In April 2026, one of the major brokers reassessed ANZ, Breville, and Macquarie shares and gave mixed recommendations to investors.

In accordance with the analysis, ANZ Group Holdings Ltd was given a sell rating despite its strong first-quarter performance, whereas Breville Group Ltd was given a buy call after it reported strong earnings.

In the meantime, a hold rating was given to the Macquarie Group Ltd on the basis of valuation issues.

These updates indicate the turn in the market mood in the banking, consumer appliances, and investment banking industries. The review is being undertaken in the changing economic conditions and investor apprehension within the ASX.

Investors track broker ratings across major ASX-listed companies. [Courtesy: The Australian]

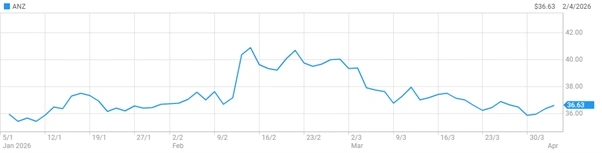

ANZ Shares Face Valuation Pressure Despite Strong Performance

ANZ Group Holdings Ltd exhibited a positive first-quarter performance, which was backed by cost cuts and better revenue flows.

The broker, however, insisted that the full-year cost outlook of the bank would not be more than 11.5bn, and therefore, the expectations would not be high.

Consequently, it was downgraded to sell, with the 12-month price target at $32.65. This is a warning to investors, even though share prices have been strong lately.

ANZ shares remain under scrutiny due to elevated valuation metrics. [ASX]

Why Is Breville Emerging As A Growth Favourite?

Breville Group Ltd is a good performer in the ANZ, Breville, and Macquarie shares analysis, with improved half-year results than expected. The firm registered a 10-digit sales growth of +10%, though the margin was hit by tariff pressure of about 130bp.

Nevertheless, net profit after tax grew by +1% on the previous corresponding period. Notably, the visibility of the FY26 EBIT growth guidance has been enhanced, which boosts investor confidence.

The broker placed a buy rating with the price target of $40.65, meaning that it will have a potential upward movement of about 50 per cent of the current price.

Breville gains investor attention with strong sales growth and an expansion strategy. [Courtesy: Shutterstock]

Macquarie Shares Hold Steady Amid Strong Market Performance

Macquarie Group Ltd provided a robust third-quarter update, and this has been backed by a strong performance in its market-facing businesses.

Commodities and Global Markets, as well as Macquarie Capital, posted outcomes that were significantly higher than the previous equivalent period. Improved guidance saw analysts increase FY26 and FY27 EPS forecasts by +2% and +4, respectively.

These gains are, however, partially counterbalanced by an increase in the expected FY26 tax rate.

The broker held a hold rating and revised price target of $223.00, which represented equal risk and reward at the current valuations.

What Does This Mean For Investors In April 2026?

The neutral perspective among ANZ, Breville, and Macquarie shares underscores the divergent trends in the sector on the ASX.

Banking stocks such as ANZ have a limitation in valuation despite improvement in operations, whereas consumer-oriented companies such as Breville enjoy expansion globally and product innovation.

Investment banks like Macquarie are still generating good profits, but the valuation issues put a cap on the upside. To investors, this is an indication that they should pick stocks selectively instead of having a broad market exposure.

The market environment is still under cost pressure, international demand and changing monetary expectations in Australia.

Market volatility drives selective investment strategies across ASX sectors. [Courtesy: InvestorPlace]

How Will Shares Perform Ahead?

In the future, ANZ, Breville, and Macquarie shares will tend to track sector-specific trends due to macroeconomic trends. ANZ can be subjected to further pressure unless it can achieve higher earnings growth than cost-cutting.

Breville seems to be in a good position to continue its growth, with geographical expansion and an innovation pipeline of products. Diversified business model helps Macquarie to be stable, but restricts the upside in the near term due to valuation.

Investors are advised to track updates of earnings, changes in guidance and indicators of the economy in the world to determine the future performance. The next couple of months may be critical in terms of positioning the portfolio in these large ASX stocks.

Also Read: ANZ Appoints New Leader for Business and Private Bank

FAQs

Q1. What happened with ANZ, Breville, and Macquarie shares?

A1: A broker issued updated ratings, assigning sell to ANZ, buy to Breville, and hold to Macquarie.

Q2. Why is Breville rated as a buy?

A2: Breville reported +10% sales growth and improved earnings visibility, supporting strong future potential.

Q3. Why are ANZ shares considered a sell?

A3: ANZ’s valuation metrics appear stretched despite stable operational performance and cost reductions.

Q4. What is Macquarie’s outlook for investors?

A4: Macquarie shows strong earnings growth but remains fairly valued, leading to a hold recommendation.

Disclaimer

This article is for informational purposes only and does not constitute financial advice. The analysis is based on publicly available information and broker commentary. Investors should conduct independent research or consult a licensed financial advisor before making decisions. Market conditions can change rapidly, and past performance is not indicative of future results. The companies mentioned may be subject to risks and uncertainties affecting outcomes.

Sources

- https://www.fool.com.au/2026/04/06/buy-hold-sell-anz-breville-and-macquarie-shares/

- https://www.macquarie.com/us/en/investors/2026-operational-briefing.html