Right now, income investors are staring at two names and asking the same question. Which of these best ASX mining stocks for dividend income actually holds up when the cycle turns?

Figure 1: The Australian Securities Exchange (ASX) in Sydney [Courtesy: Business Times]

Fortescue Ltd (ASX: FMG) and Rio Tinto Limited (ASX: RIO) are not interchangeable bets. They share the Pilbara, they share iron ore exposure, and they both appear in conversations about ASX mining shares passive income 2030. But the similarities start to thin out fast once you look under the hood.

What the March Quarter Results Actually Show

Both companies released their most recent quarterly production results within days of each other. The numbers tell two different stories about operational momentum.

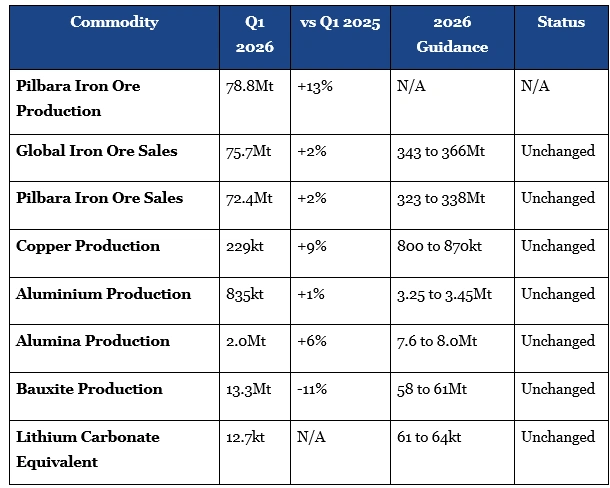

Rio Tinto Q1 2026 Production and Sales Summary

Iron Ore: Both Are Strong, One Has More Complications

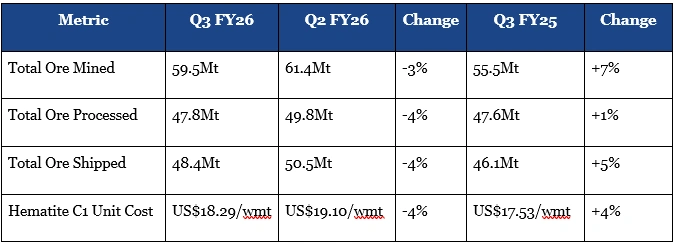

Fortescue’s Record Shipments Come With a Weather Footnote

Fortescue’s nine-month shipment record is real and hard to dismiss. There is, however, a complication sitting inside the headline. Iron Bridge Concentrate shipments were 2.0Mt in Q3 FY26, impacted by weather disruptions from Tropical Cyclones Mitchell and Narelle.

Figure 2: Fortescue Ltd (ASX: FMG), one of Australia’s largest iron ore producers [Courtesy: Fortescue Ltd]

Iron Bridge guidance for the full year has been amended from 10 to 12Mt previously down to a range of 9 to 10Mt, on a 100 per cent basis.

Fortescue Operations Summary: Q3 FY26

Volumes on a 100 per cent basis unless stated otherwise.

Hematite C1 unit cost for the quarter came in at US$18.29/wmt, four per cent lower than Q2 FY26. The hematite realised price was US$92/dmt, representing 89 per cent of the average Platts 61% CFR Index.

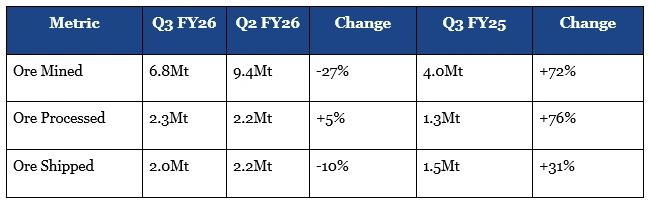

Iron Bridge Operations: Q3 FY26

Volumes on a 100 per cent basis. Fortescue holds a 69 per cent equity share of Iron Bridge.

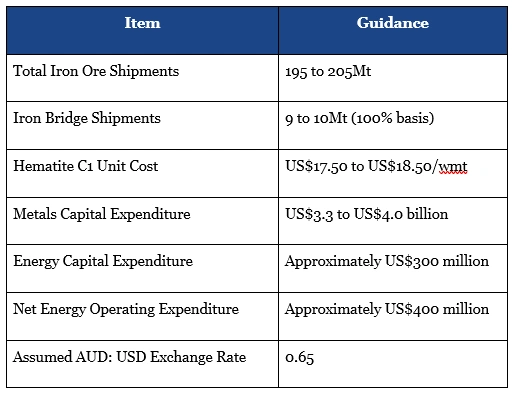

Fortescue FY26 Guidance Summary

Rio Tinto’s Pilbara Volume Is Strong Despite Cyclone Impact

Rio Tinto had a strong start to 2026 in the Pilbara. Q1 production was the second-highest for any first quarter since 2018. Two cyclones cut into shipments by around 8Mt, but the

Company expects to recover roughly half of that in the coming months. Sales came in at 72.4Mt for the quarter, up 2 per cent on the same time last year. Full-year Pilbara sales guidance of 323 to 338Mt stays as is.

Figure 3: A haul truck at Rio Tinto [Courtesy: Rio Tinto]

Copper C1 net unit cost guidance for Kennecott, Oyu Tolgoi, and Escondida is US65 to US75 cents per pound.

The Commodity Mix: Where the Two Really Diverge

This is the part of the Fortescue vs Rio Tinto dividend yield Australia conversation that matters most for income beyond 2030.

Fortescue is still overwhelmingly an iron ore business. Green energy and green metal are serious strategic directions, not yet revenue-generating at scale. The Company is targeting first hot metal at the Green Metal Project at Christmas Creek in the June Quarter 2026.

Fortescue has commenced construction of the 133MW Nullagine Wind Project and the 440MW Solomon Airport solar farm, expected to become Western Australia’s largest solar development.

Figure 4: Fortescue’s wind energy infrastructure under construction [Courtesy: Fortescue Ltd]

Additionally, a US$680 million investment has also received Board approval to develop 200MW of firmed green energy in the Pilbara, positioning the Company to meet growing industrial demand, including from data centres.

Under the Green Grid programme, Fortescue is building a combined 2.3GW of renewable generation capacity comprising 1.5GW of solar and 800MW of wind, firmed by more than 5GWh of batteries.

Rio Tinto already generates significant revenue from five commodity groups. In the first quarter of 2026 lithium carbonate equivalent production was 12.7kt, and mechanical completion had been achieved for both Fenix 1B and Sal de Vida.

Figure 5: Rio Tinto’s corporate office [Courtesy: The Wall Street Journal]

Moreover, Rio Tinto also completed the historic land exchange at Resolution Copper in Arizona in March 2026, with drilling now underway at one of the world’s largest untapped copper deposits.

For an investor thinking about passive income, this commodity spread is not a minor detail. It is the whole argument.

The Dividend Outlook

Fortescue’s Income Appeal

Fortescue ended the March quarter with a cash balance of US$4.2 billion, down from US$4.7 billion at the end of December 2025. The movement is not surprising. The Company paid out a US$1.3 billion interim dividend during the quarter and spent US$915 million on capital expenditure. Net debt sat at US$1.6 billion and gross debt was US$5.8 billion as on 31 Mar 2026.

Rio Tinto’s Steadier but Lower Yield

Rio Tinto’s earnings base is broader, and the dividend stream reflects that. The Company had implemented US$650 million of annualised productivity benefits by March 2026, with further improvements underway across throughput, operating costs, and central costs. Pre-tax exploration and evaluation expenditure in Q1 2026 was US$180 million.

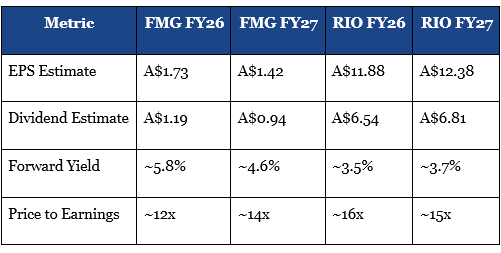

Fortescue vs Rio Tinto: Earnings and Dividend Estimates

Fortescue’s yield is the headline number for income investors evaluating Fortescue vs Rio Tinto dividend yield Australia. Rio Tinto’s yield is lower, but its earnings are drawn from a wider set of commodities. That distinction matters most when iron ore has a difficult year.

Copper, Lithium, and the Road to 2030

Anyone genuinely thinking about best ASX mining stocks for dividend income over a five-year horizon should be thinking about where earnings will come from when iron ore disappoints.

Fortescue completed the acquisition of Alta Copper in March 2026, securing the Cañariaco Copper Project in Northern Peru for approximately US$70 million, at C$1.40 per share and an implied total equity value of approximately C$139 million.

Share Price Snapshot

Fortescue Ltd (ASX: FMG)

- Last price: A$20.53 per share

- Market capitalisation: A$64.71 billion

- 52-week high: A$23.38 per share

- 52-week low: A$14.31 per share

Rio Tinto Limited (ASX: RIO)

- Last price: A$184.58 per share

- Market capitalisation: A$69.93 billion

- 52-week high: A$195.84 per share

- 52-week low: A$100.75 per share

Industry Outlook

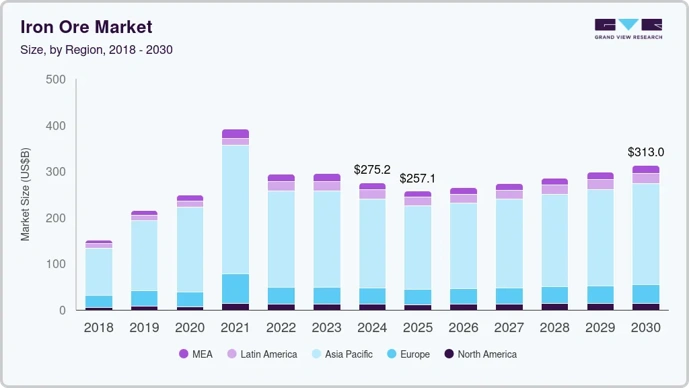

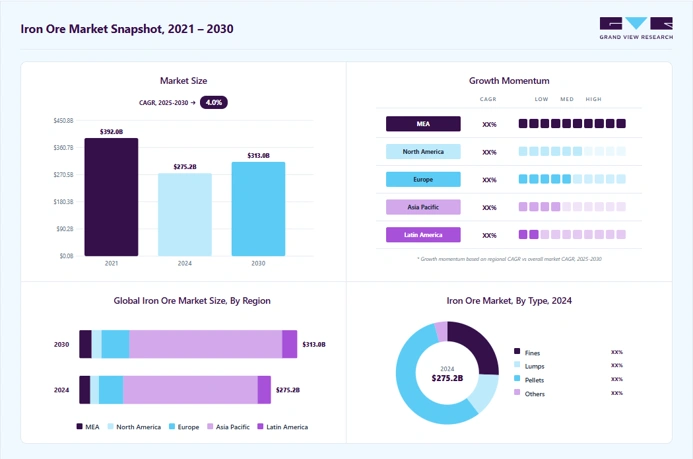

Iron ore is not going anywhere soon. The global market was worth US$275.23 billion in 2024 and is expected to reach US$313.02 billion by 2030, growing at 4.0 per cent per year. Asia Pacific drives the bulk of that demand, holding a 70.0 per cent revenue share in 2024.

Figure 6: Global iron ore market projected [Courtesy: Grand View Research]

More than 71 per cent of the regional share came from China alone. Pellets continued to be the largest type of product with a revenue share of 56.3 per cent, and steel was the most commonly used end use by far. The steady demand floor is driven by population growth in emerging economies, urbanisation, and infrastructure spending.

Figure 7: Global iron ore market size by region from 2018 to 2030 [Courtesy: Grand View Research]

Future Direction and Impact on Dividend Sustainability

The trajectory for both companies points in different directions, and the impact on income reliability heading into 2030 is real.

Fortescue’s green energy investments are genuinely ambitious. If green metal production scales and green energy becomes a revenue stream rather than only a cost item, Fortescue’s earnings profile could broaden materially.

The Company expects full completion of its Pilbara green grid by the end of 2028 and intends to replicate the technology commercially wherever it is invited. For now, the income investor is essentially buying iron ore cash flows and waiting to see if the green transition adds to them over time.

Rio Tinto’s copper ramp-up at Oyu Tolgoi, the Resolution Copper land exchange in Arizona, the lithium projects in Argentina and Canada, and the Simandou iron ore Project in Guinea together create a more layered earnings picture heading into the back half of this decade.

The first full SimFer shipment of high-grade Simandou product was successfully delivered to China in Q1 2026, with first sales realised in April. For investors evaluating mining Companies passive income 2030, Rio Tinto’s broader base offers more paths for earnings to hold up even if iron ore softens.

ALSO READ: St George Mining Welcomes ATL as Shareholder Following Lithium Star JV Restructure

FAQ

Q1. What is Fortescue Ltd on the ASX?

Ans. Fortescue Ltd trades on the Australian Securities Exchange under the ticker FMG. It is one of the world’s largest iron ore producers, headquartered in Perth, Western Australia.

Q2. How does Fortescue vs Rio Tinto dividend yield Australia compare right now?

Ans. Fortescue is forecast to yield approximately 5.8 per cent in FY26, compared to approximately 3.5 per cent for Rio Tinto, based on current consensus estimates.

Q3. What happened to Iron Bridge shipments in Q3 FY26?

Ans. Iron Bridge Concentrate shipments were impacted by Tropical Cyclones Mitchell and Narelle.

Q4. Is Rio Tinto producing copper and lithium already?

Ans. Yes. Rio Tinto produced 229kt of copper and 12.7kt of lithium carbonate equivalent in Q1 2026.

Q5. Which is the better pick for ASX mining shares passive income 2030?

Ans. Rio Tinto’s diversified commodity base gives it more earnings pathways if iron ore softens. Fortescue offers a higher yield today but carries more single-commodity risk.

Disclaimer

This article is meant only for informational purposes. If you are an investor who is watching Fortescue or Rio Tinto closely, all the data published in the content is sourced from ASX announcements and external sources. Kindly verify all the information related to the share price and market data. Any investment should be made at the investor’s own risk. Colitco does not hold any position in the above-mentioned companies.

Sources

https://www.fool.com.au/2026/06/08/are-fortescue-or-rio-tinto-shares-the-better-buy/

https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-03082072-6A1321851&v=undefined

https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-03080661-3A691691&v=undefined

https://www.grandviewresearch.com/industry-analysis/iron-ore-market-report

https://www.asx.com.au/markets/company/RIO

https://www.asx.com.au/markets/company/FMG

https://www.un.org/development/desa/pd/content/world-population-prospects

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.