Approximately 24 million Americans face a dramatic shift in healthcare affordability starting January 1, 2026. Enhanced Affordable Care Act subsidies expire on December 31, 2025, fundamentally altering marketplace insurance costs. The majority of these enrollees depend entirely on federal tax credits disappearing overnight. Premium payments will increase substantially once these crucial credits vanish from the system.

Health insurance cost spike in 2026

Subsidy Expansion Made Healthcare Accessible

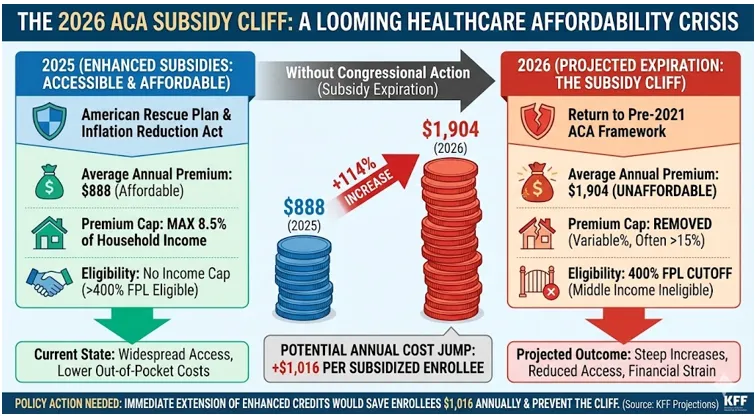

The American Rescue Plan introduced expanded tax credits in 2021 across the nation. These subsidies made health insurance dramatically more affordable for millions of working Americans. The Inflation Reduction Act extended these benefits through 2025, temporarily widening eligibility and increasing assistance amounts. Households earning above 400% of the federal poverty level gained access to credits previously unavailable to them. Premiums became capped at 8.5% of household income for most beneficiaries. No one enrolling during this period faced the previous coverage barriers.

Expiration Will Double Premium Payments

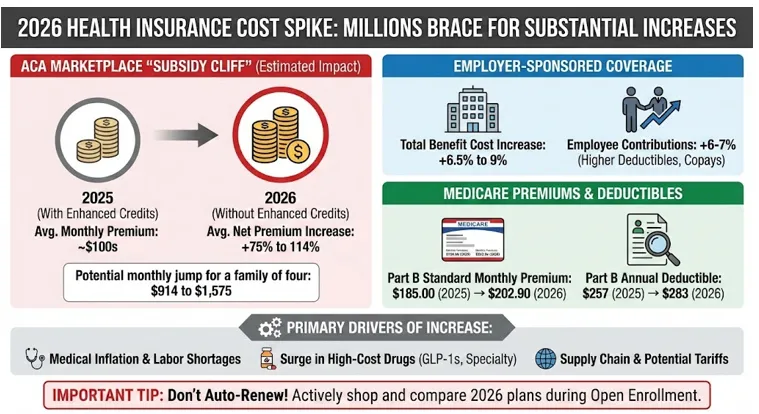

KFF, a nonpartisan health policy research organisation, released startling projections about 2026 affordability. Premium payments will more than double for subsidised enrollees without congressional action. Average annual premiums jump from $888 in 2025 to $1,904 in 2026. This represents a 114% increase in out-of-pocket costs within twelve months. Subsidised enrollees would save $1,016 annually if Congress extends the enhanced credits immediately. Unsubsidised individuals face even steeper increases across the marketplace system.

The 2026 ACA Subsidy Cliff

Risk Pool Deterioration Accelerates Premium Growth

Insurance companies expect significant enrollment declines when subsidies expire completely. Healthier individuals will likely abandon marketplace coverage due to affordability concerns. This dynamic creates a sicker risk pool, prompting insurers to raise rates further. Median premium increases of 15% are being requested for 2026 across major markets nationally. Some insurers cite subsidy expiration as contributing an additional 4% to their rate increase proposals. Healthcare providers anticipate losing $32 billion in reduced revenue once uninsured rates climb sharply.

Congressional Action Remains Stalled

Democrats consistently advocated for clean extensions of enhanced premium tax credits. Proposed legislation would continue subsidy assistance for multiple years without modification. Republican proposals focused on alternative approaches with fewer fiscal commitments. Neither Democrats nor Republicans gathered sufficient votes in the Senate recently. Both options failed to reach the 60-vote threshold required for passage. Republican leadership did not include subsidy extensions in their recent tax legislation approved before year-end. The outcome leaves millions without certainty regarding 2026 healthcare affordability.

Broader Healthcare System Faces Cascading Challenges

The Congressional Budget Office estimates 4.2 million Americans could become uninsured within ten years. This represents the direct impact of subsidy expiration alone. Combined with broader Medicaid cuts and ACA programme reductions, healthcare coverage faces unprecedented contraction. Over $1 trillion in programme spending reductions will compound the subsidy expiration effects significantly. Healthcare institutions serving as community economic anchors anticipate revenue declines and uncompensated care increases. The magnitude of these changes represents the most substantial federal healthcare support rollback in modern history.

Also Read: Beyoncé Hits Billionaire Status After Cowboy Carter Tour Smashes Records

Employer-Sponsored Plans Also Face Premium Increases

Working-age Americans with employer coverage experience separate cost pressures in 2026. Family health insurance premiums reached $27,000 in 2025, up 6% from the previous year. Employers project additional 9% increases for 2026 based on recent benefit surveys. Mercer’s analysis indicates the largest employer premium increases since 2010. Aon forecasts 9.5% increases in employer health expenses for the coming year. Prescription drug costs, particularly weight-loss medications, drove substantial premium growth in 2025. Chronic illness management and increased medical service utilisation continue pushing expenses upward.

Population Segments Face Disproportionate Impact

A 35-year-old couple earning $30,000 annually would see annual premiums increase from zero to $1,500. A 49-year-old couple earning $90,000 with a 19-year-old child experiences annual premium increases to nearly $9,000 from $6,246. Middle-income households above 300% of poverty face the sharpest percentage increases. Lower-income households lose complete premium subsidies when credits expire. Some enrollees will simply exit the marketplace due to unaffordability. KFF’s updated tax credit calculator allows individuals to model their specific 2026 cost scenarios.

Healthcare System Faces Unprecedented Disruption

Medical professionals warn of substantial patient harm from subsidy expiration. The American Medical Association and over 90 physician organisations formally opposed allowing credits to lapse. Healthcare provider networks anticipate treating increased uninsured populations. Emergency departments expect rising volumes from previously insured individuals. Community health centres will experience expanded service demand without corresponding revenue increases. The disruption extends beyond marketplace plans to broader healthcare system capacity.