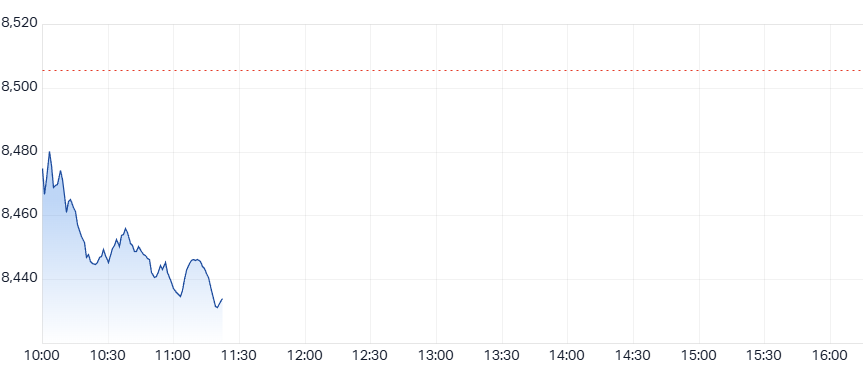

S&P/ASX 200 opens lower

The S&P/ASX 200 futures fell 20 points or 0.23% early Monday after the US struck Iranian nuclear sites on Sunday. Markets responded to the geopolitical tensions with volatile movements in oil, gold, and the US dollar as investors digested headlines. The attack raised risk sentiment globally, triggering initial gains in safe havens before fading through the morning session.

Figure 1: ASX 200 as on 11:22 AEST

Oil, gold and US dollar pare gains

Brent crude rallied 4.1% to US$80.34 a barrel around 8:00 am AEST and now sits at US$78.84, up 2.1%. Gold surged 0.80% to US$3,398 per ounce before settling at US$3,376, a 0.15% increase from Friday’s close. The US Dollar Index opened 0.34% higher at 99.1 and is now up 0.18% at 98.95 as risk sentiment stabilised.

Broker downgrades weigh on resource stocks

UBS downgraded several resource heavyweights including Fortescue, Pilbara Minerals and Liontown Resources.

Fortescue Metals dropped to Neutral from Buy with its target cut from $17.50 to $16.

Liontown Resources was downgraded to Sell from Neutral, with the target price maintained at $0.50.

Pilbara Minerals was downgraded to Neutral from Buy, with a revised target of $1.30, down from $1.60.

IGO Limited fell to Neutral from Buy, with UBS cutting its target from $4.40 to $4.10.

Other broker actions across sectors

ANZ was downgraded to Sell from Neutral by UBS, with its target reduced to $26.50 from $30. REA Group received a Hold from Buy downgrade by BP, with the price target falling from $267 to $262. Lovisa was upgraded to Neutral from Sell, with UBS lifting its target from $26 to $30. Macquarie downgraded Lynas Rare Earths to Underperform from Neutral, with the target price unchanged at $8.00. “LYC’s recent share price performance has exceeded our target and the underlying NdPr prices,” Macquarie stated.

Adairs plunges on margin deterioration

Adairs shares dropped 31% after a weak FY25 trading update. Group sales for FY25 were flagged at $614-618 million, up around 6.1% year-on-year. Underlying EBIT rose approximately 1.2% to $53.5-57 million. Second-half sales came in at $303.5-307.5 million, up 5.7% compared to 2H24. However, EBIT declined 9.2% to $20.5-24.0 million as margin pressures intensified. Adairs stated promotional activity to manage inventory and drive sales adversely impacted gross margins.

Spark New Zealand exits Hutchison Australia stake

Spark New Zealand accepted Hutchison Telecommunications Amsterdam BV’s offer to divest its 10% stake in Hutchison Australia. HTABV’s bid offered 3.2 cents per share, a 52% premium on the last traded price. “The decision to divest the shareholding is consistent with Spark’s current strategic review of non-core assets,” said Spark. The deal is expected to deliver NZ$47 million in July 2025 and reduce Spark’s debt load.

Santos takeover faces regulatory scrutiny

South Australia’s government called for ADNOC to maintain Santos’ headquarters in Adelaide amid a $36 billion takeover offer. Energy Minister Tom Koutsantonis said jobs and investment in the Cooper Basin must remain priorities for the state. The government is conducting a cost-benefit analysis to assess the impact on gas supply and local infrastructure. Concerns persist that LNG exports may be prioritised over domestic supply if ADNOC proceeds.

Metcash delivers in-line FY25 results

Metcash reported full-year results aligned with its June trading update, showing revenue growth of 8.9% to $17.3 billion. Underlying EBIT rose 2.3% to $507.8 million, within guidance of $504-508 million. Net profit after tax dipped 2.4% to $275.5 million, staying within forecast range. A final dividend of 9.5 cents beat UBS expectations by 6.7%. The company’s early FY26 data showed group sales rose 4.7%, or 2.7% excluding tobacco and Superior Foods. Supermarket sales climbed 2.9% while food sales excluding tobacco jumped 17%. Hardware sales rose 1.1%, cycling acquisitions made last March.

SHAPE Australia posts strong FY25 finish

Construction firm SHAPE Australia posted strong unaudited results for FY25, with revenue up ~14% to $950-960 million. EBITDA rose ~25% to $32-33 million and NPAT increased ~31% to $20.5-21.5 million. Backlog orders held steady at $460 million. Despite limited coverage, the stock gained 35% year-to-date and is up 72% over twelve months.

Lendlease price target lowered on weaker assumptions

Citi downgraded Lendlease’s target price to $6.80 from $7.50, citing lower profit assumptions. FY25 earnings slightly improved due to recent asset sales including Capella Capital. The share buyback depends on closing further sales of the Retirement and Malaysian TRX assets. Citi flagged uncertainty in Lendlease’s funds management arm with a potential ~$10 billion AUM outflow. This could impact 4-5% of earnings and dampen long-term growth prospects.

PMIs reveal modest growth in private sector

Australia’s composite PMI rose to 51.2 in June from 50.5 in May, reaching a three-month high. Services sector expansion drove the gains, while manufacturing stabilised after a May decline. New domestic orders rose as export demand fell, impacted by US trade policy changes. Employment increased for the sixth straight month, though hiring slowed from May’s pace. Firms cleared backlogs at the fastest rate in seven months. Input cost inflation hit a seven-month low while output prices dropped to a four-year low due to competition.