Borrowers in Australia and the United States face different home loan markets in 2026. Australian mortgage rates remain high after continued policy tightening. In the United States, long-term fixed rates hold near 6% but show mild easing. This report compares headline rates, product structures and regulatory settings to explain how each market prices housing credit.

Interest Rate Benchmarks in Australia and the United States

Australia’s benchmark rate rose to 3.85% on 3 February 2026 after a decision by the Reserve Bank of Australia. The central bank said inflation pressures and resilient household demand justified the move. Governor Michele Bullock stated the board would continue to assess incoming data before making further adjustments.

The Reserve Bank of Australia raised the cash rate to 3.85 per cent in February 2026 amid inflation concerns. [ABC]

In the United States, the Federal Reserve kept the federal funds target at 3.50%–3.75% in January 2026. The Federal Open Market Committee noted slower inflation but warned of uncertainty in labour and energy markets. Chair Jerome Powell said policy would remain restrictive until inflation aligned with the target.

Average Mortgage Rates and Recent Market Trends

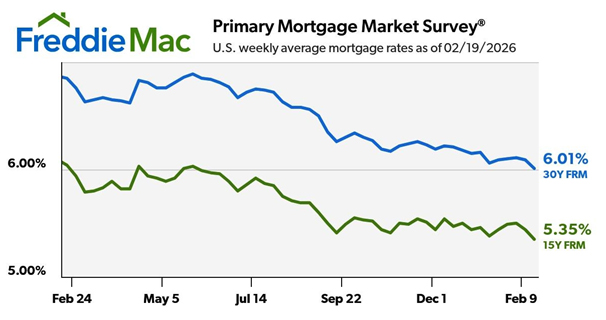

Survey data from Freddie Mac showed the average US 30-year fixed mortgage rate reached 5.98% on 26 February 2026. The figure marked a small decline from earlier in the month. Analysts linked the movement to lower Treasury yields and softer inflation data.

US 30-year fixed mortgage rates eased slightly in late February 2026 after softer inflation data. [Manila Times]

In Australia, average new-loan rates for owner-occupiers stood near the mid-five per cent range in late 2025. Major lenders listed fixed offers above 6% for multi-year terms by early 2026. Market pricing reflected higher wholesale funding costs and expectations that the cash rate would stay restrictive for longer.

Loan Product Structure and Fixed-Term Availability

The United States market relies heavily on long-term fixed mortgages. The 30-year fixed loan remains the standard product for owner-occupiers. Lenders hedge interest rate risk through capital markets and government-backed securitisation programs. Borrowers gain predictable repayments for three decades.

Australian banks operate differently. True 30-year fixed mortgages do not form part of mainstream offerings. Borrowers usually select fixed periods of one to five years, with some loans extending to ten. After the fixed term ends, the loan reverts to a variable rate unless refinanced. This design exposes households to future rate changes and complicates cross-country comparisons.

Central Bank Policy and Mortgage Pricing Dynamics

The February rate rise by the RBA aimed to curb demand and ease price pressures. The central bank said wage growth and housing activity added to inflation risks. Higher policy rates increased bank funding costs and flowed through to retail mortgage pricing.

In contrast, the Federal Reserve paused after earlier reductions in 2025. Officials highlighted slower price growth and weaker business investment. US mortgage lenders link pricing to long-term bond yields rather than short-term rates alone. A decline in those yields in February helped keep 30-year fixed rates near 6%.

Regulation and Lending Standards in Both Markets

The Australian Prudential Regulation Authority introduced a debt-to-income limit from February 2026. The rule caps high-DTI loans at 20% of new mortgage lending. APRA said the measure would reduce systemic risk and moderate speculative borrowing.

APRA introduced a debt-to-income lending cap to reduce systemic risk in Australia’s housing market. [The Adviser]

US lenders operate under different rules. Credit scores, income documentation and loan-to-value ratios determine access to credit. National policy does not impose a fixed quota on high-DTI loans. Instead, private mortgage insurance and federal guarantee programs manage risk. These approaches shape how lenders price loans for higher-risk borrowers.

Comparison of Major Bank Offers in 2026

Commonwealth Bank of Australia listed fixed mortgage rates in the mid-six per cent range for packaged home loans in February 2026. Comparison rates appeared higher after fees. The bank stated pricing reflected wholesale funding costs and regulatory capital requirements.

Westpac published similar five-year fixed rates for principal-and-interest loans. The bank adjusted rates by loan size and borrower profile. Both lenders highlighted that variable products could change quickly if the RBA shifted policy.

In the United States, Wells Fargo quoted an indicative 30-year fixed rate near 6% in late February 2026. The bank noted that advertised rates included typical points and fees, which lifted the annual percentage rate. Other major US lenders posted comparable figures for borrowers with strong credit profiles.

Also Read: How to Choose Shares to Buy in Australia | ASX Guide | Colitco

Implications for Borrowers in 2026

Borrowers seeking payment stability find more certainty in the US market. A 30-year fixed rate locks repayments for the life of the loan. However, borrowers must account for fees, insurance premiums and refinancing penalties when comparing total costs.

Australian borrowers face shorter fixed periods and greater exposure to future rate movements. Regulatory limits on high-DTI lending may also restrict borrowing capacity for some households. Banks price risk more carefully under the new rules, which may affect rates for higher-leverage applicants.

Australian and US home loan markets operate under different structures and policy settings in 2026. Australia shows slightly lower average headline rates for new loans, yet fixed terms remain short and subject to repricing. The United States offers long-term certainty at around 6% but includes higher ancillary costs for some borrowers. Official statements from the RBA, the Federal Reserve and APRA confirm that monetary and regulatory policy continue to shape mortgage pricing in both economies.

FAQs

1) What are current average home loan rates in Australia and the US?

Ans. Australia’s new home loans sit in the mid-5% range, while US 30-year fixed mortgages average about 5.98%.

2) Do Australian banks offer 30-year fixed mortgages like US lenders?

Ans. No. Australia mainly offers fixed terms of one to five years, sometimes up to ten.

3) How do advertised rates differ from effective cost (APR)?

Ans. Advertised rates exclude fees and insurance. APR or comparison rates show the true loan cost.

4) How do central bank decisions affect mortgage pricing?

Ans. Policy rate changes affect bank funding costs and influence variable and fixed loan rates.

5) What is the debt-to-income (DTI) cap in Australia?

Ans. High-DTI loans can make up only 20% of new mortgages from February 2026.

6) Can borrowers refinance to secure lower rates?

Ans. Yes, but they must consider break fees and new loan costs.

7) Are interest-only loans restricted?

Ans. Yes. Both countries apply tighter rules and stricter assessments.

8) How much deposit avoids mortgage insurance?

Ans. A deposit of 20% usually avoids mortgage insurance in both countries.

9) Is mortgage interest tax-deductible?

Ans. Not in Australia for owner-occupiers. Many US borrowers can deduct it.

10) How should borrowers compare fixed and variable loans in 2026?

Ans. They should assess repricing risk, break costs and future rate movements.

11) Where can borrowers find official rate information?

Ans. From central banks, regulators and major bank rate pages.