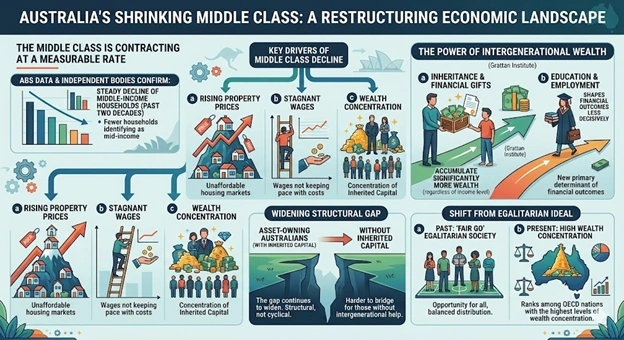

Australia’s middle class is contracting at a measurable rate, as property prices, stagnant wages, and the concentration of intergenerational wealth restructure the nation’s economic landscape. Research from the Australian Bureau of Statistics (ABS) and multiple independent economic bodies confirms that the share of households identifying as middle-income has declined steadily over the past two decades. The gap between asset-owning Australians and those without inherited capital continues to widen at a pace economists describe as structural, not cyclical.

The Grattan Institute reported that Australians who receive inheritances or financial gifts from family members accumulate, on average, significantly more wealth than those who do not — regardless of income level. The transfer of wealth between generations now shapes financial outcomes more decisively than education or employment. Australia, long regarded as an egalitarian society built on the “fair go” principle, now ranks among OECD nations with the highest levels of wealth concentration.

Figure 1: Australia’s shrinking middle class

Every Australian Feels This — Here Is Why

The erosion of the middle class affects every Australian who earns a wage, pays rent, services a mortgage, or raises children. Middle-income earners historically drove consumer spending, tax revenue, and social stability — and their decline signals a fundamental shift in how the Australian economy distributes opportunity. Workers in their 30s and 40s now face the prospect of never owning property in a capital city without direct financial assistance from parents or grandparents.

The implications extend beyond personal finance:

- Housing affordability collapses further as wealth concentrates among property-owning households

- Superannuation inequality deepens, as those with inherited assets supplement retirement savings while wage-only earners rely entirely on compulsory contributions

- Social mobility stalls, with educational outcomes, career networks, and geographic access increasingly tied to family wealth rather than individual merit

- Tax receipts shift, as capital gains and investment income — concentrated at the top — attract lower effective tax rates than wages

Australians without access to the “Bank of Mum and Dad” increasingly find themselves locked out of the asset ownership cycle that previous generations used to build financial security.

The Players Reshaping Australia’s Economic Order

The following groups sit at the centre of this structural economic shift:

- Middle-income wage earners aged 25–50, particularly those in non-capital-city regions, face the steepest decline in relative wealth accumulation

- Baby Boomers and older Gen X Australians, who hold the majority of residential property and superannuation balances, are the primary transferors of intergenerational wealth

- Millennials and Gen Z Australians without family assets are the cohort most acutely affected, with homeownership rates in this group falling to historic lows

- The Reserve Bank of Australia (RBA) and Treasury have both acknowledged the role of monetary policy — particularly prolonged low interest rates — in inflating asset prices and widening the wealth gap

- The Grattan Institute, the Australian Council of Social Service (ACOSS), and Per Capita have each published research documenting the structural retreat of middle Australia

- Federal and state governments face pressure to respond through taxation reform, housing policy, and wage legislation, though substantive reform remains limited

The “Bank of Mum and Dad” — parental financial support for home deposits — now functions as Australia’s ninth-largest mortgage lender by volume, according to research cited by the Financial Services Council.

Figure 2: Players reshaping Australia’s economic order

The Cities and Suburbs Where the Divide Cuts Deepest

The trend plays out across Australia’s major urban centres, with Sydney and Melbourne recording the sharpest divergence between asset owners and wage earners. Sydney’s median house price exceeded $1.1 million in 2024, placing outright purchase beyond reach for households earning the median income without supplementary capital. Melbourne, Brisbane, and Perth follow with rapid price-to-income ratio deterioration.

Regional Australia presents a more complex picture — property remains more accessible in some areas, but wage growth, employment diversity, and infrastructure investment lag behind capital cities. The net effect confines middle-class financial security to a narrowing band of geographic and demographic circumstances.

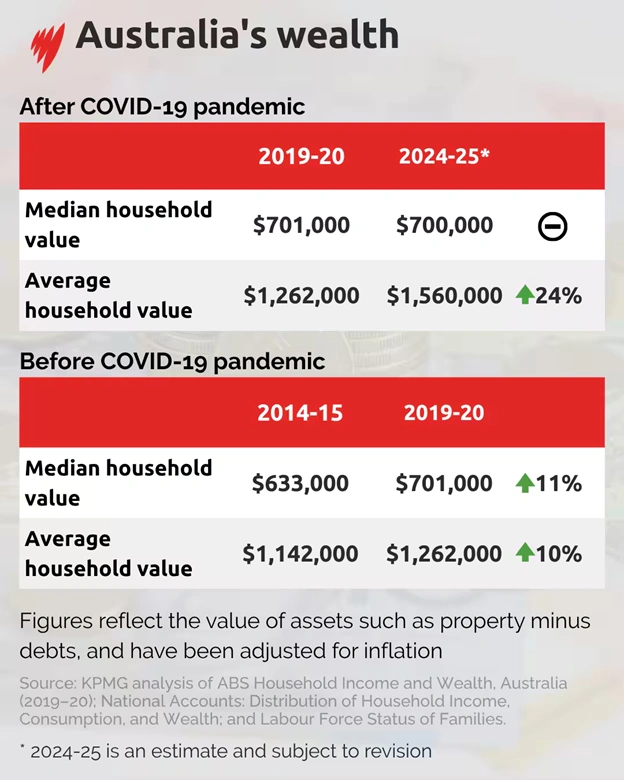

Figure 3: Average household wealth has skyrocketed since the start of the COVID-19 pandemic while median wealth has stagnated [SBS News]

Two Decades That Turned the Tide Against Wage Earners

Economists trace the acceleration of wealth concentration to the early 2000s, when residential property values began outpacing wage growth on a sustained basis. The 2008 Global Financial Crisis briefly disrupted asset price growth, but government stimulus and successive interest rate cuts from the RBA reignited property markets. Between 2012 and 2022, Australian residential property values doubled in real terms in most capital cities, while real wages grew by under 10 per cent over the same period.

The COVID-19 pandemic accelerated the divide further. The RBA cut the official cash rate to a historic low of 0.1 per cent in November 2020, driving another surge in asset prices. Homeowners accumulated hundreds of thousands of dollars in equity; renters accumulated nothing. By 2023, the wealthiest 20 per cent of Australian households held over 60 per cent of total net wealth, according to ABS data.

Also Read: Moderna Stock Climbs to Two-Month High on Hantavirus Vaccine Development News

The Mechanisms That Built the Divide — And What Comes Next

Several reinforcing mechanisms drove the dismantling of middle-class economic security in Australia:

- Negative gearing and capital gains tax discounts incentivised property investment over productive enterprise, channelling capital into existing housing stock

- Superannuation balances compounded inequality — those who entered the workforce earlier, or with higher incomes, accumulated exponentially greater retirement savings

- Wage theft, insecure employment, and the casualisation of the workforce depressed income growth for middle and lower earners across retail, hospitality, construction, and aged care

- University debt increased the cost of education without guaranteeing the wage premium that justified it in previous decades

- Rental markets tightened as investor demand absorbed available stock, pushing vacancy rates to sub-2 per cent levels in most capital cities by 2023–24

Looking forward, economists project the trend will entrench further unless governments intervene through targeted taxation of unearned wealth, land value tax reform, and large-scale social housing construction. Without structural policy change, Australia moves closer to a two-tier economy — one class that inherits assets, and one that services them.

The Productivity Commission noted in its 2021 report on wealth transfers that inheritances and gifts in Australia will grow to approximately $3.5 trillion over the next two decades — the largest intergenerational wealth transfer in the nation’s history. Those positioned to receive a share of that transfer will pull further ahead. Those outside the inheritance cycle will fall further behind.

Australia’s “fair go” identity now competes directly with the statistical reality of a nation where birth determines financial destiny more reliably than effort.

Disclaimer: This article is intended for informational purposes only. The statistics and data cited reflect publicly available research and reports at the time of publication. This article does not constitute financial, legal, or investment advice. Readers should seek independent professional advice before making financial decisions.

Sources

Tags: Australia's middle class, intergenerational wealth, wealth inequality Last modified: May 12, 2026