Broker Shaw and Partners has issued fresh ratings on three major Australian energy companies this week. AGL Energy Limited (ASX: AGL), Origin Energy Ltd (ASX: ORG), and Woodside Energy Group Ltd (ASX: WDS) each received a different verdict, reflecting contrasting views on risk, income, and long-term positioning across the sector.

![]()

Figure 1: Shaw and Partners financial advisory firm logo [Courtesy: Shaw and Partners]

For investors assessing the best ASX energy stocks, the divergence in ratings signals that not all energy names are being treated equally at current valuations. The analysis, published via The Bull, highlights execution risk, regulatory uncertainty, and commodity price volatility as the key considerations shaping each call.

1. AGL Energy Earns a Hold as Transition Risks Linger

Shaw and Partners rates AGL Energy as a hold at current levels. The broker acknowledges the Company’s scale and essential service positioning within Australia’s energy sector but points to ongoing structural challenges as the reason for restraint.

Figure 2: AGL Energy corporate signage at its Australian operations facility [Courtesy: AFR]

Earnings Stability Has Improved, but Execution Risk Remains

Shaw and Partners outlined its thinking on AGL Energy in detail. The broker noted that AGL provides exposure to Australia’s energy sector during a period of structural change and that earnings stability has improved. However, asset transition challenges and evolving policy settings continue to create uncertainty.

“AGL warrants a hold rating, balancing its strategic importance against longer term capital requirements,” Shaw and Partners said.

2. Origin Energy Share Price Backed by a Buy Rating

Shaw and Partners is notably more constructive on Origin Energy, assigning a buy rating this week. The broker points to an attractive income profile and leveraged exposure to Australia’s evolving energy market as the primary reasons for its positive view on the Origin Energy share price.

Figure 3: Origin Energy office building and branding in Australia [Courtesy: Market Index]

Yield Appeal Meets Energy Transition Exposure

Origin Energy benefits from scale in both electricity generation and retailing. Shaw and Partners noted that the Company’s yield remains appealing in a market that is still sensitive to income certainty. The broker described Origin as well placed to balance defensive income characteristics with longer-term energy transition opportunities.

That said, Shaw and Partners was direct in flagging the risks that accompany the buy call.

“Regulatory risk and energy price volatility remain key risks. We see Origin as well placed to balance defensive income characteristics with longer-term opportunities tied to the domestic energy transition,” Shaw and Partners said.

3. Woodside Energy Rated a Sell Despite Recent Share Price Strength

Shaw and Partners has issued a sell rating on Woodside Energy this week, advising investors to take advantage of the recent rise in the Company’s share price. The call is notable given that Woodside has historically been a key reference point for the best ASX energy stocks and discussions around the Woodside Energy dividend 2026.

Figure 4: Woodside Energy exhibition booth showcasing LNG and offshore operations [Courtesy: Reuters]

Capital Intensity and Project Execution Risk Drive the Sell Call

The broker’s concern centres on Woodside’s long-dated development timelines and its track record of missing market expectations. Shaw and Partners noted that the current commodity environment has supported the share price but characterised the rally as an exit opportunity rather than a reason to add exposure.

“This energy giant has historically struggled to consistently meet market expectations. While the current commodity environment has supported its share price, we see this as an opportunity to exit. Capital intensity, project execution risk and long-dated development timelines remain my concerns,” Shaw and Partners said.

The broker noted that Woodside shares rose from A$23.59 on 9 Jan 2026 to A$35.80 on 7 Apr 2026 before pulling back to A$33.37 on 9 Apr 2026. The share price movement has also been influenced by volatile crude oil prices resulting from the Middle East conflict.

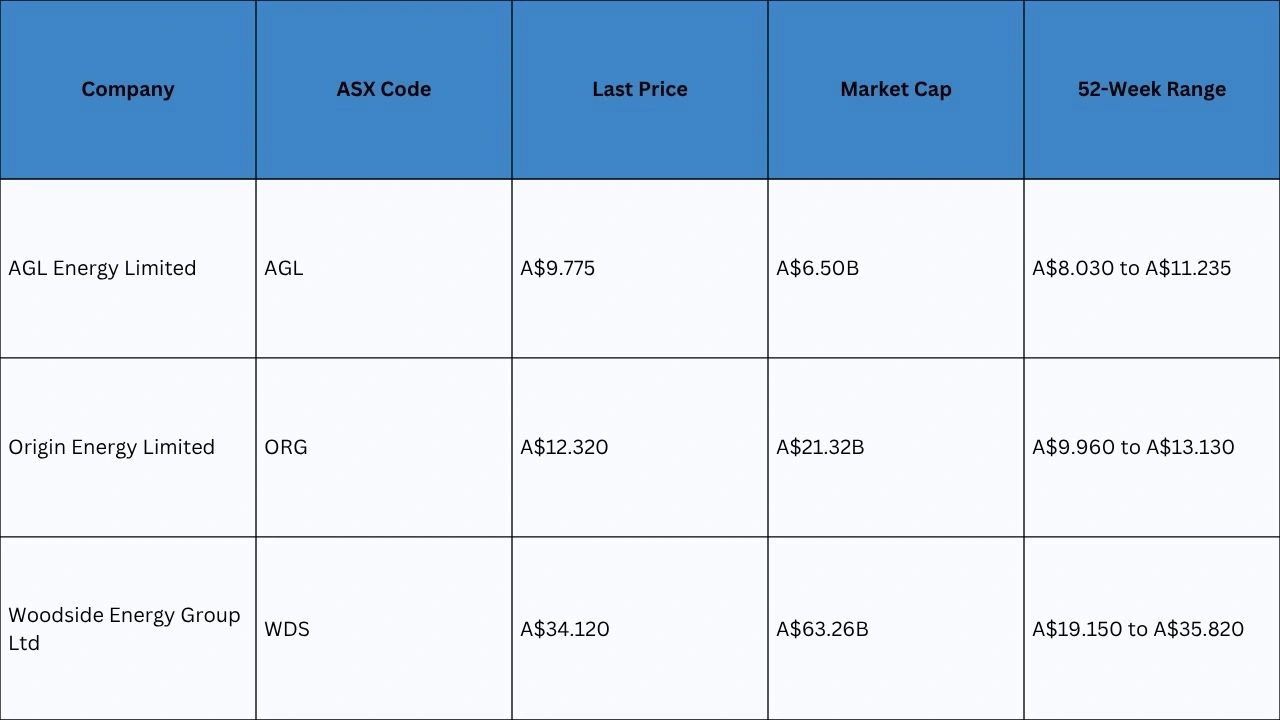

Share Price Snapshot

Industry Outlook

Australia’s energy sector is navigating a period of structural transition as the domestic grid moves away from coal-fired generation and toward renewable and gas-backed capacity. Regulatory settings remain in flux, with policy uncertainty continuing to affect capital allocation decisions across the sector.

Global oil and gas prices remain sensitive to geopolitical developments, particularly in the Middle East, which continues to introduce volatility into the earnings profiles of Australian energy exporters. For investors focused on the best ASX energy stocks and the Woodside Energy dividend 2026, the current environment rewards selectivity over broad sector exposure.

Future Direction and Impact on ASX Energy Investors

The Shaw and Partners ratings provide a clear framework for investors navigating these three names:

- AGL Energy is rated hold, with earnings stability improving but execution and policy risk keeping the broker on the sidelines

- Origin Energy share price is backed by a buy rating, supported by income appeal and domestic energy transition leverage

- Woodside Energy is rated sell, with the broker viewing the recent share price rally as an opportunity to reduce exposure

- Woodside shares rose from A$23.59 to A$35.80 between 9 Jan 2026 and 7 Apr 2026, a significant move Shaw and Partners believes has run its course

- Regulatory risk, energy price volatility, and capital intensity remain the dominant concerns across all three names

- Investors tracking the Woodside Energy dividend 2026 should weigh the sell rating against the Company’s commodity-linked earnings outlook

Frequently Asked Questions

Q1. What is Shaw and Partners’ rating on Origin Energy?

Ans. Shaw and Partners rates Origin Energy as a buy, citing an attractive income profile and leveraged exposure to Australia’s domestic energy transition.

Q2. Why is Woodside Energy rated a sell?

Ans. Shaw and Partners views the recent share price rally as an exit opportunity, citing capital intensity, project execution risk, and long-dated development timelines as key concerns.

Q3. What is the current Origin Energy share price?

Ans. Origin Energy (ASX: ORG) is currently trading at A$12.320 per share, with a market capitalisation of A$21.32 billion.

Q4. Why does AGL Energy have a hold rating?

Ans. Shaw and Partners acknowledges AGL’s scale and essential service positioning but cites ongoing asset transition challenges and evolving policy settings as reasons to hold rather than buy.

Q5. Are these among the best ASX energy stocks to watch in 2026?

Ans. Shaw and Partners sees clear differences between the three. Origin Energy is its preferred pick among the best ASX energy stocks currently, while Woodside is rated a sell and AGL a hold.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or investment advice. All content is based on reporting published on 13 Apr 2026, sourced from analyst commentary provided by Shaw and Partners via The Bull. Share price and market capitalisation data reflect figures provided at the time of publication. Investing in securities involves risk. Readers should conduct their own research and seek independent financial advice before making any investment decisions. Colitco does not hold any position in the companies or organisations mentioned.

Sources

https://www.fool.com.au/2026/04/13/buy-hold-sell-agl-origin-energy-and-woodside-shares/

https://www.asx.com.au/markets/company/AGL

https://www.asx.com.au/markets/company/ORG

https://www.asx.com.au/markets/company/WDS

Last modified: April 14, 2026