ASX 200 Starts Steady As Global Volatility Builds

The ASX 200 futures opened flat on Monday morning despite renewed global market jitters. European markets closed broadly lower overnight as investors weighed escalating trade tensions ahead of Donald Trump’s reciprocal tariff deadline. The US markets remained shut due to Independence Day.

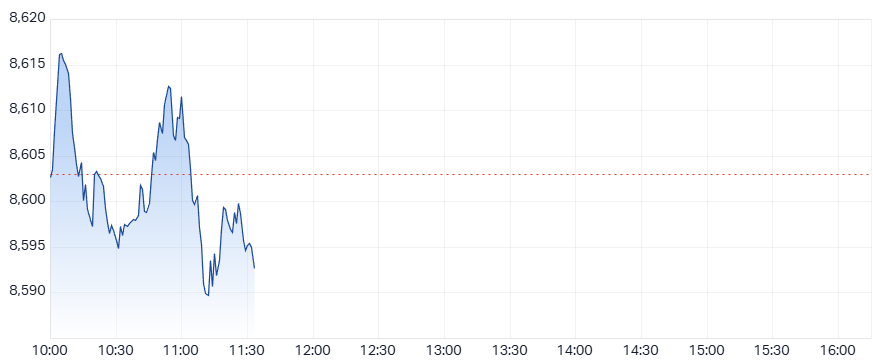

ASX 200 Chart as of 11:33 AM AEST

U.S. Policy Shifts And Tariff Deadline Dominate Sentiment

Investor sentiment shifted after the US House passed a US$3.4 trillion fiscal package. The bill includes widespread tax cuts, spending reductions, and reversals of Joe Biden’s clean energy initiatives. Trump’s reciprocal tariffs, due to commence on 1 August, added further pressure. Trump stated he signed letters to 12 countries, detailing tariff rates on exports to the US. These “take it or leave it” offers are expected to be dispatched this week, according to Reuters.

Major US trading partners rushed to secure trade deals or request extensions over the weekend, Bloomberg reported.

Gold Producers Under Investor Focus Following Quarterly Updates

Gold miners released their quarterly updates amid a strong FY25 backdrop. AUD gold prices rose around 45% over the year. Yet, gold stocks only outperformed by 10%, according to RBC Capital Markets analyst Alex Barkley. FY25 saw decent operational delivery with minimal surprises. Investors now focus on FY26 guidance.

Top FY25 Performers And Preferred Names

Strong performers in FY25 included SX2, RRL, EVN, DEG, and GOR, largely due to lower hedge exposure. Barkley highlighted Westgold Resources and Bellevue Gold as preferred mid-tier miners for FY26 due to earnings leverage and low-risk growth.

RBC upgraded Vault Minerals to Outperform as hedge roll-offs are expected to drive EBITDA growth. SX2 was downgraded to Sector Perform on valuation concerns. Regis Resources is favoured over large caps like Northern Star and Evolution due to better value and momentum.

RBC’s FY26 Gold Production And Cost Outlook

Northern Star’s FY26 gold sales guidance of 1,700-1,850koz falls short of its previous 2.0Moz target. AISC is forecast between A$2,300 and A$2,700 per ounce, above Citi’s forecast of A$2,181/oz. Citi projects FY26 production at 1,793koz, flagging ongoing cost pressures from delayed Golden Pike North access and higher maintenance across Yandal.

Evolution Mining is expected to meet FY25 guidance, with flat FY26 production outlook. Despite a 35% reserve grade cut at Red Lake, minimal risks to guidance are forecast. However, recent strong stock performance restricts its near-term value.

Ramelius And Regis Deliver Mixed Guidance And Performance

Ramelius Resources beat FY25 guidance with gold production at 301,664 ounces and fourth-quarter output at 73,454 ounces. Free cash flow surged to $694.9 million, lifting cash reserves to $809.7 million. No FY26 guidance was issued. Managing Director Mark Zeptner said, “We plan to embrace their exploration DNA which led to the discovery of the highest-grade undeveloped gold project in Australia, importantly right in our backyard.”

Regis Resources expects FY26 gold production of 365koz, compared to consensus of 375koz. AISC is projected to rise 4%, with A$65 million in growth capex. Despite a strong FY25, Regis remains undervalued, with a 3.2x EV/EBITDA multiple and 21% free cash flow yield.

Mixed Results For Other Gold Producers

Alkane Resources reported FY25 gold production of 70,120 ounces, meeting guidance. Managing Director Nic Earner said, “Alkane’s operation at Tomingley, combined with our merger with Mandalay Resources, place us firmly into the mid-tier gold companies on the ASX.”

Bellevue Gold missed its downgraded Q4 guidance, producing 38.9koz versus guidance of 40-40.5koz. FY25 sales were 130,164 ounces, slightly below Goldman Sachs’ estimate. However, strong free cash flow of A$48 million offset the miss.

Vault Minerals slightly missed FY25 sales guidance. FY26 estimates forecast lower production and higher costs, but an 85% EBITDA rise by FY27 is expected.

Westgold Resources’ FY25 guidance may be missed again, but this is seen as priced in. FY26 value remains strong, with consistent unhedged production growth driving a 2.0x EV/EBITDA multiple.

South32 Exits Cerro Matoso In Strategic Move

South32 entered a binding agreement to sell its Cerro Matoso nickel project to CoreX for up to US$100 million. The deal includes US$80 million tied to production and pricing, and US$20 million based on permitting milestones. The asset will be reported as a discontinued operation, with a US$130 million write-down for FY25. CEO Graham Kerr said, “The Transaction is consistent with our strategy and will further streamline our portfolio toward higher margin businesses in minerals and metals critical to the world’s energy transition.”

Cobram Estate Olives Posts Strong Production And Acquisition Update

Cobram Estate Olives guided FY25 adjusted EBITDA at $115 million, above the $114.3 million consensus. Olive oil production reached 14.2 million litres, up from 10.1 million litres last year. Over 2.7 million litres were sold between April and June. The company declared a fully franked dividend of 4.5 cents per share. It also acquired Leda Ag, a farming machinery business, for an initial $3 million, with up to $2 million more due over four years.

Nanosonics Unveils New Devices To Extend Innovation Reach

Nanosonics launched the trophon3 ultrasound disinfection device with over 40% faster cycles, enhanced digital features, and broader traceability. It also introduced a software upgrade for trophon2 users. Both will roll out across Europe, the UK, Australia, and New Zealand, while US regulatory review is pending. RBC’s Craig Wong-Pan said, “We estimate only ~35% of NAN’s US installed base had upgraded to a trophon2 at Dec 24 and therefore we believe there is a reasonable runway for further upgrade sales.”

Northern Star Falls On Higher FY26 Cost Guidance

Northern Star opened 2.94% lower at $17.85 and dropped as much as 8.05% to $16.91 during morning trade. It currently trades 6.53% lower at $17.19. The company guided FY26 gold sales of 1,700-1,850koz and AISC of A$2,300–2,700/oz. Investors reacted negatively to the significantly higher costs.

Soul Patts Secures Full Equity Funding For Merger

Soul Patts raised an additional $220 million at no discount to its last closing price of $42.61. The fully funded capital raise now totals $1.4 billion from 34 million shares. “This represents a key milestone in the merger process, providing shareholders with certainty that all equity funding has been secured ahead of the scheme votes,” the company said.

Citi Downgrades Afg And Pepper Money After Strong Rallies

Australian Finance Group and Pepper Money surged 40–45% this year, buoyed by expectations of a 3.1% terminal cash rate. However, Citi sees recent gains as driven by P/E re-ratings rather than earnings upgrades. Earnings growth is forecast to emerge slowly as lower rates improve sentiment. Citi downgraded both from Buy to Neutral. AFG’s target rose to $2.10 from $1.85. Pepper Money’s target rose to $1.75 from $1.45.