West Africa now leads global gold exploration. Côte d’Ivoire sits at the absolute centre of this modern gold rush. The nation holds underexplored greenstone belts that excite global investors.

The Côte d’Ivoire gold mining future looks incredibly bright right now. Junior explorers are transforming into major producers across the country. One project stands out among the rest in 2026.

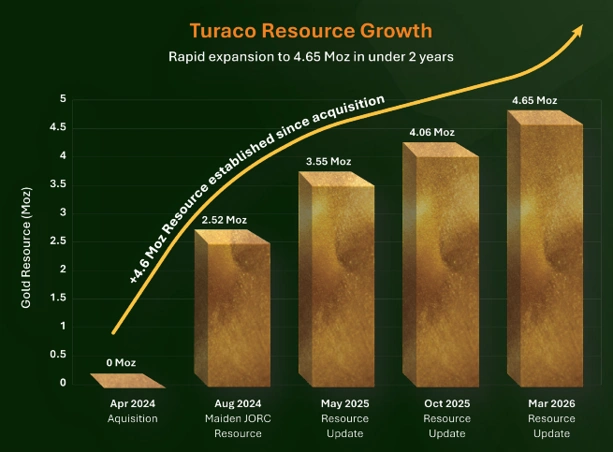

Fig 1: Turaco resource growth [ASX Announcement]

The Afema Project Milestone

Turaco Gold recently released its Pre-Feasibility Study for the Afema project. This study confirms excellent economic potential for the asset. The project will anchor the Côte d’Ivoire mining industry outlook for years.

Turaco holds a dominant land position in the southeast region. The company has established a gold resource in under two years. This progress showcases the true quality of the asset.

The project boasts a maiden open pit JORC Ore Reserve of 1.9 million ounces. This reserve underpins a mine life of more than ten years. The asset positions Turaco as a major upcoming gold producer.

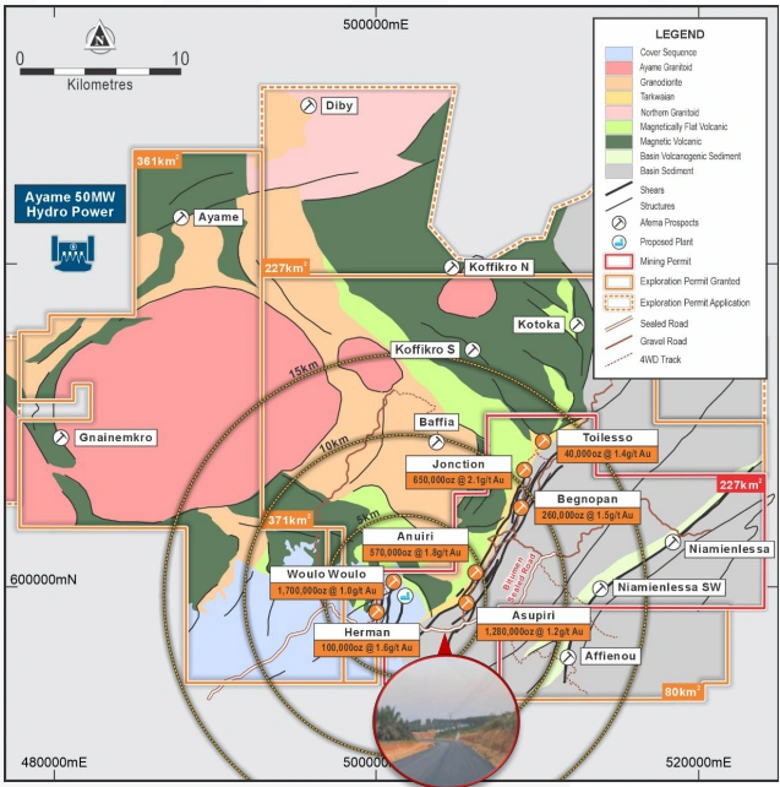

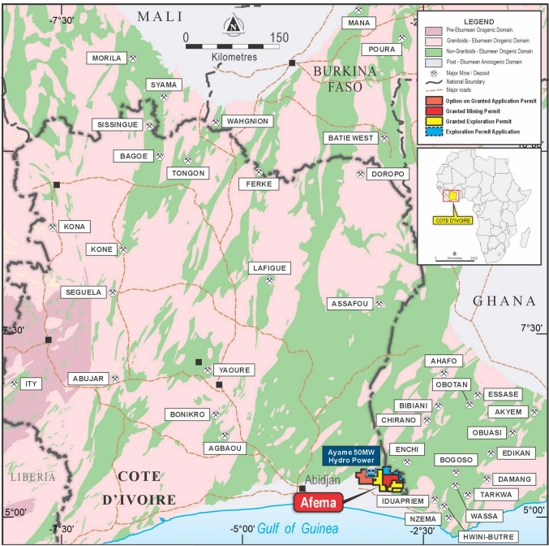

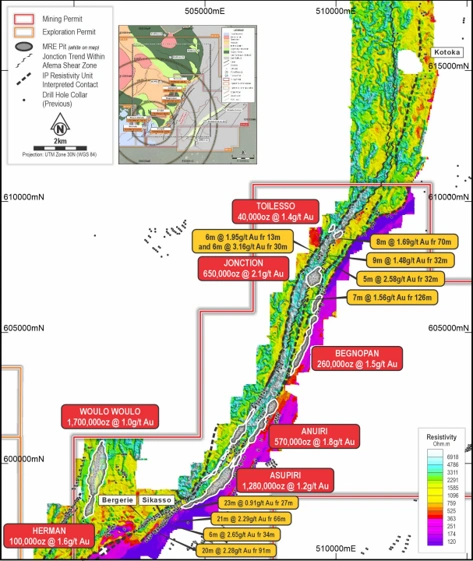

Fig 2: Afema Project map [ASX Announcement]

Star Operations and Production Targets

The operation will deliver over 230,000 ounces of gold in its first year. Production will average 215,000 ounces annually for the initial seven years. Over the entire mine life, the site will produce 196,000 ounces per year.

These numbers place Afema among the premier gold mining projects in Côte d’Ivoire. The global gold industry desperately needs this type of production scale. Turaco will process 6 million tonnes of ore every year.

The total mineral resource estimate currently stands at 4.65 million ounces. This resource grew at a rate of 100,000 ounces every single month. Geologists love this type of resource growth.

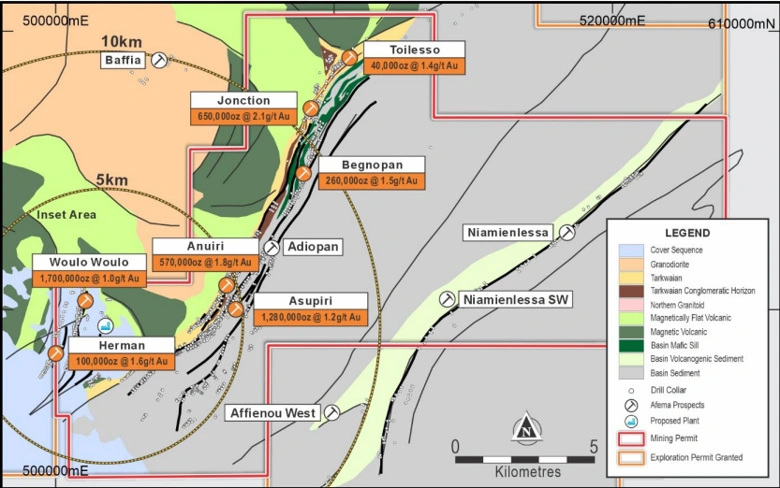

Fig 3: Afema Ore Reserve, Production and Layout [ASX Announcement]

Financial Metrics and Value

The financial metrics from the study look exceptionally strong. At a gold price of US$3,500 per ounce, the project shines. The post-tax net present value hits a staggering US$2.1 billion.

The project delivers an internal rate of return of 79 percent. This rate represents elite financial performance for any mining asset. Capital payback takes a mere 13 months from production start.

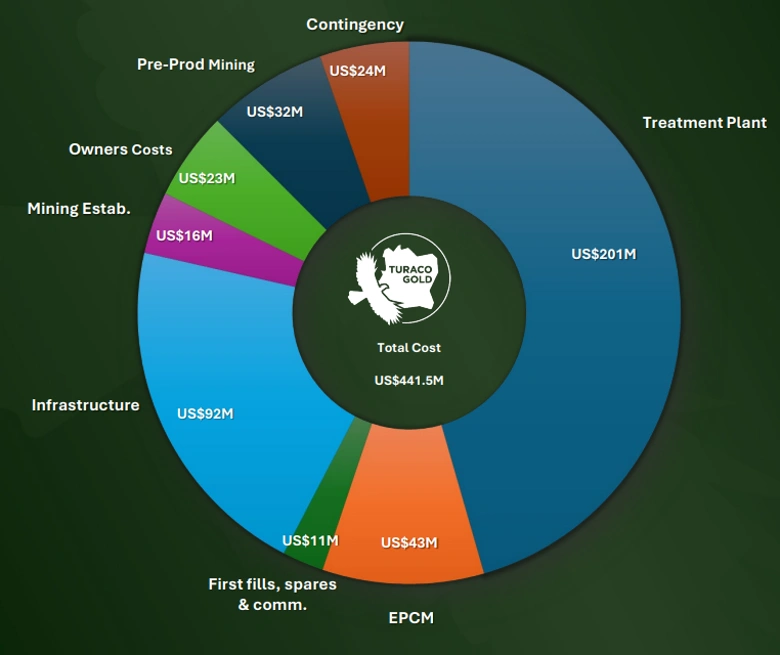

Development capital requires US$410 million, which includes a healthy contingency. Pre-production mining costs add another US$32 million to that initial total. The capital intensity remains very low compared to global peers.

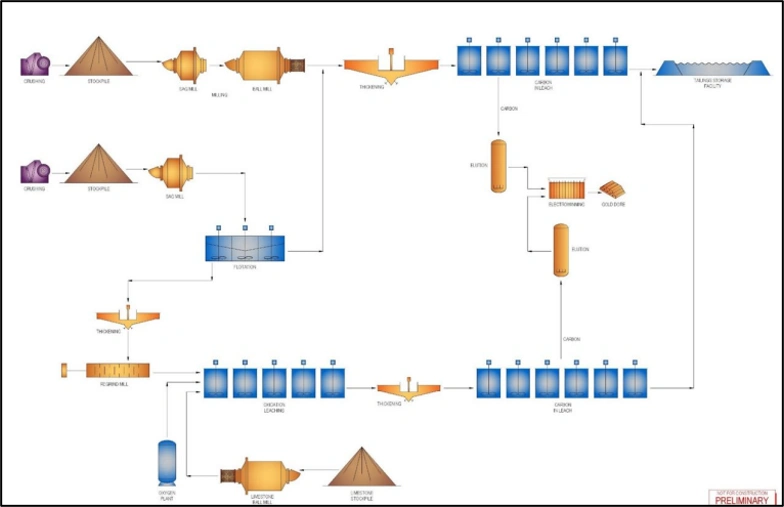

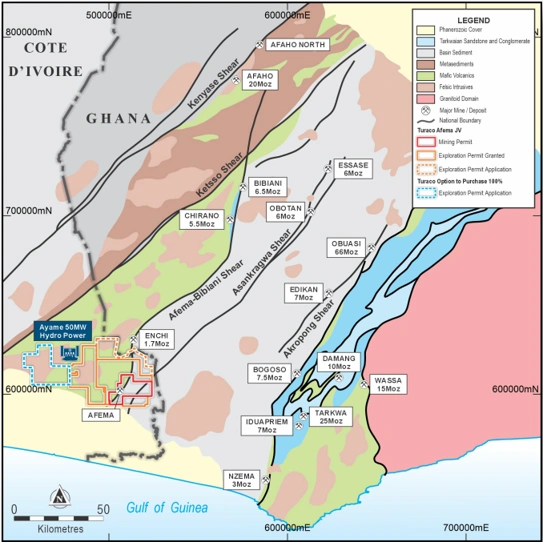

Fig 4: Process Plant | Comprehensive Metallurgical Testwork [ASX Announcement]

Costs and Profit Margins

The operation maintains a Life of Mine strip ratio of 4.8 to 1. This ratio allows for highly efficient open pit mining operations. Contract miners will handle the earthmoving duties to save initial capital.

Cash operating costs sit at a comfortable US$1,268 per ounce. The All-In Sustaining Cost tracks at US$1,508 per ounce over the mine life. These costs guarantee excellent profit margins in the current market.

The high gold price environment ensures cash generation. Year one pre-tax operating cash flow will reach US$442 million. This cash flow provides ultimate financial flexibility for the company.

Fig 5: Location Advantage | Low Capital Intensity Development [ASX Announcement]

Process Plant Infrastructure

The processing plant uses a smart dual-circuit design. The first circuit is a 4 million tonne per annum carbon-in-leil system. This circuit processes the softer oxide and simple fresh ore.

The second circuit is a 2 million tonne per annum flotation system. This section handles the more complex mineralisation through ultra-fine grinding. This configuration yields a gold recovery rate of 87 percent.

Extensive metallurgical testing confirms excellent recoveries across all deposits. The main Woulo Woulo deposit achieves 92 percent recovery in oxide material. This simple metallurgy keeps processing costs highly predictable.

Fig 6: Development Capital Benchmarking [ASX Announcement]

Infrastructure Advantages

The project benefits from world-class infrastructure right on its doorstep. A new sealed highway connects the site directly to the capital city. The major port of Abidjan sits just 120 kilometres away.

This proximity cuts down transport times to a mere two hours. Heavy machinery can reach the site without expensive road upgrades. This geographic advantage significantly reduces initial development costs.

Reliable green grid power sits just 32 kilometres from the project. The nearby Ayame hydro scheme provides cheap, renewable electricity. This access eliminates the need for expensive diesel generation on site.

Fig 7: Afema Gold Project [ASX Announcement]

Minimal Resettlement and Social Licence

Turaco has designed the mine with great environmental care. The Environmental and Social Impact Assessment is nearing final completion. The project requires absolutely zero village relocations.

Small and scattered settlements keep the overall footprint very clean. This layout minimises social capital expenditure and project delays. The local communities strongly support the upcoming development.

This strong social licence lowers the execution risk for investors. Smooth permitting allows the company to hit its development milestones quickly. Turaco is setting a new standard for sustainable mining.

Fig 8: Afema Project Location [ASX Announcement]

Regional Geology and Scale

The Afema permit area covers 1,600 square kilometres. It sits on the underexplored extension of the famous Sefwi gold belt. This belt hosts several world-class multi-million-ounce deposits nearby.

The project area features a convergence of two prolific gold structures. Over 35 kilometres of strike length remains prospective. All five main deposits remain open in every direction.

Four drill rigs currently operate on site across double shifts. The company continues to find new high-grade gold mineralisation nearby. This exploration success will drive further resource expansion very soon.

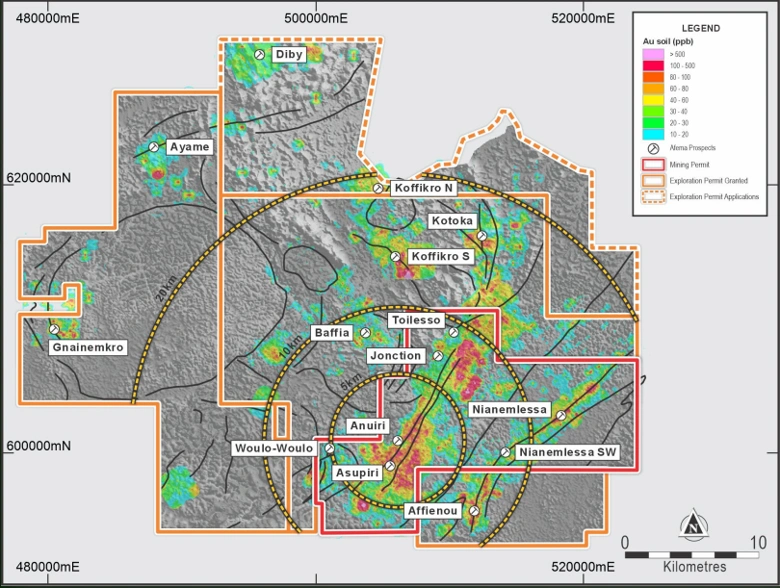

Fig 9: Afema Shear [ASX Announcement]

Comparison to African Peers

Afema easily beats most peer projects across West Africa. The capital intensity sits at a low US$2,094 per annual ounce. The peer median capital intensity is much higher at US$2,582.

The project delivers higher annual production than most regional competitors. Its cost structure places it firmly in the lower half of the curve. These facts make Turaco a standout investment on the ASX.

The management team brings a proven track record to the table. Managing Director Justin Tremain successfully built West African gold companies before. This experience gives the market confidence in project delivery.

Fig 10: Afema Project [ASX Announcement]

Corporate Strength and Timeline

Turaco maintains a corporate structure with excellent backing. The company holds over A$60 million in cash reserves. Institutional and corporate investors own 42 percent of the register.

The enterprise value sits at a tight A$450 million today. The current share price reflects upcoming catalyst potential. A Definitive Feasibility Study will commence immediately in late 2026.

The company expects the final study results by mid-2027. Construction will follow shortly after the final investment decision. Shareholders can look forward to fast asset progression.

Fig 11: 35km of Afema Shear strike [ASX Announcement]

Outlook for Côte d’Ivoire

Côte d’Ivoire has become a premier mining jurisdiction globally. The country has more than doubled its gold output over the last decade. It now boasts nine operating gold mines.

The government offers excellent political stability and modern mining laws. Permitting processes attract major international capital to the region. The sovereign rating remains the highest in sub-Saharan Africa.

The modern Côte d’Ivoire mining industry outlook encourages major gold production growth. This supportive framework allows projects like Afema to thrive. The next decade will belong to Ivorian gold miners.

Also read: The ASX Wealth Blueprint Australians Will Follow for the Next Decade

FAQ

1.What makes the Afema project unique?

ANS. The project combines huge scale with low-risk infrastructure and high profit margins. This rare combination sets it apart from other global gold assets in the current market.

2.How is Turaco Gold positioned for the next decade?

ANS. Turaco Gold sits perfectly to capture immense value over the next ten years. The company focuses heavily on operational efficiency to maximise its financial returns.

3.What is the outlook for gold mining in Côte d’Ivoire?

ANS. The gold mining future in Côte d’Ivoire looks brighter than ever before. Efficient operators will lead the region and unlock major value across these rich greenstone belts.

Also read: Australia’s Gold Sector Gains Momentum with Bellevue’s Tribune South Drilling

Disclaimer

This article is meant only for informational purposes. If you are an investor who is watching Mineral Resources Limited closely, all the data published in the content is sourced from ASX announcements and external sources. Kindly verify all information related to the share price and market data. Any investment should be made at the investor’s own risk. Colitco does not hold any position in the above-mentioned Company

Source :

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.