The BHP operational review for June 2026 dropped on 16 July with a familiar headline. Record iron ore. A second straight year near two million tonnes of copper. Read past that front page, though, and the more useful story is about what comes next.

Iron ore mining amounted to 265 million tonnes in the year ended 30 June. This was only slightly more than last year. The copper production was recorded at 1.95 million tonnes, representing a fall of 3 per cent.

On paper, a slight miss. In the bank, a fat win. Copper sold for about 35 per cent more than a year earlier.

The realised copper price hit US$5.74 a pound. That single number did most of the heavy lifting.

Record output leaned on the copper price, not more copper

Here is the part that rewards a careful read. BHP produced less copper than the year before, yet copper again ran the show for earnings. Higher prices, not higher volumes, carried the result.

New chief executive Brandon Craig, in his first review since taking the top job on 1 July, said every asset was tracking inside its unit cost guidance despite inflation, dearer diesel and supply chain knocks.

Cost control was the quiet achievement of the year. Escondida, Spence and Copper South Australia all sat at the bottom end of their cost ranges.

So the operating machine hummed. The rock, less so.

Escondida is digging more to get less

Escondida is the tell. BHP’s flagship Chilean mine set a record for material mined, up 4 per cent, and a record for concentrator throughput. It still produced 3 per cent less copper.

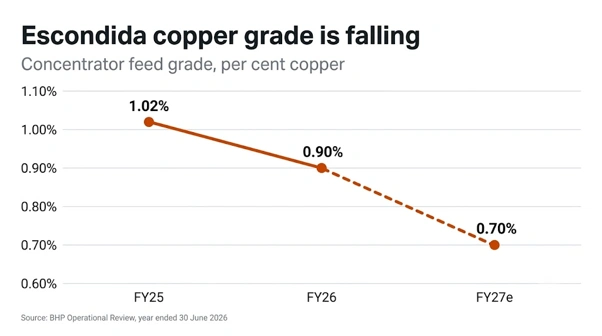

Escondida’s falling copper grade explains why record digging still means less metal.

The reason is grade. There will be a reduction in the grade of copper ore feed to the concentrator to 0.90 per cent against 1.02 per cent recorded in last year. In the coming year, the figure is projected to reduce further to 0.70 per cent.

That is why the forward guidance carries a warning. This is against the current expectation by BHP of a total copper production of 1,650 to 1,800 kilotonnes in FY27 as against the almost two million tonnes in this year.

Concerning Escondida, there will be a production of 1,000 to 1,100 kilotonnes, which is a massive reduction from its FY26 production.

The record year, in other words, comes just before a leaner one. That is the depletion treadmill in plain sight. You run faster to stay in roughly the same place, then slip back anyway.

The June 2026 operational review flags a softer copper year and a costly potash bet

The Jansen potash project is the bruise on this report. BHP expects to book an impairment of about US$2.3 billion against the Canadian mine in its full-year accounts.

Stage 2 has blown out from US$4.9 billion to US$6.9 billion. First potash from Stage 1 is now due around the middle of 2027.

Net debt at 30 June sat near US$9 billion.

Potash was meant to be the fourth leg of the portfolio, a fresh commodity to sit beside iron ore, copper and coal. It still might be. But it has cost more and taken longer than the pitch promised, and the write-down puts a hard figure on that gap.

Craig framed Jansen as a decades-long play. Fair enough. The market is less patient. Shares slid about 5.6 per cent on the day the cost blowout first landed in June.

Ministers North shows the cheaper side of BHP’s spending

Set against Jansen, one line in the review reads like relief. North Ministers iron ore project in the Pilbara region has been approved by BHP with an investment of US$0.9 billion in 100 per cent terms.

The project is expected to generate extra 20 million tonnes per year and will utilize the Yandi existing infrastructure. It will generate a return of more than 30 per cent.

First ore is expected in FY29. A bolt-on that leans on kit already in the ground is exactly the sort of spend that keeps iron ore cheap to run.

That contrast, a lean brownfield tonne versus a runaway greenfield build, is the real capital allocation lesson buried in this document.

A fresh knock also turned up. In July, an underground conveyor belt failed at Carrapateena in South Australia.

No one was hurt, but the fix could cost up to eight weeks of production. Small in the scheme of things. Worth watching all the same.

The coal book, often the forgotten corner, quietly delivered. BMA lifted steelmaking coal 3 per cent on its highest stripping volumes in five years. NSW energy coal beat the top of its guidance range.

FY26 production snapshot

- Iron ore: 265 Mt, up 1 per cent, a record

- Copper: 1,952.8 kt, down 3 per cent

- Steelmaking coal (BMA): 18.6 Mt, up 3 per cent

- Energy coal (NSWEC): 16.4 Mt, up 9 per cent

- FY27 copper guidance: 1,650 to 1,800 kt

The full picture arrives on 18 August, when BHP releases its financial results and the Jansen charge gets locked into the accounts. That report will also set the dividend, which is where most shareholders will look first.

For background, we have tracked BHP’s copper-versus-iron-ore transition, its stronger-than-expected March quarter update, the China iron ore trade pressure squeezing its main market, and the Samarco dam disaster ruling still hanging over the group.

The read on this operational review is straightforward. A strong finish, banked at good prices, sitting on top of a copper grade problem and a potash bill that keeps growing. Records look good in a headline. The grade table tells you where the pressure lands next.

Also Read: SKS Technologies Data Centre Contract Puts $312m on the Books

FAQs

Q: Did BHP hit record production?

A: Yes, record iron ore at 265 million tonnes.

Q: Why is BHP’s FY27 copper guidance lower?

A: Falling ore grade at Escondida, dropping to about 0.70 per cent.

Q: How big is the Jansen impairment?

A: About US$2.3 billion, before and after tax.

Q: When are BHP’s full-year results due?

A: 18 August 2026.

Disclaimer:

This article is for general information only and does not constitute financial or investment advice. It does not account for your personal circumstances. Always do your own research and consult a licensed financial adviser before making investment decisions. Investing in shares carries risk, including loss of capital.

Source:

Elizabeth Jones is a finance and mining content specialist with over 10 years of experience creating clear, SEO-driven content across fintech, investing, banking, insurance, cryptocurrency, and resource markets. She transforms complex financial data and industry trends into engaging, reader-focused articles that improve understanding and audience engagement.