Australia’s retail liquor and pub hospitality sector rarely makes headlines for the right reasons. But on 27 May 2026, Endeavour Group Limited (ASX: EDV) gave investors something worth paying attention to. At its Investor Day in Sydney, the Company laid out a comprehensive reset strategy, one developed through difficult choices and honest priorities while acknowledging where the business had lost momentum.

Figure 1: Endeavour Group CEO and Managing Director Jayne Hrdlicka [Courtesy: Point Hacks]

This review was led by the CEO and Managing Director, Jayne Hrdlicka, on behalf of the Board. They found three areas in which Endeavour Group had drifted away from what made its brands strong. The strategy announced addresses all three and sets the Company up for sustainable, long-term growth throughout its Retail and Hotels divisions.

Among ASX company strategy announcements made this year, this one stands out for the level of detail provided and the frank admission of where the business had underperformed.

Three Priorities Driving the EDV Growth Strategy

Endeavour Group’s refreshed strategy is built around three clear priorities. Each one targets a part of the business that the strategic review found underperforming.

1. Resetting the Retail Strategy Across Dan Murphy’s and BWS

Endeavour Group identified price leadership as the cornerstone of the Dan Murphy’s brand. The Company admitted it had drifted, prioritising margin expansion at the expense of customer trust. The plan now is to restore the “lowest liquor price guarantee” positioning and compete vigorously across every customer touchpoint.

Figure 2: Dan Murphy’s retail liquor store exterior [Courtesy: AFR]

The website attracts more than 3.5 times the visits of its next largest competitor, according to SimilarWeb data cited in the presentation. These are strong assets. The Company believes it has not been using them well enough.

BWS, positioned as “Your Local for Convenience with a Twist,” has 1,451 stores around Australia. It saw a 40 per cent growth in its digital traffic in F25, while its orders are delivered within an average of about 34 minutes.

Since launching in May 2024, there are around 4.6 million active members, and since then, the Appy Deals program has generated nearly A$580 million in total sales at BWS. So the strategy here is to localise range and improve the digital experience, but also build on customer engagement platforms.

2.Accelerating Investment in the ALH Hotels Portfolio

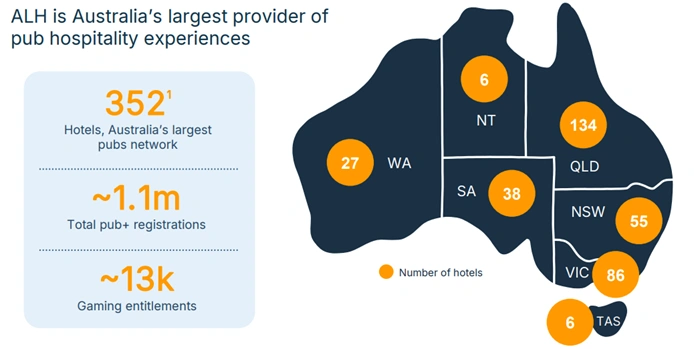

ALH Hotels is Australia’s largest pub hospitality network, operating 352 hotels across every state and territory. The total addressable Hotels market sits at approximately A$34 billion, spanning pub and bar food, beverages, gaming machines, and accommodation. The gaming segment alone represents approximately A$18 billion in market size.

Figure 3: ALH Hotels market overview across food, beverages, gaming, and accommodation [Courtesy: Endeavour Group]

Endeavour Group’s Hotels strategy for the ASX EDV growth plan has been too focused on cost control. The new approach flips that. The Company plans to accelerate renewals, targeting 50 to 60 hotel renewals per year at steady state, up from 25 in F24 and 27 in F25. The targeted year-two return on investment for renewals is greater than 15 per cent.

Figure 4: ALH Hotels national network footprint and pub+ membership statistics [Courtesy: Endeavour Group]

The pub+ loyalty program, launched in August 2024, has already reached approximately 1.1 million registrations. About 35 per cent of food and beverage transactions at ALH venues now flow through pub+ users. That first-party data is central to the Hotels growth strategy.

3. Simplifying Operations and Cutting Costs

The third pillar of the Endeavour Group ASX growth strategy is operational simplification and cost reduction. The Company is targeting approximately A$300 million in cost savings to be delivered by F29, including approximately A$100 million in F27 alone. This comes on top of the A$300 million in cumulative savings already delivered between F22 and F26.

Cost levers include right-sizing support functions, operational productivity improvements, end-to-end process simplification, procurement and supply chain optimisation, and site cost reduction. Additionally, the Company is progressing its technology separation from Woolworths through the One Endeavour program.

On the asset side, Endeavour Group is exiting the majority of its winery and vineyard portfolio. This includes Chapel Hill, Oakridge, and Josef Chromy. The Pinnacle Drinks business is being repositioned as a private label operation in service of the Retail brands, with three core wineries retained for scale winemaking.

About Endeavour Group

Endeavour Group Limited is one of Australia’s largest retailers and hospitality operators. The Company operates through two primary segments, Retail and Hotels. The Retail division runs 1,737 stores nationally, covering Dan Murphy’s and BWS across destination, neighbourhood, and drive-through formats.

The Hotels division includes 352 venues nationally via ALH Hotels. The Company also owns Pinnacle Drinks, an exclusive brand and private label business. The registered office of Endeavour Group is located at Level 3, 10 Shelley Street, Sydney NSW 2000. In 2021, the Company was admitted to trade on the Australian Securities Exchange after it demerged from Woolworths Group.

Capital Management and Dividend Policy

It revised its dividend payout ratio to a range of 50 per cent to 75 per cent of the Group underlying Net Profit After Tax. The previous ratio sat higher. The shift is about more flexible funding in the investment stage, not under a financial strain.

Total committed debt facilities weighted average maturity of 4.3 years at A$2.65 billion as at 30 April 2026. Another A$300 million of bank facilities start from June 2026. Leverage is expected to be elevated in F26 and F27 as investment accelerates.

The medium-term target is less than 2.0 times EBITDA on a pre-AASB 16 basis. The balance sheet is supported by more than A$1 billion in freehold property and a portfolio of tradeable hotel businesses.

EDV Share Price and Market Data

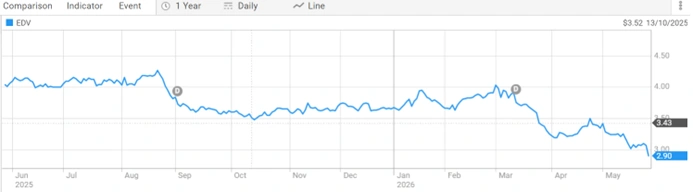

Endeavour Group (ASX: EDV) last traded at A$2.965 per share. For those tracking the ASX EDV share price forecast Australia, the stock is sitting near its 52-week low.

Figure 5: Endeavour Group (ASX: EDV) share price chart [Courtesy: ASX]

Any EDV stock forecast ASX analysts put forward from here will hinge on whether the cost reduction targets and hotel renewal program deliver on schedule.

Retail Liquor and Hospitality in Australia

The Australian retail liquor and pub hospitality sector is big and growing. For example, the total addressable market for ALH Hotels is approximately A$34 billion, and this includes food and beverages, gaming machines, and accommodation alone.

This is a story of numbers; they tell quite an interesting one when it comes to retail liquor. Luxury wine from A$25 to A$50 grew at a 7.0 per cent two-year sales compound annual growth rate for F23 to FY25. Mid-strength beer again tracked the moderation trend at 5.6 per cent. Premix and ready-to-drink products were at 3.5 per cent growth. Customers are still heavily involved with the category.

g

g

Figure 6: Customers socialising at a pub venue [Courtesy: Endeavour Group]

The pub market is also moving. Food and beverage is growing at around 3 per cent per year. Gaming is at 5 per cent, with sustained spend across the eastern states. Accommodation is the standout, growing at 7 per cent as post-COVID travel habits hold firm.

Digital is reshaping everything. Having big, very engaged user bases and clean first-party data is becoming the true competitive moat. In that context, the 9 million active members and around 180 million retail customer touchpoints of Endeavour Group are real assets.

Future Direction and Impact on Investors

The strategy plays out in three phases. F26 and F27 are about getting the basics right: restoring price leadership, cutting costs, and lifting hotel investment. F27 and F28 shift to building the growth platform. F28 to F30 is where the returns are expected to follow.

For shareholders, the revised dividend policy gives the business room to invest without being squeezed. The A$300 million cost reduction target provides a credible earnings tailwind regardless of top-line performance.

Hotel renewals targeting greater than 15 per cent year-two returns are capital-efficient if the program delivers at scale. For the broader sector, Endeavour Group returning to price competitiveness will lift pressure on every competitor in the category.

ALSO READ: Auric Mining Expands Munda Gold Resource by 32% as Starter Pit Outperforms Expectations

FAQs

Q1. What is Endeavour Group’s new strategy about?

Ans. A Retail reset, Hotels investment push, and A$300 million in cost cuts by F29.

Q2. Why is Endeavour Group selling its wineries?

Ans. To simplify Pinnacle Drinks and focus it on private label only.

Q3. What changed with the EDV dividend policy?

Ans. The payout ratio is now 50 per cent to 75 per cent of the underlying Net Profit After Tax.

Q4. How large is the ALH Hotels network?

Ans. 352 hotels nationally, Australia’s largest pub network.

Q5. What is the current EDV share price?

Ans. A$2.965 per share, with a market cap of approximately A$5.53 billion.

Disclaimer

This article is meant only for informational purposes. If you are an investor who is watching Endeavour Group closely, all the data published in the content is sourced from ASX announcements and the Company’s Investor Day presentation dated 27 May 2026. Kindly verify all the information related to the share price and market data. Any investment should be made at the investor’s own risk. Colitco does not hold any position in the above-mentioned company.

SOURCES

https://webcast.openbriefing.com/edv-inv-2026/

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.