CSL Limited (ASX: CSL) released a significant financial update on 11 May 2026 from Melbourne, Australia. The update followed the completion of a 90-day business review by Interim Chief Executive Officer and Managing Director, Gordon Naylor, who stepped into the role in February 2026.

Figure 1: CSL signage displayed on the Company’s building exterior [Courtesy: API News]

The CSL FY26 financial update confirmed revised full-year guidance, additional non-cash asset impairments, and a series of leadership changes. Naylor and Chief Financial Officer Ken Lim presented findings to analysts and investors via a webcast investor call the same morning.

Revised Guidance Reflects Slower Financial Benefits From Growth Initiatives

CSL now expects FY26 revenue of approximately US$15.2 billion on a constant currency basis. The Company has also revised its NPATA guidance to approximately US$3.1 billion on a constant currency basis, excluding restructuring costs and impairments.

Gordon Naylor stated, “Our growth initiatives are working, but the financial benefits will take longer than previously anticipated to materialise. As a result, we have now revised down our 2026 financial year guidance.”

Three Headwinds Behind the Guidance Downgrade

The CSL FY26 financial update identified three specific revenue impacts driving the guidance revision:

- US Immunoglobulin: demand is growing at mid to high single digits, but reported revenue will reflect channel inventory normalisation, resulting in an approximately US$300 million revenue impact

- Albumin in China: while CSL’s market share has expanded and volumes have stabilised, market value has declined, resulting in an expected revenue impact of approximately US$200 million

- Other factors: the Middle East conflict, revised HEMGENIX growth, and iron competition collectively resulted in an expected revenue impact of approximately US$150 million

The Company confirmed it continues to expect CSL Behring revenue growth in the second half of FY26. CSL Seqirus is expected to perform moderately stronger than previously anticipated for the full year.

Approximately US$5 Billion in Additional Non-Cash Impairments Expected

Beyond the revised guidance, the CSL FY26 financial update disclosed that the Company expects to recognise approximately US$5 billion in non-cash, pre-tax impairments across FY26 and FY27. This is in addition to the US$1.5 billion already recognised at the first-half FY26 results.

The additional impairments cover CSL Vifor intangible assets, including the product portfolio, as well as under-utilised property, plant and equipment. These figures remain subject to further analysis, business developments, external audit, and Board approval.

Full-Year Results to Provide Next Update on Impairments

The Company confirmed the next update on impairments will be provided at the full-year results announcement, scheduled for 18 August 2026. The CSL investment outlook remains focused on rebuilding long-term value through disciplined capital allocation and focused operational execution.

Interim CEO Review Identifies Strengths and Accelerates Execution Plan

The 90-day review completed by Naylor assessed the business across portfolio growth, operating model efficiency, and capital allocation. The review found CSL making progress on key transformation initiatives, though outcomes had fallen short of investor expectations.

Figure 2: Gordon Naylor, Interim Chief Executive Officer and Managing Director of CSL Limited [Courtesy: CSL Limited]

Naylor stated, “CSL’s culture and people continue to be first class, the industry is stable and growing and the Company has evident strengths in plasma collections and influenza vaccines. I am confident that the Company can be returned to profitable growth and my work is to position the business and the next CEO for success.”

Key Transformation Progress Noted Across the Business

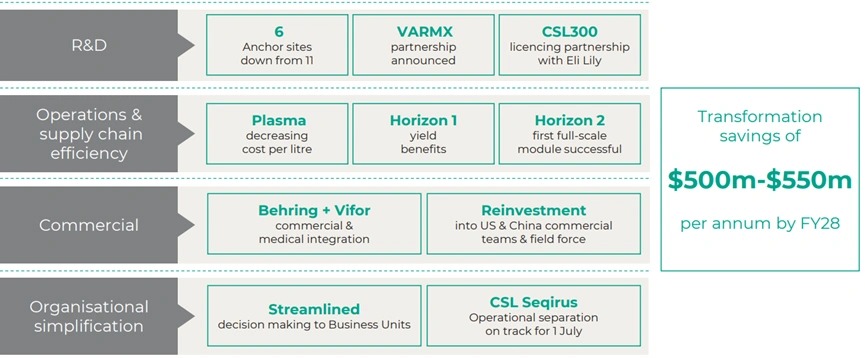

The review identified meaningful progress across several areas of the transformation programme:

- R&D anchor sites reduced from 11 to 6, with a VARMX partnership announced and a CSL300 licensing partnership executed with Eli Lilly

- Plasma cost per litre is decreasing, with Horizon 1 yield benefits and a successful Horizon 2 first full-scale module

- CSL Seqirus operational separation remains on track for 1 July 2026

- Commercial and medical integration of Behring and Vifor is progressing, with reinvestment into the US and China commercial teams

- Transformation savings are targeted at US$500 million to US$550 million per annum by FY28

Figure 3: Key transformation initiatives and savings targets outlined in CSL’s interim CEO 90-day review presentation [Courtesy: CSL Limited]

Leadership Changes Confirmed as CEO Search Progresses

The CSL stock forecast 2026 outlook is also shaped by several leadership developments confirmed in this announcement. Chief Commercial Officer Andy Schmeltz has decided to retire from CSL for personal reasons.

Naylor noted, “CSL thanks Andy for his important contribution to the Company and conveys its best wishes to him and his family.”

Diego Sacristan will assume the Chief Commercial Officer role for CSL Behring and CSL Vifor, effective 1 July 2026. Sacristan brings deep commercial experience, having previously led CSL Behring’s US business and international markets.

Board and Global Leadership Team Updated

The global search for a new Chief Executive Officer is progressing as planned. Following the appointment and transition of the new CEO, Gordon Naylor is expected to remain on the CSL Board as a Non-Executive Director. Steve Marlow, Executive Vice President of CSL Plasma, has been appointed to the Global Leadership Team.

CSL ASX Share Price

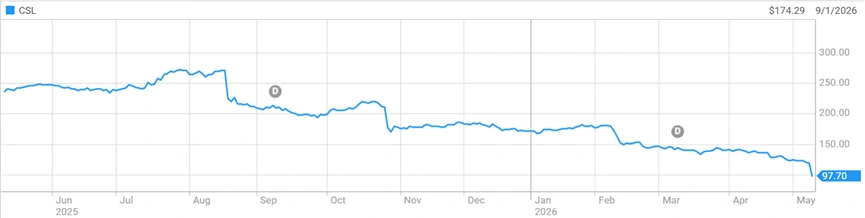

CSL Limited (ASX: CSL) is currently trading at A$97.820 per share, with a market capitalisation of A$57.41 billion. The 52-week range stands at A$93.640 to A$275.790 per share.

Figure 4: CSL Limited (ASX: CSL) share price performance on the ASX following the FY26 financial update announcement [Courtesy: ASX]

Industry Outlook

The global biopharmaceutical sector continues to face a complex operating environment, shaped by pricing pressures, evolving regulatory frameworks, and intensifying competition across plasma-derived and specialty therapeutics.

Companies with diversified product portfolios, strong plasma collection networks, and credible transformation programmes are best positioned to navigate near-term headwinds.

The CSL investment outlook benefits from a stable underlying demand environment in immunoglobulin therapies, with the addressable patient population still significantly underserved across primary and secondary immune deficiencies.

Future Direction and Impact on CSL Shareholders

The outcomes of the CSL FY26 financial update carry clear near-term implications for investors monitoring the CSL stock forecast 2026:

- FY26 revenue guidance revised to approximately US$15.2 billion on a constant currency basis

- FY26 NPATA guidance revised to approximately US$3.1 billion on a constant currency basis, excluding restructuring and impairments

- Approximately US$5 billion in additional non-cash, pre-tax impairments expected across FY26 and FY27, subject to Board and auditor approval

- US Immunoglobulin channel inventory normalisation expected to create approximately US$300 million revenue impact in FY26

- CSL Behring revenue growth expected in the second half of FY26

- CSL Seqirus operational separation on track for 1 July 2026

- Transformation savings target of US$500 million to US$550 million per annum by FY28

- Full-year results and next impairment update scheduled for 18 August 2026

- Global CEO search progressing, with Gordon Naylor to remain on the Board as Non-Executive Director post-transition

Frequently Asked Questions

Q1. What did the CSL FY26 financial update announce on 11 May 2026?

Ans. CSL revised its FY26 guidance, now expecting revenue of approximately US$15.2 billion and NPATA of approximately US$3.1 billion on a constant currency basis.

Q2. Why was the CSL FY26 guidance revised downward?

Ans. Three key headwinds were cited: US Immunoglobulin channel inventory normalisation, declining market value for Albumin in China, and the combined impact of the Middle East conflict, HEMGENIX, and iron competition.

Q3. What is the CSL investment outlook for the rest of FY26?

Ans. CSL expects CSL Behring revenue growth in the second half of FY26 and moderately stronger performance from CSL Seqirus. The Company targets transformation savings of US$500 million to US$550 million per annum by FY28.

Q4. Who is the new Chief Commercial Officer of CSL?

Ans. Diego Sacristan will assume the Chief Commercial Officer role for CSL Behring and CSL Vifor from 1 July 2026, succeeding Andy Schmeltz who is retiring for personal reasons.

Q5. When will CSL provide its next full update?

Ans. Detailed financial and operational performance will be provided at the full-year results announcement scheduled for 18 August 2026.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or investment advice. All content is based on the ASX announcement and investor presentation released by CSL Limited on 11 May 2026. Share price and market capitalisation data reflect figures provided at the time of publication. Investing in securities involves risk, including the possible loss of principal. Readers should conduct their own research and seek independent financial advice before making any investment decisions. Colitco does not hold any position in the companies or organisations mentioned.

Sources

- https://www.asx.com.au/markets/company/CSL

- https://www.csl.com/investors

- https://data-api.marketindex.com.au/api/v1/announcements/XASX:CSL:3A693022/pdf/inline/interim-ceo-90-day-review-and-financial-update

Last modified: May 12, 2026