In financial institutions, we often hear about different frauds and scams. However, something significant happened in Australian banking this week. Commonwealth Bank, the country’s largest lender, reported itself to police and the corporate regulator after uncovering roughly A$1 billion worth of suspected fraudulent home loans. That is not a typo. One billion dollars in loans that may never have been legitimate in the first place.

But CBA did not stand alone in that uncomfortable spotlight. Westpac and ANZ quickly joined NAB and CBA in flagging suspected bogus borrowing through their own channels. Suddenly, the loan fraud investigation gripping Australia ceased to look like one bank’s problem. The Australia big four banks now share both the scrutiny and the reputational fallout, and that changes the nature of the challenge entirely.

Figure 1: Australia’s big four banks face scrutiny after Commonwealth Bank uncovered A$1 billion in suspected fraudulent home loans, prompting industry-wide investigations and reputational damage.

This Is Not History Repeating: It Is History Evolving

Australians who remember the 2018 Royal Commission into Banking Misconduct will feel a familiar unease. Back then, NAB bankers in greater western Sydney accepted bribes and approved loans based on false documentation to hit lending targets and collect personal bonuses. The Commission found that up to 15 per cent of all NAB home loans approved at certain branches did not meet standard criteria for valuation, serviceability, or document verification.

That was ugly. But today’s version is harder to defeat. The new wave of fraud does not rely on corrupt insiders accepting cash. Instead, criminals use stolen personal data pieced together from large-scale data breaches, then feed that data into AI tools that generate convincing fake payslips, tax returns, and identity documents.

According to cybersecurity expert Luke Irwin of Aegis Cybersecurity, criminals build entire fake identities from stolen data and then use AI tools to produce convincing supporting documents. The forgeries no longer look like forgeries.

The banking sector spent years tightening internal controls after the Royal Commission. Those controls largely targeted human misconduct. They were not built to stop an algorithm.

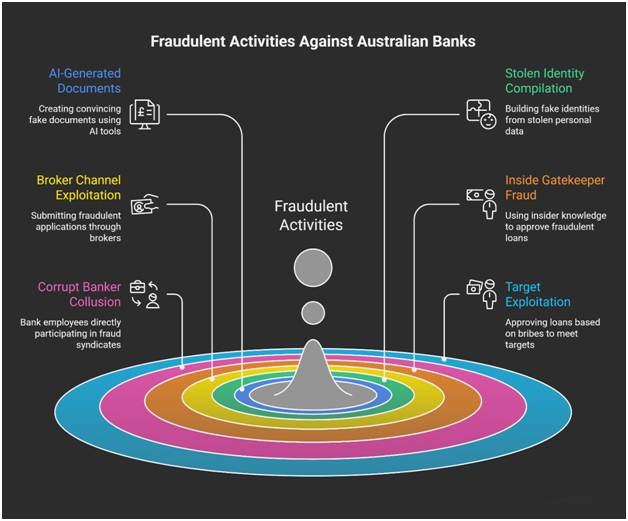

Figure 2: Ways loan fraud activities are being committed in the banks

The Broker Channel: Growth Engine or Weak Link?

Here is a structural tension that deserves more attention than it typically gets. UBS estimates that mortgage brokers now originate close to 80 per cent of new Australian home loans. Banks have leaned into this model aggressively, it allows them to scale loan books without expanding their own salesforces.

But that same broker channel is exactly where the fraud enters. CBA’s own spokesman described the problem as coming through “mortgage broking and referral channels.” The bank invested A$900 million last financial year to strengthen its protections, and it still wound up with a suspected A$1 billion fraud problem sitting inside its loan book.

This raises an uncomfortable question for every CEO at the Australia big four banks: if brokers originate most of your loans, and you cannot verify those loans fast enough to remain competitive, then speed and security fundamentally conflict. Every time competitive pressure shortens verification timelines, the door opens wider for sophisticated fraud syndicates.

The Syndicate Problem: Organised Crime Goes Institutional

The Clayton Utz white-collar crime review of 2026 paints a disturbing picture of just how organised this fraud has become.

In late 2025, a former senior NAB business banking manager faced 19 charges for allegedly acting as a “gatekeeper” inside a syndicate that used stolen identities to obtain over A$200 million in fraudulent loans across multiple lenders. Police estimate the total fraud from that syndicate alone may reach A$250 million.

A separate case involved a former CBA and NAB banker charged with 89 fraud-related offences for allegedly participating in a A$105 million fake loan syndicate. These are not opportunistic criminals. These are organised operations with inside knowledge of how banks process loans, where the verification gaps lie, and how to exploit them at scale.

The bank fraud investigation now underway across Australia must grapple with the fact that syndicates study institutional behaviour. When banks tighten one channel, experienced syndicates move to another. When one verification step becomes robust, AI helps create documents that pass it.

Also Read: Will Rising Interest Rates Pressure ASX Bank Profits in 2026?

What Regulators Are Watching: And What They Will Demand Next

ASIC and APRA have not been idle. In 2025, ASIC settled four claims against a major banking group for A$240 million in penalties. AUSTRAC’s anti-money laundering reforms take effect in phases through 2026.

New Financial Accountability Regime obligations increase the personal risk for senior executives who preside over risk governance failures.

The message from regulators is clear: ignorance is no longer a defence, and the era of institutional settlements without individual accountability may be ending. The A-O Shearman white-collar review notes that while no individual has yet faced prosecution under the Financial Accountability Regime, personal enforcement risk is rising fast given parliamentary and public pressure.

For the Australia big four banks, this creates a dual compliance burden. They must defend against external criminal syndicates while simultaneously demonstrating to regulators that their governance structures are genuinely robust, not just paper-compliant.

Technology Is Both the Problem and the Answer

The irony of the current crisis is that AI creates the fraud problem, and AI must help solve it. In November 2024, ANZ, CBA, NAB, and Westpac joined a pilot of BioCatch Trust, a world-first inter-bank behavioural biometric intelligence network. The system analyses thousands of digital interactions in real time, flagging risks associated with receiving accounts before payments leave the sender.

Figure 3: Logo of BioCatch [BioCatch]

Banks have also deployed hundreds of machine learning algorithms to detect mule accounts and suspicious patterns. ASIC has previously found that the big four banks detect only around 13 per cent of scams, and refund just 2-5 per cent of losses. Those numbers need to move dramatically; and fast.

What technology cannot yet fully solve is the document verification problem at loan origination. When a fraudulent application arrives through a broker channel, accompanied by AI-generated documents that pass optical and structural checks, the fraud often enters the system before any behavioural signal exists to detect it.

What Needs to Change: Three Hard Realities

First, the broker model needs structural reform. Banks cannot continue to outsource 80 per cent of loan origination to brokers while treating verification as a broker responsibility rather than a bank responsibility. The Royal Commission made that point in 2018 about expense verification. The same logic applies to identity and income verification in 2026. Banks must own the verification process end to end, not merely rely on what brokers submit.

Second, Australia needs a serious regulatory conversation about AI-generated document fraud. UNSW AI researcher Toby Walsh argued this week that the scale of the CBA fraud demonstrates the federal government can no longer claim Australia does not need new AI regulation. The tools that generate fake payslips and identity documents face no meaningful legal controls. That gap needs closing.

Third, the industry’s existing intelligence-sharing infrastructure must deepen. BioCatch Trust is a promising start for payment fraud. But the equivalent does not yet exist for loan application fraud, a real-time, cross-institution system that flags suspected fraudulent applications before loans settle, not after billions of dollars have already moved.

Figure 4: Three steps to Address Loan Application Fraud in Australia

The Deeper Issue: Trust in the System

Australia’s big four banks hold a position of extraordinary structural importance. They originate the majority of Australian home loans, they process the overwhelming majority of domestic payments, and they sit at the centre of the nation’s financial architecture. When CBA’s share price slips 1.5 per cent on news of a fraud probe, even while the broader market closes near record highs, it signals that investors understand the stakes.

But the deeper risk is not to share prices. It is to the implicit trust Australians place in the loan verification system every time they compete for a home in one of the world’s most expensive property markets. If criminals can obtain A$1 billion in fraudulent home loans, they drive up property prices, distort credit risk across the financial system, and ultimately expose ordinary borrowers to the consequences of a market inflated by fake demand.

The bank fraud investigation now unfolding across CBA, NAB, Westpac, and ANZ is not simply a banking problem. It is a systemic problem that demands systemic answers. The question is whether Australia’s regulators, legislators, and banking executives treat it as such — or wait for the next Royal Commission to tell them what they already know.

Sources

- Australian Financial Review: https://www.afr.com/companies/financial-services/big-four-banks-find-themselves-embroiled-in-loan-fraud-probe-20260226-p5o5r8

- The Conversation: https://theconversation.com/why-commonwealth-banks-1billion-suspected-loan-fraud-should-change-how-we-bank-and-do-business-277083

- TS2 Space / Investing.com: https://ts2.tech/en/cbas-1-billion-mortgage-fraud-alarm-big-banks-face-new-ai-document-threat/

- Clayton Utz: https://www.claytonutz.com/insights/2026/february/australias-top-business-crime-cases-insights-into-white-collar-crime-trends

- A-O Shearman: https://www.aoshearman.com/en/insights/cross-border-white-collar-crime-and-investigations-review-2026/australian-regulators-intensify-enforcement-of-bribery-money-laundering-and-ai-driven-fraud

- BioCatch: https://www.biocatch.com/press-release/biocatch-partners-australian-banks-fraud-scams-intelligence-sharing-network

- Information Age / ACS: https://ia.acs.org.au/article/2024/big-four-banks-test-new-ai-based-fraud-tech.html

- iTnews: https://www.itnews.com.au/news/australias-big-4-banks-exit-thousands-of-suspected-mule-accounts-614079

- Berrills Watson: https://www.berrillwatson.com.au/supertalk-blog/2023/may/financial-scams/

- ASIC: https://download.asic.gov.au/media/mbhoz0pc/rep761-published-20-april-2023.pdf