Westpac Group (ASX: WBC), one of Australia’s Big Four banks, has released its financial results for the half-year ended 31 March 2025. Despite global macroeconomic challenges, the bank has posted a solid performance driven by strategic growth in key lending areas, resilient credit quality, and a renewed focus on regional accessibility. Net profit after tax came in at $3.3 billion, while the interim dividend remained steady, signalling confidence in Westpac’s long-term trajectory.

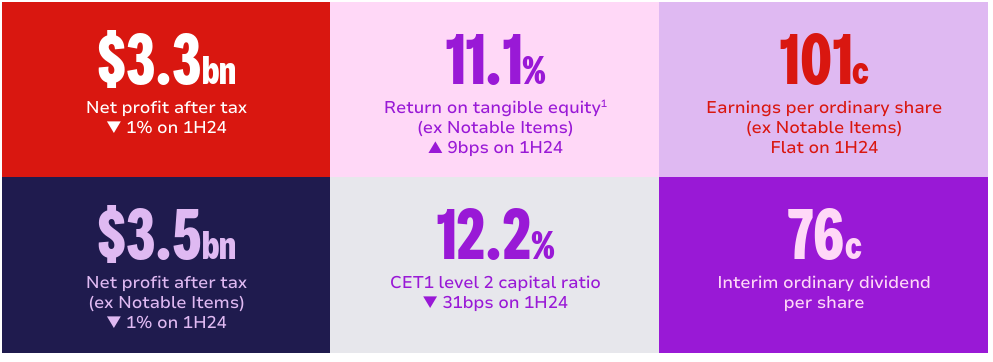

Figure 1: Financial Highlights of Westpac Group’s 2025 Half-Year Results

Solid Financial Results Despite Market Headwinds

Westpac’s financial performance in the first half of FY25 reflects its disciplined approach to growth and risk. Highlights include:

- Net profit after tax: $3.3 billion (down 1% from 1H24)

- Earnings per share: 101 cents (unchanged)

- Return on tangible equity (excl. notable items): 11.1%, up 9 basis points

- Business lending: up 14% year-on-year

- Institutional lending: increased by 15%

- Australian housing loans: grew by 5%

- Household deposits: rose by 9%

- Common Equity Tier 1 (CET1) capital ratio: 12.2% (down 31 basis points)

While the slight dip in net profit reflects broader economic softness and increased operational investment, the growth in core lending and deposits demonstrates strong customer trust and sustained business momentum.

CEO Anthony Miller: “We’re Building for the Long Term”

Westpac CEO Anthony Miller praised the results as proof of the bank’s strategic alignment and people-focused service model.

“This result confirms Westpac’s strong position. We are growing in the areas we’re targeting and supporting customers through uncertain times. Whether it’s helping businesses invest or enabling families to purchase their homes, we’re committed to being there when it matters most,” said Mr. Miller.

The bank’s continued investments in digital platforms, regional service models, and frontline staff aim to create a more accessible and responsive customer experience.

Investing in Regional Australia

A highlight of this half-year report is Westpac’s renewed commitment to regional Australia. The bank has announced the establishment of three new service centres in Moree (NSW), Leongatha (VIC), and Smithton (TAS). These centres will combine in-person banking services with digital technology to improve access and efficiency for customers living outside metropolitan areas.

The move aligns with Westpac’s broader regional strategy and efforts to address concerns about the availability of banking services in remote communities.

Operational Efficiency and Technology Transformation

Operating expenses rose 6% to $5.7 billion in 1H25, primarily due to the ongoing UNITE transformation program, wage growth, and increased investment in third-party technology services.

The UNITE program is a key strategic pillar for Westpac, aimed at simplifying systems, improving service delivery, and modernising operations across the group. Additional investment has also been directed towards digital platforms like:

- Westpac One – a new digital banking experience

- BizEdge – a platform focused on transaction and business lending

Despite short-term expense growth, these initiatives are expected to deliver improved efficiency and cost-to-income ratios over time.

Strong Balance Sheet and Capital Position

Westpac continues to maintain a strong capital base. The CET1 ratio at 12.2% remains well above the Australian Prudential Regulation Authority (APRA) minimum requirements. This robust capital position provides flexibility for future investments, regulatory compliance, and consistent shareholder returns.

The board has declared an interim fully franked dividend of 76 cents per share, unchanged from the prior half and representing a payout ratio of 75% of earnings (excluding notable items).

Credit Quality Remains Resilient

The first half of FY25 demonstrated strong credit quality despite ongoing cost-of-living pressures for households and global economic volatility. Key indicators include:

- Stressed exposures at 1.36% of total committed exposures (flat from 2H24)

- Credit impairment charge of 6 basis points, down from 9 basis points in 1H24

- Impairment provisions of $5.07 billion, marginally lower than the previous half

This stability reflects careful credit management and the overall resilience of Australian consumers and businesses.

Sustainability and Financial Inclusion

Westpac continues to advocate for financial inclusion and sustainable banking. The bank’s support for housing affordability, improved cash access, and environmental impact reporting are core to its stakeholder engagement strategy. Westpac has signalled intentions to work more closely with the Australian Government and regulators on:

- Housing market challenges

- Cash access solutions for older Australians and rural communities

- ESG transparency and climate-related financial disclosures

These long-term priorities align with Westpac’s goal of being a responsible, community-focused institution.

Looking Ahead: Opportunities and Challenges

While the outlook for the second half of 2025 remains cautious due to geopolitical tensions and uncertainty in global trade flows, Westpac is well-positioned to manage potential disruptions. The group’s strong balance sheet, capital flexibility, and digital momentum will be key in navigating emerging risks.

CEO Anthony Miller remains optimistic:

“We’ve built a bank that is simpler, stronger, and more responsive to customer needs. We’re confident in our strategy and our people, and we look forward to driving sustainable growth in the years ahead.”

About Westpac Group

Founded in 1817, Westpac is Australia’s oldest bank and one of its largest financial services groups. As of March 2025, Westpac holds a 21% market share in both Australian household deposits and mortgages. The bank serves over 13 million customers across Australia, New Zealand, and global markets.

Investor’s Outlook: Solid Fundamentals with Long-Term Upside Potential

Westpac Banking Corporation (ASX: WBC) continues to offer investors a compelling mix of steady performance and future potential, even amid short-term market fluctuations.

As of the latest trading session, WBC shares are priced at $32.56, down 2.66% for the day. However, broader metrics paint a positive picture. The bank’s market capitalisation stands at $114.50 billion, and its 52-week range of $25.76 to $35.27 highlights a strong recovery and growth trajectory over the past year.

Performance Snapshot

- 1 Week: +1.62%

- 1 Month: +5.07%

- 2025 YTD: +0.74%

- 1 Year: +23.24%

- Outperformance vs Sector (1yr): +1.82%

- Outperformance vs ASX 200 (1yr): +16.14%

These figures reflect investor confidence in Westpac’s operational strategy and long-term direction. The bank’s 1H25 results — particularly its robust lending growth, stable dividend, and regional expansion — are aligned with broader investor interests in defensive, income-generating stocks within a volatile economic environment.

Dividend Stability and Capital Strength

Westpac’s fully franked 76-cent interim dividend reinforces its appeal as a reliable dividend stock. Backed by a CET1 capital ratio of 12.2%, the bank remains well-capitalised to weather regulatory pressures and economic headwinds, while still rewarding shareholders.

Long-Term View

With a 1-year return of +23.24%, WBC has significantly outperformed the broader ASX 200 index by 16.14%. This positions Westpac as a potential long-term hold for investors seeking stable income and strategic growth exposure in the financial sector.

As Westpac continues to invest in digital transformation and regional outreach, analysts and long-term shareholders may view current price dips as an opportunity to accumulate on weakness, especially with the stock still trading below its 52-week high.