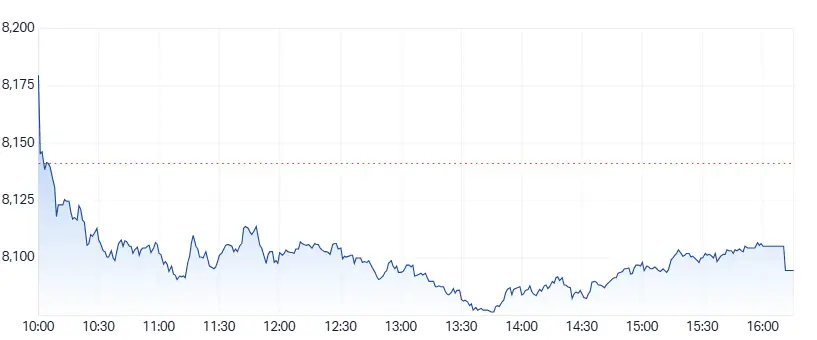

Energy ASX 200 Declines for Third Consecutive Session

The S&P/ASX 200 closed down 0.57% on Thursday, losing 46.40 points to finish at 8,094.70. The index has now fallen for three straight sessions, setting a new 20-day low. Over the past five days, the index has declined by 2.10%, though it remains stable year-to-date. Seven out of 11 sectors finished in negative territory, led by energy stocks.

The broader All Ordinaries Index declined 0.44% to 8,326.40. The index’s Small Ordinaries Index gained 0.50% to 3,094.40, showing resilience in smaller companies. The ASX All Technology Index was one of the few bright spots, rising 0.46% to 3,747.70.

Figure 1: ASX 200 Chart

Sector Performance

The energy sector was the worst performer, falling 3%, with Woodside Energy down 5.34%. Beach Energy, Ampol, and Santos also declined, despite a slight increase in crude oil prices. The materials sector gained 0.4%, driven by strong performances from gold miners. West African Resources led the rally after reporting a 49% increase in full-year profit.

The ASX 200 VIX, a measure of market volatility, rose 2.49% to 12.96, reaching a one-month high. Investors remained cautious amid global economic uncertainty and mixed commodity price movements.

Market Winners and Losers

Top Gainers:

- Resolute Mining (ASX: RSG): +7.59% ($0.43)

- Cochlear Ltd (ASX: COH): +4.59% ($275.38)

- St Barbara Ltd (ASX: SBM): +4.35% ($0.24)

- Bellevue Gold Ltd (ASX: BGL): +7.35% ($1.315)

- Orthocell Ltd (ASX: OCC): +7.20% ($1.265)

Biggest Decliners:

- Appen Ltd (ASX: APX): -9.03% ($1.31)

- Mesoblast Ltd (ASX: MSB): -8.33% ($2.20)

- Clinuvel Pharmaceuticals (ASX: CUV): -7.52% ($12.05)

- Novonix Ltd (ASX: NVX): -5.68% ($0.415)

- Smartgroup Corporation Ltd (ASX: SIQ): -5.34% ($7.98)

A total of 580 stocks advanced, 482 declined, and 451 remained unchanged on the Sydney Stock Exchange.

Major Corporate Developments

Commonwealth Bank completed the sale of its remaining 4.4% stake in Vietnam International Commercial Joint Stock Bank for $170 million. Rio Tinto finalised its acquisition of Arcadium Lithium, which has stopped trading on the index. The company also announced a $2.8 billion investment in its Brockman iron ore project.

Bannerman Energy reported a first-half loss per diluted share of AU$0.0168, improving from AU$0.041 in the prior year. Revenue surged to AU$2.3 million from AU$871,000. Capricorn Metals reported a 20% decline in first-half profit, citing lower gold production and higher operating costs.

Executive and Leadership Changes

Air New Zealand announced CEO Greg Foran will step down in October. The company has started a global search for his successor. Inghams Group appointed Matthew Easton as the new head of New Zealand operations. Michael Hill named Andrew Lowe as interim CEO following Daniel Bracken’s passing.

Ratings Adjustments

Citi upgraded Cochlear and Integral Diagnostics from ‘neutral’ to ‘buy’. Analysts cited valuation grounds for the decision, as both stocks had declined significantly after recent earnings reports. E&P Capital initiated coverage on uranium producers Boss Energy and Paladin Energy, expressing a positive mid-term outlook. Citi downgraded ARB Corporation from ‘buy’ to ‘neutral’ due to near-term market concerns.

Commodities and Currency Market

Gold futures rose 0.05% to $2,927.59 per ounce. Crude oil climbed 0.56% to $66.68 per barrel, while Brent crude increased 0.56% to $69.69 per barrel. The Australian dollar remained steady, with AUD/USD at 0.63 and AUD/JPY gaining 0.17% to 94.52. The US Dollar Index dipped 0.04% to 104.21.

Outlook

The index remains under pressure amid global economic uncertainty and volatility in commodity markets. Investors continue to monitor inflation data, central bank policies, and corporate earnings reports for further direction. Market sentiment may remain cautious, with upcoming economic data releases likely to influence short-term movements.