Qantas Airways Limited (ASX: QAN) released a significant market update on 14 Apr 2026. The Company revised its second-half FY26 outlook in response to a sharp rise in jet fuel costs following the escalation of the Middle East conflict.

Figure 1: Qantas Airways aircraft in flight with official livery [Courtesy: Qantas Airways]

The airlines fuel cost impact from the crisis has moved well beyond original guidance. Yet the update also carries an offsetting story: international demand has strengthened, domestic yields are holding, and the Group’s financial position remains sound heading into the second half.

A Surging Fuel Bill Rewrites the Second-Half Cost Outlook

Qantas reported its 1H26 results in late February 2026, at which point 2H26 fuel costs were guided at approximately A$2.5 billion. That figure has since been overtaken by a spike in jet refining margins triggered by the conflict.

Jet refining margins surged from approximately US$20 per barrel in February to a peak near US$120 per barrel. The revised 2H26 fuel estimate now stands at A$3.1 to A$3.3 billion, based on forecast consumption of approximately 16.1 million barrels. The implied increase from original guidance represents A$600 to A$800 million in additional cost pressure for the half.

Hedging Cushions the Crude Side, But Refining Margins Remain Exposed

Qantas confirmed approximately 90% of its 2H26 crude oil exposure is already hedged. This has provided meaningful insulation on the commodity price side of the airlines fuel cost impact.

However, the Group remains largely exposed to refining margins, and it is this component that drove the revision higher. Qantas noted it is monitoring fuel supply closely, with government and supplier engagement supporting confidence in continued availability through April and into May.

Revenue Growth Offers a Meaningful Offset

The revenue picture in the update is considerably more constructive than the fuel revision alone suggests. Group International unit revenue growth for 2H26 is now expected at 4 to 6%, double the prior guidance range.

Middle East airspace closures and multiple carriers suspending services have redirected travellers toward alternative routings through Australia and Asia. Qantas responded by redeploying capacity from the United States network to increase services to Paris and Rome from Perth. Group Domestic unit revenue growth for 2H26 is expected at approximately 5%, rising to 6% in the fourth quarter of FY26.

The Middle East Crisis Creates a Two-Speed Outcome Across the Group

The market update highlights a clear divergence between the Qantas and Jetstar brands. Qantas International capacity is growing 9% in 4Q26 versus the prior corresponding period, supported by premium demand and the Europe rerouting tailwind.

Jetstar International, by contrast, is contracting meaningfully, with capacity down 7% in 4Q26. Jetstar’s budget-sensitive leisure customers are more exposed to cost-of-living pressure and geopolitical uncertainty, while Qantas full-service travellers are relatively price-inelastic.

Capacity Discipline Applied to the Domestic Market

Qantas applied a 5% domestic capacity reduction in 4Q26. This has supported domestic yields by tightening the available supply of seats against steady demand.

For investors tracking Australian airlines performance 2026, this approach reflects a deliberate strategy to preserve unit revenue across both the domestic and international portfolios during a period of elevated cost pressure.

Capital Discipline and Balance Sheet Management in a Volatile Environment

Qantas confirmed FY26 capital expenditure is now expected to come in at A$4.1 billion or below. This is the bottom of the previously guided A$4.1 to A$4.3 billion range and reflects the Group’s decision to preserve financial flexibility.

The planned A$150 million on-market share buyback, announced at the 1H26 result, has not yet commenced and has been paused pending clarity on the evolving environment. Net debt is expected to be at or above the midpoint of the A$5.6 to A$7.0 billion target range at 30 June 2026.

Interim Dividend Proceeds Unchanged

The A$300 million fully-franked interim dividend of 19.8 cents per share remains unchanged and was paid on 15 Apr 2026. FY26 depreciation and amortisation is expected to be approximately A$2.25 billion, with transformation savings of approximately A$400 million targeted in FY26 to offset cost pressures.

Charges expected to be taken outside underlying earnings in 2H26 are approximately A$110 million, including Jetstar Asia closure costs and restructuring costs.

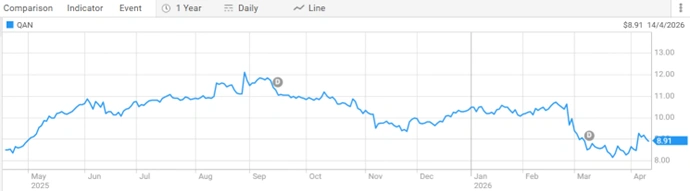

QAN ASX Share Price

Qantas Airways Limited (ASX: QAN) is currently trading at A$8.915 per share, with a market capitalisation of A$13.63 billion. The 52-week range stands at A$8.035 to A$12.620 per share.

Figure 2: Qantas (ASX: QAN) share price performance over one year [Courtesy: ASX]

Industry Outlook

Global aviation is navigating one of its most complex operating environments in recent years. Airlines fuel cost impact from the Middle East conflict has reshaped second-half cost structures across the industry, while simultaneously creating demand tailwinds for carriers with strong Europe and premium networks.

For investors assessing the best airline stocks 2026, the key variable is the duration of the refining margin spike. If margins normalise as Gulf energy infrastructure is restored, today’s cost pressure may prove transitory. Carriers with strong hedging programmes, premium demand exposure, and diversified route networks are best positioned to recover.

Future Direction and Impact on QAN Investors

The Qantas share price forecast and broader QAN investor thesis will be shaped by several moving parts in the months ahead. The key items to monitor from the 14 Apr 2026 update are:

- Revised 2H26 fuel cost estimate of A$3.1 to A$3.3 billion, up from A$2.5 billion at the 1H26 result

- Approximately 90% of 2H26 crude oil exposure is hedged; refining margin exposure remains open

- Group International unit revenue guidance doubled to 4 to 6% growth for 2H26

- Group Domestic unit revenue expected to grow approximately 5% in 2H26 and 6% in 4Q26

- FY26 capital expenditure tightened to A$4.1 billion or below

- The A$150 million share buyback has been paused pending further clarity

- Net debt expected at or above the midpoint of the A$5.6 to A$7.0 billion target range at 30 June 2026

- FY27 guidance will be provided at a later date given ongoing volatility

For those watching the best airline stocks 2026, Qantas enters the second half with a materially higher fuel bill but also with stronger-than-expected international revenue, a hedged cost base, and a resilient balance sheet.

ALSO READ:Resolution Minerals Unveils Significant Scale Potential at Antimony Ridge with Advanced 3D Modelling

Frequently Asked Questions

Q1. What is the updated Qantas fuel cost estimate for 2H FY26?

Ans. Qantas revised its 2H26 fuel cost estimate to A$3.1 to A$3.3 billion, up from approximately A$2.5 billion guided at the 1H26 result in February 2026.

Q2. How is Qantas managing the airlines fuel cost impact?

Ans. Approximately 90% of 2H26 crude oil exposure is hedged. The Company is also using fare increases, route changes, and capacity adjustments to partially offset the higher fuel bill.

Q3. Has Qantas changed its dividend or buyback plans?

Ans. The A$300 million interim dividend of 19.8 cents per share was paid on 15 Apr 2026 and remains unchanged. The A$150 million share buyback has been paused pending clarity on the evolving environment.

Q4. What is the Qantas share price forecast outlook for FY26?

Ans. Analysts had a consensus target near A$12.19 before the update. The current share price of A$8.915 represents a significant discount to that level, with the fuel cost revision and market volatility the primary headwinds.

Q5. Is QAN considered one of the best airline stocks 2026?

Ans. Qantas has strong hedging, a growing international premium network, and a solid balance sheet. Investors should conduct their own research and seek independent financial advice before making any investment decisions.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or investment advice. All content is based on publicly available sources including the Qantas market update released on 14 Apr 2026 and supplementary reporting. Share price and market capitalisation data reflect figures provided at the time of publication. Investing in securities involves risk, including the possible loss of principal. Readers should conduct their own research and seek independent financial advice before making any investment decisions. Colitco does not hold any position in the companies or organisations mentioned.

Sources

https://stocksdownunder.com/investing-in-qantas-in-2026/

https://www.asx.com.au/markets/company/QAN

Last modified: April 15, 2026