The Australian share market is known for its heavy reliance on the resources industry. When major miners move, the entire index tends to follow their lead. However, over the past 12 months, one of these blue-chip mining companies has far outperformed the overall market. This company is Fortescue Ltd (ASX: FMG), a leading iron ore producer.

This article provides a deep Fortescue stock surge 12-month return analysis to see how much a modest investment grew. We will also look at what drove these massive gains.

The Raw Numbers: Turning $10,000 into a Fortune

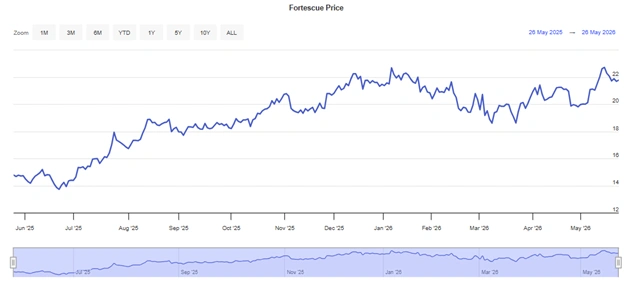

If you had invested $10,000 into Fortescue exactly one year ago, you would be looking at a very healthy brokerage account today. Over the past 12 months, the Fortescue share price has surged by approximately 40%. This is a massive return for a large blue-chip company.

The initial $10,000 investment would now be worth $14,000. That represents a clear $4,000 gain in capital alone.

Figure 1: Fortescue 12-month share price momentum from May 2025 to May 2026 [Credit – Fool]

This performance looks even more impressive when compared to the rest of the Australian share market. The benchmark S&P/ASX 200 Index rose by only about 4% over the same period.

It is quite rare for an established market leader to beat the index by such a wide margin. This standout growth has made Fortescue the envy of many other market sectors.

Understanding the ASX Materials Sector

To better understand how (and why) this has occurred, we will examine the ASX materials sector closely. The materials industry is comprised of companies that extract natural resources through mining; this includes minerals like iron-ore, copper, and gold.

Mining companies are generally considered to have unpredictable and unstable profits. Unlike retail/financial stocks, the profit generated by mining companies will fluctuate on a regular basis due to changes in global commodity prices.

Figure 2: Fortescue (ASX: FMG) multi-year stock price timeline tracking market [credit – stocklight]

As Fortescue’s mining operation has a relatively fixed cost to extract and ship iron ore, Fortescue will generate approximately the same profit for every dollar that it sells iron ore for – regardless of whether iron ore is selling for $80 or $180 per tonne.

Because of this fixed cost structure, with the rise in global commodity prices, the majority of every dollar of additional revenue generated by Fortescue as a result of rising global commodity prices flows directly to Fortescue in the form of profit. This is known as operating leverage and is, in fact, what caused the recent increase in Fortescue’s share price.

HY26 Results

The stellar run of the Fortescue share price was heavily supported by its financial reporting. The company’s half-year results for 2026 (HY26) showed immense strength.

During this period, Fortescue’s realised iron ore price improved by 7% to reach US$90.87 per tonne. At the same time, the volume of ore sold increased by 4% to 100.2 million tonnes.

These dual increases created a powerful compounding effect across the company’s entire balance sheet:

- Total Revenue: Climbed by 10% to hit US$8.4 billion.

- Underlying EBITDA: Surged by 23% to US$4.5 billion.

- Net Profit: Increased by 23% to US$1.9 billion.

- Operating Cash Flow: Jumped by 32% to US$3.2 billion.

With cash flowing into the business at this rate, investor confidence soared. Higher earnings inevitably lead to higher share prices in the mining game.

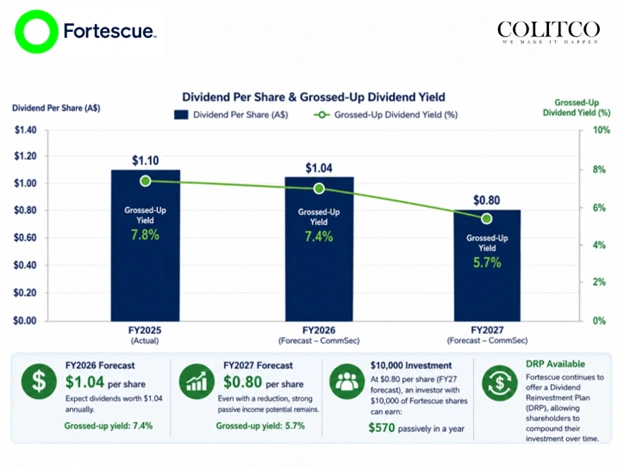

Figure 3: Fortescue dividend per share trends [Colitco]

According to broker UBS:

“Iron ore: we expect prices to remain ~$100/t over the next six months with demand stable and incremental supply growth modest (Simandou is 2H weighted); medium term, we expect the market to move into surplus and prices to trend back to around the 90th percentile, which we estimate at ~$90/t in 2027”.

Global Factors

Australian mining companies do not operate in a vacuum. Their success depends heavily on international trade and global demand.

China remains the primary buyer of Australian iron ore. The Asian superpower requires enormous amounts of steel to power its infrastructure and real estate sectors.

Despite past worries of an economic decline, Chinese demand remained strong throughout the year. This steady appetite kept iron ore trading at highly profitable levels.

Investor sentiment was also boosted by a recovery in market confidence. This followed the initial shock of US tariffs placed on China during the first half of 2025.

By the beginning of 2026, iron ore prices had risen to approximately $109 per tonne. This extended pricing strength provided the perfect environment for Fortescue to thrive.

Passive Income: The Dividend Bonus

While a 40% share price gain is excellent, ASX resource stocks are also famous for dividends. Fortescue has been one of the biggest dividend payers in Australia.

The huge cash flows generated from iron ore sales allow management to return billions to mums and dads. This passive income acts as an extra reward for shareholders.

| Note: Even when analysts predict minor drops in the future stock price, the company’s fully-franked dividends often help soften the blow for long-term holders. |

For instance, forecasts suggest a healthy dividend payout will continue through the financial year. This mix of growth and income is why the stock remains incredibly popular.

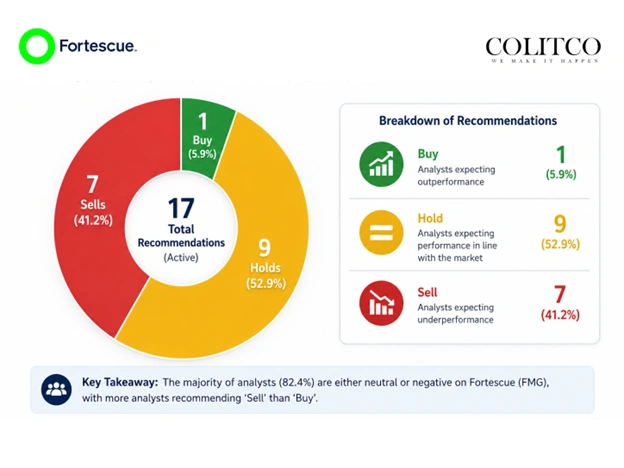

Figure 4: Out of 17 active professional recommendations tracked by CommSec, surprisingly, only a single analyst rates the company a ‘Buy’, compared to nine ‘Holds’ and seven ‘Sells’. [Colitco]

What Does the Future Hold for this Mining Company?

The sustainability of that momentum is probably going to be one of the biggest issues to investors. Over the next year, will we get similar results as the previous 12 months?

As an expert looking at the ASX materials sector, the future remains tied to commodity trends. If iron ore prices retreat, the stock could follow.

Fortescue is also strateging of expanding copper projects. Since copper is critical for the global transition to green energy, it could provide a cushion against declines in iron ore.

However, professional analysts are currently flashing warning signs regarding the current valuation. The consensus view suggests the stock might have run too hard.

Analyst Sentiment

According to recent market data from CMC Invest, the average analyst price target sits at $19.37. This is noticeably lower than the current trading price.

This price target implies that the stock could face a double-digit decline over the coming year. Out of multiple professional ratings, very few investment experts currently rate the stock as a BUY.

Most analysts have placed a HOLD or SELL rating on the company. They believe the easy money has already been made in this specific cycle.

While the past 12 months were spectacular, resource investing requires strict discipline. Buying at the absolute top of a commodity cycle can expose your capital to unnecessary risk.

FAQ

Q: Is my money safe if Chinese demand falls?

A: Being China’s biggest customer, Fortescue will face impacts on its bottom line whenever there is a sudden drop in demand for its steel manufacturing.

Q: Why do analysts ‘sell’ despite the stock price jumping by 40%?

A: Since market analysts focus on future trends, they expect iron ore prices to fall and make the share price drop by more than 10% over the course of the year.

Q: Will passive dividend income be reduced next year?

A: Analysts expect the dividends to be slashed to 80 cents per share compared to the previous figure of $1.04.

Q: Will this be an investment or a short-term trade?

A: This is definitely a trade since its profits will depend exclusively on iron ore prices, which are unpredictable.

Conclusion

The Fortescue stock surge 12-month return analysis shows just how lucrative the mining sector can be. Turning $10,000 into $14,000 in a year is an excellent return for any blue-chip investment.

This expansion was fueled by strong financial results, high iron ore prices, and a rebound in global market confidence. It emphasises the importance of operational strength in the mining industry.

However, care is advised moving forward because commodity markets will certainly fluctuate. For the time being, early investors may celebrate a very successful year in the Australian market.

Disclaimer

This article is meant only for informational purposes. If you are an investor who is watching Mineral Resources Limited closely, all the data published in the content is sourced from ASX announcements and external sources. Kindly verify all information related to the share price and market data. Any investment should be made at the investor’s own risk. Colitco does not hold any position in the above-mentioned Company.

————————-

Sources:

https://www.fool.com.au/2026/05/26/10000-invested-in-fortescue-shares-12-months-ago-is-now-worth/

https://hellostake.com/au/invest/aus/stocks/fmg

https://stocklight.com/stocks/au/asx-fmg/fortescue?media_id=316977

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.