Carbonxt Group Limited (ASX: CG1) (Carbonxt or the Company) has agreed a restructuring plan with its two largest financial stakeholders, Phelbe Pty Ltd and Pure Asset Management, aimed at strengthening the balance sheet as its Kentucky activated carbon facility moves towards commercial production.

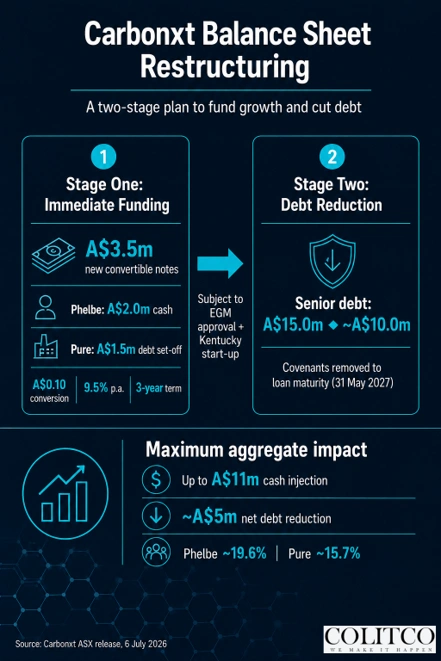

The plan, announced on 6 July 2026, runs in two stages. The first delivers immediate funding through A$3.5 million of new convertible notes. The second, subject to shareholder approval and the start of Kentucky operations, sets a clear path to reduce senior debt and simplify the capital structure.

Both backers are lifting their commitment at a point when the Company says its underlying business is generating positive operating cash flow and gross margins above 45 per cent. That mix of fresh capital and lower gearing sits at the centre of the announcement.

The Restructuring at a Glance

The headline terms of the plan are as follows:

- Phelbe and Pure will collectively subscribe for A$3.5 million of convertible notes, with Phelbe providing A$2.0 million in cash and Pure’s A$1.5 million set off against debt and interest on its senior loan.

- Subject to shareholder approval and the start of Kentucky operations, senior debt would fall from A$15.0 million to about A$10.0 million.

- A 10 per cent per annum early-conversion incentive will be offered to all option and convertible note holders, excluding warrants, to bring forward conversions and exercises.

- On completion, Phelbe and Pure would hold approximately 6 per cent and 15.7 per cent of the Company respectively.

- The plan’s maximum aggregate impact is an estimated cash injection of up to A$11 million and a net debt reduction of about A$5 million.

Figure 1: Infographic mapping the two-stage restructuring, from the A$3.5 million note subscription through to the senior debt reduction. [Source: Carbonxt ASX release, 6 July 2026]

Stage One Delivers Immediate Funding

Under the first stage, which completes immediately, Phelbe will subscribe for A$2.0 million of new convertible notes in fresh cash. Those funds support near-term operations and the continued commissioning of the Kentucky facility.

Pure will subscribe for A$1.5 million of convertible notes. Rather than new cash, Pure’s subscription is set off against outstanding debt and accrued interest on the existing senior loan facility.

The notes carry a three-year term, a conversion price of A$0.10 per share and interest of 9.5 per cent per annum. For every two shares issued on conversion, one unlisted option attaches, exercisable at A$0.10. That equates to 10 million options for Phelbe and 7.5 million for Pure.

Of the A$3.5 million, A$3.0 million of notes and the attaching options for Phelbe fall under the Company’s existing placement capacity under ASX Listing Rule 7.1. The remaining A$0.5 million of notes and the attaching options for Pure require shareholder approval. Pure has also agreed to provide any required covenant waivers to 31 December 2026.

| First-Stage Convertible Notes | Terms |

|---|---|

| Total issue size | A$3.5 million |

| Phelbe subscription | A$2.0 million (new cash) |

| Pure subscription | A$1.5 million (set off against debt and interest) |

| Conversion price | A$0.10 per share |

| Interest rate | 9.5 per cent per annum |

| Term | 3 years |

| Security | Pari-passu with existing senior debt (Pure) |

Table 1: Summary of the first-stage convertible note terms. [Source: Carbonxt ASX release, 6 July 2026 ]

Stage Two Targets the Senior Debt

The second stage is conditional. It requires approval by shareholders at an extraordinary general meeting (EGM) and the commencement of operations at the Kentucky facility. Commencement is defined as independent engineer certification that the plant is operational, together with an initial revenue milestone of US$1 million.

Once both conditions are met, Phelbe will convert its notes at approximately A$0.075 per share, expected to raise about A$3.4 million in cash.

Pure will exercise its warrants at approximately A$0.07 per share, with proceeds of approximately A$4.97 million applied directly to the senior debt facility, reducing it from A$15.0 million to about A$10.0 million. Pure will also remove all financial covenants for the remaining life of the senior loan, which matures on 31 May 2027.

Each conversion and exercise price, including those reduced by the incentive, sits above the Company’s share price of A$0.068 referenced in the announcement.

Why the Timing Points to Kentucky

The restructuring is timed to the Kentucky activated carbon facility moving into production. The Company describes the plant as a potential uplift of more than 200 per cent in group sales capacity.

Activated carbon is a treated, highly porous form of carbon used to capture pollutants from air and water. The Kentucky plant is built to serve the liquid-phase market, which treats water and is considerably larger than the air-phase market the Company supplies today.

Management frames a lower-geared balance sheet as the flexibility needed to capture that opportunity as revenue scales.

Managing Director’s View

Carbonxt Managing Director Warren Murphy said the timing reflected both the Kentucky ramp-up and the strength of the underlying business.

“With the Kentucky facility moving into production and our underlying business delivering stronger operating cash flow and gross margins, this is the right moment to strengthen our balance sheet. The backing of both Phelbe and Pure reflects a shared confidence in the Company’s direction and a clear preference for building long-term value alongside the Company. As Kentucky ramps and our liquid-phase activated carbon revenues grow, a materially de-geared balance sheet will allow us the flexibility needed to capitalise fully on the significant opportunity in front of us.”

Shareholder Approvals and the 20 Per Cent Threshold

Several elements of the recapitalisation require shareholder approval, to be sought at an EGM expected in August 2026.

The resolutions include amendments to the terms of existing options to allow the 10 per cent per annum early-exercise discount.

Shareholders will also be asked to approve, under item 7 of section 611 of the Corporations Act, an increase in Phelbe’s voting power above 20 per cent, to approximately 23 per cent, without a takeover bid.

That increase would arise from Phelbe converting its remaining convertible notes into equity at A$0.10 per share and exercising its remaining options. Approximately A$0.4 million would be raised in cash, with about A$4.2 million of debt converted into equity.

A Notice of Meeting, together with an Independent Expert’s Report on the section 611 resolution if required, will be sent to shareholders. Phelbe and its associates will be excluded from voting on the resolution to which they are a party.

Early-Conversion Incentive Open to All Option Holders

The early-conversion incentive is not limited to the two major backers. It will be offered to all of the Company’s option holders and lapses on 31 December 2026, after which exercise prices revert to their original terms.

Carbonxt, Pure and Phelbe are committed to the restructuring regardless of wider participation. If every option holder took up the discount, the Company estimates it could raise approximately A$6.0 million in cash.

Subject to increased customer demand, those proceeds would fund an expansion of one of the Company’s three facilities or retire debt.

The Activated Carbon Market Backdrop

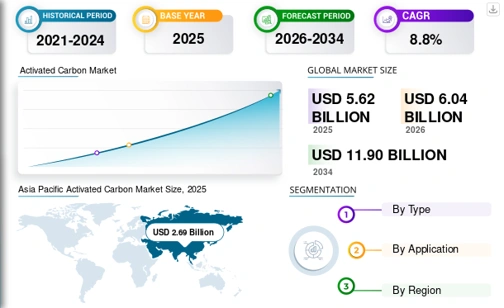

Carbonxt sells into a market shaped by tightening environmental rules. The global activated carbon market was valued at about US$5.62 billion in 2025 and is forecast to reach roughly US$11.9 billion by 2034, a compound annual growth rate of 8.8 per cent, according to Fortune Business Insights.

Water treatment is the largest end-use, accounting for about 42.5 per cent of the market in 2025, according to Grand View Research. Demand is being driven in part by United States rules on PFAS, the group of long-lasting “forever chemicals” that activated carbon is used to strip from drinking water.

Carbonxt manufactures in the United States, which positions it to supply utilities and industrial customers seeking a domestic source as those rules tighten.

Figure 2: Global activated carbon market size, 2025 to 2034 (US$ billion). [Source: Fortune Business Insights]

Investors’ Outlook

Carbonxt heads into the second half of 2026 with its Kentucky plant close to production and a plan in place to lower its gearing. The Company frames the recapitalisation as both a source of near-term capital and a step towards a simpler balance sheet.

The estimated maximum aggregate impact underlines the scale of the plan.

| Post-Completion Snapshot | Detail |

|---|---|

| New convertible notes (Stage 1) | A$3.5 million (Phelbe A$2.0m cash, Pure A$1.5m set-off) |

| Senior debt | Reduced from A$15.0m to about A$10.0m |

| Senior loan maturity | 31 May 2027 |

| Phelbe holding on completion | ~19.6 per cent |

| Pure holding on completion | ~15.7 per cent |

| Maximum aggregate cash injection | Up to about A$11 million |

| Maximum aggregate net debt reduction | About A$5 million |

| EGM | Expected August 2026 |

Table 2: Indicative post-completion snapshot of the restructuring. [Source: Carbonxt ASX release, 6 July 2026]

| Carbonxt Group (ASX: CG1) | Value |

|---|---|

| Last Price (ASX: CG1) | A$0.068 |

| 52 Week Range | A$0.054 – A$0.115 |

| Market Capitalisation | A$29.46M |

Table 3: CG1 share price data. [Source: ASX]

Key catalysts to watch in the months ahead include:

- Extraordinary general meeting, expected in August 2026, covering the section 611 resolution and option-term changes

- Commencement of Kentucky operations, certified by an independent engineer and an initial US$1 million revenue milestone

- Senior debt reduction from A$15.0 million to about A$10.0 million under Stage Two

- Take-up of the early-conversion incentive, which lapses on 31 December 2026

Disclaimer

This article has been prepared by Colitco in collaboration with Carbonxt Group Limited as part of a commercial content and investor communications arrangement. Colitco may receive compensation for the production and distribution of this content. This article is intended for informational purposes only and does not constitute financial product advice, investment advice, or a recommendation to buy or sell any securities. The content reflects information available at the time of publication and may not be updated. All figures, data and statements have been sourced from Carbonxt Group Limited’s official ASX announcements and publicly available sources. Readers should conduct their own independent research and seek professional financial advice before making any investment decisions. Past performance is not a reliable indicator of future results. All dollar amounts are in Australian dollars unless otherwise stated.

Elizabeth Jones is a finance and mining content specialist with over 10 years of experience creating clear, SEO-driven content across fintech, investing, banking, insurance, cryptocurrency, and resource markets. She transforms complex financial data and industry trends into engaging, reader-focused articles that improve understanding and audience engagement.