Rio Tinto Ltd (ASX: RIO) shares pushed higher on Tuesday after the mining giant dropped its first-quarter 2026 operations review, and investors liked what they saw. The stock climbed to $173.46, up 0.55% on the day, and now sits within striking distance of a record high.

The gains cap off a remarkable run. Rio Tinto shares have surged 18.14% year-to-date and a staggering 55.51% over the past 12 months, comfortably outperforming the ASX 200 by 41.46 percentage points over that same period. With a market capitalisation of approximately $64.5 billion, the company remains one of the most dominant names on the Australian exchange.

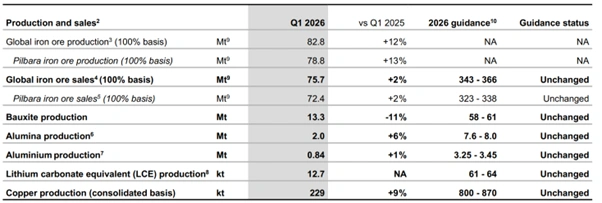

Figure 1: Rio Tinto Q1 2026 Operations Snapshot. Iron ore production rises 12% to 82.8 Mt, while sales remain steady at 75.7 Mt. Copper output grows 9%, but bauxite production declines 11%. Full-year guidance across key segments remains unchanged. [Rio Tinto]

The Rio Tinto Q1 results 2026 painted a picture of operational strength across the board — copper, iron ore, and aluminium all delivered, even as cyclones, geotechnical headaches, and a tragic fatality at Kennecott tested the business.

Also Read: Rivco Australia Posts Record Profit and Board Reshape in 2025

Copper Drives the Headline Number

9% Year-on-Year Growth in Copper Equivalent Production

The standout figure from the Rio Tinto Q1 results 2026 was a 9% year-on-year increase in copper equivalent (CuEq) production, the metric the company uses to measure overall portfolio performance across its diverse commodity mix.

Copper itself led the charge, with consolidated production reaching 229,000 tonnes, up 9% on Q1 2025. The key driver was Oyu Tolgoi in Mongolia, which delivered 101,600 tonnes of copper in concentrates, a 56% jump year-on-year, as the underground ramp-up continues to track ahead of expectations.

CEO Simon Trott noted the mine’s trajectory remains on plan to average around 500,000 tonnes per year from 2028 to 2036.

Meanwhile, Resolution Copper in Arizona hit a significant milestone. The congressionally mandated land exchange between Resolution Copper and the US federal government was completed in March, following a court ruling in Rio Tinto’s favour. Drilling is now underway, unlocking access to what the company describes as one of the world’s largest untapped copper deposits. Rio Tinto plans to invest approximately $500 million (its share: $275 million) over two years in enabling works at the site.

Those following Resolution Minerals’ recent antimony trioxide production developments will recognise how significant copper project milestones like this can move markets.

Iron Ore: Record Pilbara Output, But Cyclones Bite Shipments

Second-Highest Q1 Pilbara Production Since 2018

The Pilbara operations delivered the second-highest Q1 production since 2018, pumping out 78.8 million tonnes (100% basis), a 13% increase on the prior year. Investment in mine health, productivity improvements, and fewer weather-related disruptions during the production phase drove the result.

However, two tropical cyclones, Mitchell in February and Narelle in March, disrupted shipments by approximately 8 million tonnes. Rio Tinto expects to recover around half of those losses in Q2.

Total Pilbara iron ore sales came in at 72.4 million tonnes (100% basis), up 2% year-on-year despite the shipping disruption.

Key sales metrics from the quarter include:

- 25% of sales were made on a free on board (FOB) basis

- SP10 represented 12% of total sales, consistent with Q4 2025

- Portside sales in China totalled 2.6 Mt, down sharply from 8.6 Mt in Q1 2025

- End-March portside inventory sat at 6.6 Mt, including 3.2 Mt of Pilbara product

Full-year Pilbara iron ore sales guidance remains unchanged at 323–338 Mt.

Simandou Makes History

Rio Tinto also celebrated a historic milestone at its Simandou project in Guinea. The first full SimFer shipment of high-grade iron ore successfully reached China during the quarter, with first sales realised in April. The project’s common rail infrastructure reached full commissioning in Q1 2026, and Rio Tinto now expects a 30-month ramp-up to full production rates during the second half of 2028.

Aluminium Holds Firm Despite Weather Disruptions

Integrated Value Chain Shows Its Strength

Rio Tinto’s aluminium business demonstrated exactly why vertical integration matters. Despite record rainfall at Weipa in January and February, the worst in a decade, and a shutdown at Gove and Weipa caused by Cyclone Narelle, the company kept its production guidance unchanged.

Here’s how the aluminium segment performed in Q1 2026:

- Bauxite production: 13,281 kt; down 11% YoY due to weather impacts

- Alumina production: 2,038 kt; up 6% YoY (QAL now included at 100%)

- Primary aluminium production: 835 kt; up 1% YoY

The Kitimat smelter in British Columbia continued its ramp-up following improved hydrological conditions, while New Zealand’s Tiwai Point maintained high production rates following its full ramp-up in Q4 2025.

On a major community and industrial note, the Queensland and Australian Governments jointly committed to a $2 billion funding package to extend the Boyne Smelters Limited (BSL) operation at Gladstone through to at least 2040. That’s a significant win for regional Queensland.

Tariff costs across US-bound shipments actually decreased in Q1, reflecting lower total volumes shipped to the US (273 kt versus 303 kt in Q4 2025).

Lithium: Growth Projects Hit Their Marks

Fenix 1B and Sal de Vida Reach Mechanical Completion

The Rio Tinto Q1 results 2026 also confirmed two major lithium milestones. Both the Fenix 1B expansion in Catamarca, Argentina, and the Sal de Vida project achieved mechanical completion as planned. First production from both remains on track for H2 2026.

Total lithium carbonate equivalent (LCE) production for the quarter was 12.7 kt, with lithium carbonate prices continuing to rally, up 45% across Q1 2026 from $14,500/t to $21,000/t, driven by growing expectations of tightening supply and strong Battery Energy Storage System (BESS) demand.

The Rincon starter plant in Argentina is also progressing well, ramping up and delivering higher output than the previous quarter.

Productivity Programme Delivering on Promise

Rio Tinto’s “stronger, sharper, simpler” transformation programme hit a significant milestone. The company confirmed that the first $650 million of annualised benefits is now fully implemented, achieved as promised by March 2026.

The benefits span operational improvements, right-sizing central functions, and streamlining non-operational costs. Management says substantially more improvements are now underway, focused on throughput, operating costs, and central overhead reductions.

Market Context: Macro Tailwinds Supporting Commodity Prices

Middle East Conflict Reshaping Supply Chains

The outbreak of conflict in the Middle East has introduced volatility across Rio Tinto’s key commodity markets — but the company’s diversified portfolio has largely absorbed the disruption.

- Copper hit a record high of $6.28/lb in late January before pulling back to $5.52/lb at quarter end, and has since recovered to $6.00/lb by mid-April

- Aluminium rallied to near four-year highs in March, with the US Midwest duty-paid premium reaching a record $2,523/t as Middle East smelter curtailments removed significant ex-China supply

- Lithium carbonate surged 84% quarter-on-quarter to average $19,427/t in Q1

China’s real GDP growth accelerated from 4.5% YoY in Q4 2025 to 5% in Q1 2026, supported by industrial production strength. The US continued to benefit from an AI capital expenditure boom, driving demand for future-facing commodities.

Investors keeping an eye on the broader resources sector, particularly those interested in BHP dividend income as a passive income strategy, will note that the macro environment underpinning Australian miners remains constructive heading into the second half of 2026.

Share Price Snapshot (ASX: RIO) — 21 April 2026

| Metric | Value |

| Last Price | $173.46 [as at 1:30 pm 21/04 (AEST)] |

| Change (Day) | +$0.95 (+0.55%) |

| 1 Week | +0.81% |

| 1 Month | +18.06% |

| 2026 YTD | +18.14% |

| 1 Year | +55.51% |

| vs Sector (1yr) | +4.93% |

| vs ASX 200 (1yr) | +41.46% |

| Market Cap | ~$64.5 billion |

What to Watch From Here

The Rio Tinto Q1 results 2026 leave the company tracking well against its full-year production and cost targets. All guidance remains unchanged across every major commodity. The cyclone-related shipment shortfall in iron ore creates a modest headwind for Q2 top-line numbers, but half those volumes are expected to be recovered.

Resolution Copper drilling outcomes, the Simandou ramp-up trajectory, and further news on the Nemaska Lithium Bécancour optimisation review will be the key project-level watch points in the coming months.

With the share price now flirting with all-time highs and the underlying business firing on most cylinders, the Rio Tinto Q1 results 2026 have given shareholders plenty of reasons to feel confident heading deeper into the year.

Also Read: Resolution Minerals Advances Antimony Trioxide Production

Disclaimer:This article is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future returns. Please consult a licensed financial adviser before making investment decisions.