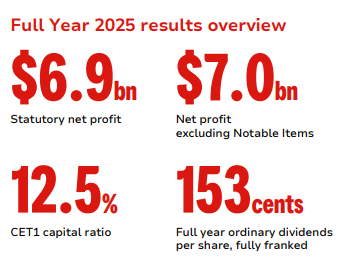

Westpac Banking Corporation (ASX:WBC) announced a statutory net profit of $6.9 billion for the 2025 financial year. The bank’s net profit, excluding notable items, sat just above $7.0 billion. These results reflect Westpac’s strategic balance of growth and returns across its business operations.

Westpac’s result overview for FY 2025

Solid Growth Across Deposits and Loans

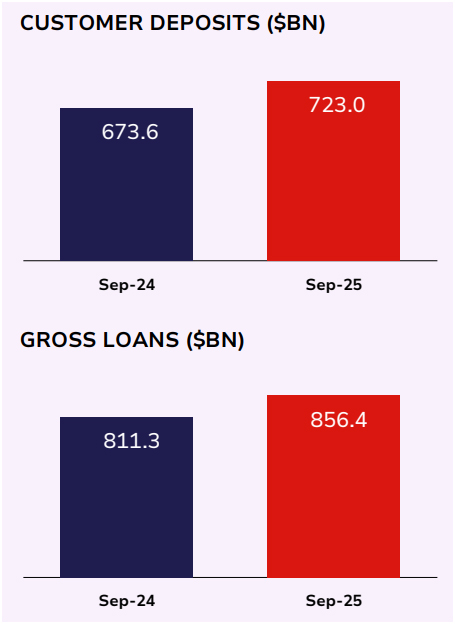

Westpac’s total deposits rose by 7%, reaching $723 billion, while gross loans grew by 6% to $856 billion by September 2025. Consumer deposits increased by 10%, supported by rises in both business and institutional deposits. Business lending surged 15%, with targeted sectors like agriculture, health, and professional services leading growth. Institutional lending expanded 17%, boosted by increased infrastructure and energy projects. Housing loans, excluding RAMS, grew by 5%, predominantly from owner-occupied mortgages.

Strong Capital and Funding Position

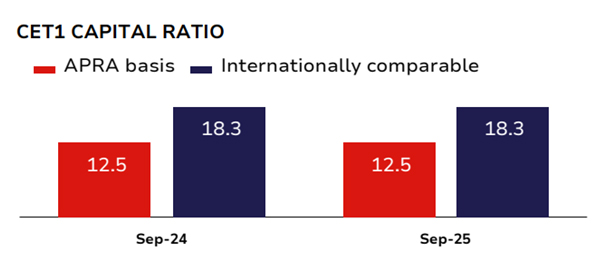

The bank’s Common Equity Tier 1 (CET1) capital ratio maintained a healthy 12.5%, exceeding the target ratio of 11.25%. Westpac held capital $3.1 billion above its target after dividend payments. Funding and liquidity metrics such as the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) remained above regulatory minimums. The deposit-to-loan ratio improved by 1.37 percentage points, reflecting deposit growth funding loan increases.

Westpac’s CET1 Capital Ratio overview

Operating Income and Expenses

Westpac reported a 3% increase in net interest income, driven by growth in interest-earning assets. Non-interest income rose by 5%, propelled by fee income, markets, and wealth management services. Operating income climbed 4% in the second half compared to the first half of 2025. However, operating expenses increased by 9%, impacted by a $273 million restructuring charge to support the Fit for Growth productivity program. Excluding this charge, expenses grew 4%, mainly from higher staff costs and investment in technology through the UNITE transformation program.

Credit Quality Improves

Credit impairment charges decreased to $424 million, representing 5 basis points of average gross loans. This improvement reflected fewer new individually assessed provisions alongside increased recoveries. The ratio of collectively assessed provisions to credit risk-weighted assets decreased to 1.25%. Stressed exposures declined from 1.45% in 2024 to 1.28% in 2025, indicating better credit quality across business segments.

Scroll Down for FULL FINANCIAL SUMMARY

Dividends and Shareholder Returns

Westpac declared fully franked ordinary dividends of 153 cents per share for the year, representing a payout ratio of 76% of net profit. The bank paid a final dividend of 77 cents per share, sustaining its commitment to shareholder returns while balancing growth and capital requirements.

Outlook Reflects Gradual Economic Improvement

Westpac anticipates that the Australian economy will improve gradually, supported by a shift from public to private sector growth. It expects GDP growth of around 2.1% in 2025 and 2.4% in 2026. The unemployment rate is predicted to stabilise near 4.5%. Housing credit growth is forecast at approximately 6.6% in 2025 and 6.5% in 2026. Business credit demand remains healthy, especially among larger enterprises, with expected growth rates of 9.0% in 2025 and 7.2% in 2026. The New Zealand economy is recovering more slowly, with credit growth of 6.3% expected in 2026.

Strategic Priorities Focus on Customers and Transformation

Westpac outlined five strategic priorities to achieve its ambition of being customers’ top bank and partner. The bank focuses on simplifying banking experiences across digital and branch channels, enhancing customer service, and expanding local expertise. It actively invests in digital platforms including BizEdge and Westpac One to improve service delivery. The bank continues transforming its risk culture and controls through the CORE program to enhance resilience.

The UNITE program aims to simplify legacy technology and operations. Westpac targets cost reductions and improved efficiency through this program while maintaining disciplined risk management. The bank measures performance by market position and return on tangible equity, prioritising sustainable growth and cost discipline.

Also Read: ASX Starts Week Lower Despite Oil Gains and Bank Results

Financial Summary and Key Figures

- Statutory net profit: $6.93 billion (2025), down 1% from 2024

- Net profit excluding notable items: $6.97 billion, down 2%

- Net interest income: $19.38 billion, up 3%

- Non-interest income: $3.0 billion, up 6%

- Operating expenses: $11.92 billion, up 9%

- Credit impairment charges: $424 million, down 21%

- CET1 capital ratio: 12.5%

- Deposits: $723 billion, up 7%

- Gross loans: $856 billion, up 6%

- Fully franked dividends: 153 cents per share, payout ratio 76%

Second Half 2025 Highlights

In the second half of 2025, Westpac posted net profit excluding notable items of $3.52 billion, a 2% increase from the first half. Net interest income grew 4%, driven by lending growth and improved net interest margins. Non-interest income rose 10% on stronger Markets and fee income. Operating expenses increased 9%, impacted by restructuring costs. Credit impairments fell to 4 basis points of average loans, with fewer new provisions.