Any Australia interest rate forecast 2026 worth reading starts with a boring fact. The Reserve Bank did nothing at its last meeting, and doing nothing was the whole message.

The board left the cash rate at 4.35 per cent, its first hold of the year after three straight rises, and the vote was unanimous. No dissent. No hedging.

Then the mood shifted. Westpac moved its first-cut call forward, headlines followed, and suddenly borrowers were asking whether relief had arrived early.

It hasn’t. Read the fine print and the “early” cut is still more than a year away.

Three hikes in six months changed the mood, not the maths

Australia started 2026 with a cash rate of 3.60 per cent. Three quarter-point rises later, it is 4.35 per cent.

Those hikes were a response to the energy shock triggered by the Iran war. Petrol went up. Freight went up. Everything that moves on a truck followed.

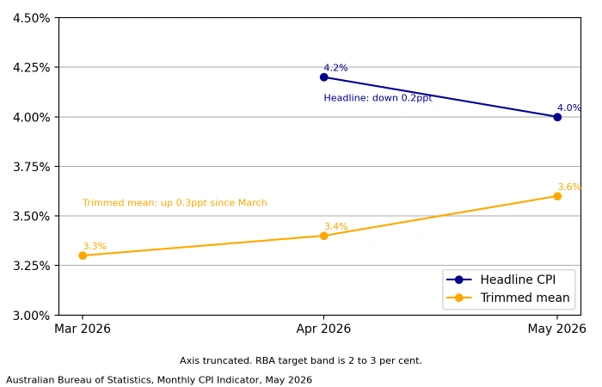

Here is the part most coverage skips. Headline inflation actually eased to 4.0 per cent in May from 4.2 per cent as fuel costs fell, but core inflation went the other way, with the trimmed mean climbing from 3.4 per cent to 3.6 per cent.

Read that twice. The number that grabs attention is falling. The number the RBA actually targets is rising.

That gap is the entire fight. Oil prices spike, then fade. But once a cafe reprints its menu, the price stays printed.

Headline inflation eased to 4.0 per cent in May while the trimmed mean rose to 3.6 per cent.

The Reserve Bank of Australia interest rate decision hinges on one number

Mark 29 July in the diary. The June quarter inflation figures land that day, and they will settle whether the RBA hikes again in August.

Not whether it cuts. Whether it hikes.

Westpac still has two more rises pencilled in, taking the cash rate to 4.85 per cent. The same bank that just brought its cut forward is also the most hawkish on the way up. Both things are true at once, and that tells the story of this cycle better than any forecast table.

The labour market is not helping the doves either. Unemployment slipped back to 4.4 per cent in May from April’s four-year high of 4.5 per cent, with employment jumping by 40,300 people.

A cooling economy does not usually add forty thousand jobs in a month.

Then there is the sleeper. The Fair Work Commission handed down a 4.75 per cent minimum wage rise from 1 July 2026, close to double the RBA’s inflation target midpoint.

Wages that size do not pass through an economy quietly. They show up in services prices about two quarters later, right when the RBA hopes to be declaring victory.

The 2025 cut still haunts Martin Place

To understand why the RBA is dragging its feet, go back a year.

The bank cut rates in 2025. Inflation then picked up again through the second half of that year. The board effectively had to undo its own work, and undo it in public.

Westpac’s own reasoning leans on this: the RBA will want clear evidence inflation is beaten before it eases again, precisely because it moved early last time and got burned.

Central bankers do not forget that. Credibility is the only thing they actually own.

Assistant Governor Sarah Hunter put the trade-off plainly this month, warning that central banks cannot always look through supply shocks, and that if inflation expectations shift, getting back to stability may require a period of low inflation and higher unemployment.

That is not the language of a bank about to cut. That is a bank telling the country the bill might come due in jobs.

What an RBA cash rate forecast for Australia in 2026 actually buys a borrower

Nothing. That is the honest answer.

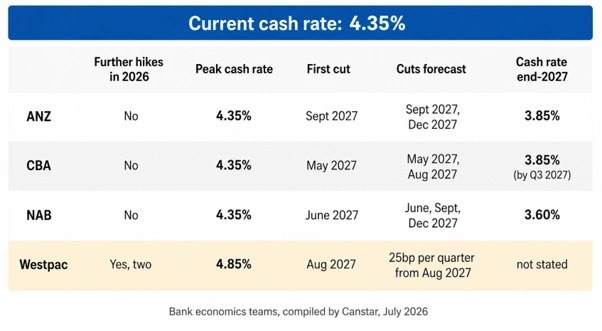

ANZ has cuts in September and December 2027. CBA has May and August 2027. NAB sees three cuts through 2027 taking the rate to 3.60 per cent. Westpac’s “brought forward” call starts in August 2027.

Notice the pattern. Every single one of them is a 2027 story.

The RBA’s own May forecasts had trimmed mean inflation above 3 per cent until the middle of 2027, only reaching 2.5 per cent by early 2028. The banks are not disagreeing with the RBA. They are just being slightly more optimistic about the same slow grind.

So the practical read for a household on a variable loan in 2026 is simple. Budget for 4.35 per cent, and stress-test for 4.85 per cent. Anyone budgeting for relief this year is planning around a forecast that does not exist.

For anyone holding ASX bank stock, the calculus flips. Higher-for-longer supports net interest margins, which is the quiet reason the big four have been comfortable through this cycle. The risk sits in arrears, and arrears lag rate rises by roughly a year. That clock started in February.

All four major banks now expect the first cut in 2027, not 2026.

The market has spent six months arguing about a rate cut that is thirteen months away, while ignoring the hike that might arrive in four weeks. Our earlier look at CBA’s 2026 rate call flagged this tightening turn well before consensus caught up, and the RBA household outlook piece unpacked how quickly the mortgage squeeze reaches everyday budgets.

Investors weighing the flip side can read the drivers behind CBA’s share price, while the housing market warning on rate cuts explains why relief, when it finally lands, brings its own problem.

The next Reserve Bank of Australia interest rate decision comes on 11 August at 2.30pm. Watch the trimmed mean on 29 July, and ignore the petrol price. The RBA already has.

Also Read: NEXTDC Upsizes Senior Debt Facilities to A$2.3 Billion

FAQs

Q: What is the RBA cash rate right now?

A: 4.35 per cent, held unchanged in June.

Q: Will the RBA cut rates in 2026?

A: No major bank forecasts a cut before 2027.

Q: Could rates rise again this year?

A: Yes. Westpac expects two more rises to 4.85 per cent.

Q: When is the next RBA meeting?

A: 11 August 2026.

Q: Why is inflation still high?

A: Fuel costs have eased, but underlying price pressure has not.

Q: What should borrowers do?

A: Plan around 4.35 per cent and stress-test higher.

Disclaimer:

This article is general in nature and does not constitute financial product advice. It does not take into account your objectives, financial situation or needs. Consider seeking advice from a licensed financial adviser before making any investment decision. COLITCO LLP accepts no responsibility for any claim, loss or damage arising from the information provided or its accuracy.

Source:

https://www.fool.com.au/2026/07/11/could-the-rba-start-cutting-interest-rates-sooner-than-expected/

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.