- Liquidity strengthened to $1.8 billion (from $1.4 billion), comprising just under $1 billion in cash and a fully undrawn $800 million revolving credit facility

- Capital expenditure for the quarter was approximately $240 million

- The Onslow Iron carry loan balance fell to $459 million (from $553 million)

- The iron ore prepayment amortised to $440 million (from $500 million)

Post-quarter, MinRes issued US$1.3 billion in new Senior Unsecured Notes across two tranches, US$650M at 6.00% due May 2032, and US$650M at 6.25% due May 2034. The proceeds will be used to refinance higher-cost existing debt and fully repay the outstanding iron ore prepayment balance.

The POSCO Holdings transaction, announced in November 2025, remains subject to regulatory approvals. Once received, those proceeds are expected to retire the residual US$750M of Senior Unsecured Notes due October 2028.

Also Read: Saga Metals Trapper South Drilling Results Put the Project on the Radar

Exploration in Motion

MinRes completed 17 diamond drill holes (765m) at Onslow Iron during the quarter, focused on advancing geological understanding rather than resource definition.

At Wodgina, 5,327m of grade-control drilling was completed in Stage 3, alongside the commencement of a diamond drill program targeting underground resource definition.

In the Perth Basin, approvals were secured for the Ventoux-1 exploration well (expected completion in Q4 FY26), and site preparation has begun for the Aubisque-1 well.

Investors’ Outlook

MinRes shares closed at $63.51 on 30 April 2026 (3:45 pm AEST), up $1.63 (+2.63%) on the day, a move the market delivered almost in real time with the quarterly release.

The stock’s recent trajectory is hard to ignore:

| Period | Performance |

| 1 Week | +0.79% |

| 1 Month | +12.03% |

| 2026 YTD | +16.79% |

| 1 Year | +208.45% |

| vs Sector (1yr) | +167.96% |

| vs ASX 200 (1yr) | +202.69% |

Market Capitalisation: $12.55 billion

The investment case for MinRes is becoming clearer. The company is rapidly deleveraging, operationally resilient (the cyclone test proved that), and is now riding a meaningful lithium price recovery with volumes trending up. The POSCO deal, once closed, would remove a significant chunk of remaining debt.

Key things to watch heading into Q4 FY26:

- Commissioning of the sixth transhipper, MinRes Lily, at Port Ashburton

- Full ramp-up of Lamb Creek and its cost impact at the Pilbara Hub

- Diesel cost pass-through and whether FOB guidance holds

- Completion of the underground mining study at Mt Marion

- Finalisation of the Ventoux-1 well drilling in the Perth Basin

For investors already holding MIN, the deleveraging momentum and upgraded guidance offer reassurance. For those watching from the sidelines, the combination of a strengthening balance sheet, recovering lithium prices, and robust iron ore operations makes this a company worth tracking closely.

You may also find these articles relevant as you track activity across the broader resources sector: Resolution Minerals Produces High-Grade Tungsten and Atlas Salt’s Great Atlantic Project Showcases Modern Mining.

Frequently Asked Questions (FAQs)

Q1: What does Mineral Resources Limited do?

Mineral Resources Limited is a Western Australian diversified resources company operating across iron ore mining, lithium mining, engineering consulting, mining support services, and heavy industry. Its major operations include Onslow Iron, the Pilbara Hub, Wodgina, and Mt Marion.

Q2: Who owns or founded Mineral Resources Limited?

MinRes was founded by Christopher James Ellison MNZM, a New Zealand-born entrepreneur. Known as Chris Ellison, he built the company from a mining services business into one of Australia’s largest diversified resources companies and continues to serve as Managing Director.

Q3: What are the latest updates from Mineral Resources Limited?

In its Q3 FY26 report released 30 April 2026, MinRes upgraded volume guidance across all divisions, cut net debt to $4.5 billion, and strengthened liquidity to $1.8 billion. Lithium prices surged 92% quarter-on-quarter, Lamb Creek shipped its first ore, and a US$1.3 billion debt refinancing was completed post-quarter.

Q4: What does MinRes’s debt refinancing mean for investors?

Post-quarter, MinRes issued US$1.3 billion in new Senior Unsecured Notes at lower coupon rates of 6.00% and 6.25%, replacing higher-cost debt running at up to 9.25%. This extends the company’s debt maturity profile, reduces its annual interest burden, and, combined with the pending POSCO transaction, puts MinRes on a clear path toward a materially cleaner balance sheet over the next 12 to 24 months.

Disclaimer

This article is intended for informational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. The information presented is based on publicly available announcements made by Mineral Resources Limited (ASX: MIN) and other referenced sources as at 30 April 2026. Share price data and financial figures are subject to change. Past performance is not a reliable indicator of future results. Readers should conduct their own independent research and, where appropriate, seek advice from a licensed financial adviser before making any investment decisions. The author and publisher accept no liability for any loss or damage arising from reliance on the content of this article.

Sources

- https://clients3.weblink.com.au/pdf/MIN/03084255.pdf

- https://www.investing.com/news/transcripts/earnings-call-transcript-mineral-resources-q3-2026-sees-debt-refinancing-boost-93CH-4647538

- https://thewest.com.au/business/mining/mineral-resources-reduces-debt-and-increases-output-targets-after-onslow-iron-haul-road-survives-cyclones-c-22212894