Rio Tinto shares have done the heavy lifting for copper bulls this past year. The stock sits near $180. It has climbed roughly 65% in twelve months, riding the same copper wave that pushed the metal to a record on the London Metal Exchange back in January.

That run is exactly the problem.

A stock that has already doubled the market leaves little room to surprise. Brokers now treat Rio as fully valued. So where does the next leg of upside come from?

Bell Potter reckons it comes from a much smaller name most retail investors have never typed into their watchlist.

The stock is AIC Mines (ASX: A1M). Company operates one mining project – Eloise Copper Project, which is situated 60 kilometers south-east of Cloncurry in North Queensland.

On June 29, Bell Potter reiterated “Buy” recommendation and increased price target to AUD 1.00 per share. Current stock price stands at around AUD 0.705, implying that there is 42% upside potential within the next 12 months.

Why a single-mine copper producer is drawing broker attention

Here is the counterintuitive bit. AIC Mines is tiny next to Rio. It has the capacity to produce between 12,000 and 13,000 tonnes of copper annually.

The production from the copper unit of Rio alone is higher in two weeks.

Small can move faster, though.

Eloise is in the middle of an expansion. The processing plant is being lifted from a nameplate of 725,000 tonnes a year to 1.1 million tonnes.

The goal is to push copper output towards 20,000 tonnes a year. That is a step-change of more than 50% from a single asset, funded and already under construction.

Bell Potter visited the site recently and came away comfortable. The ball mill has been installed on its foundations. Structural steel is largely up.

The crushing circuit is 95% mechanically complete, with dry commissioning planned for July. Eight of nine tie-ins between the new and existing circuits are done.

That level of detail matters. Mine expansions slip all the time. Concrete numbers from a site walk-through carry more weight than a press release promising things are “on track.”

The copper price did the work, and that cuts both ways

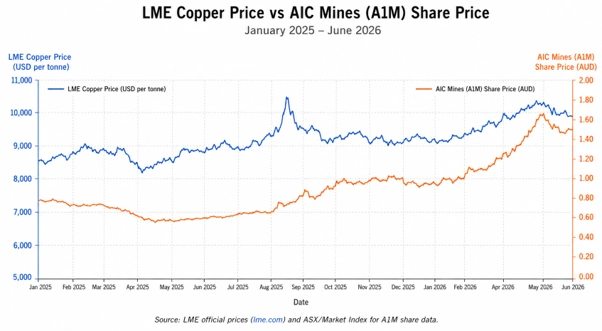

Copper hit US$14,527 per tonne on the LME on 29 January 2026. An all-time high. The metal has since cooled to around US$6.14 a pound, still up about 21% on a year ago.

The drivers behind the spike are worth understanding. Supply disruptions at major mines. US tariffs’ uncertainty that led to a stockpile build-up.

And the less dramatic but ever-present story: electrification, infrastructure improvements, and insatiable copper demand from the AI data centres.

A producer like AIC Mines is geared straight to that price. As long as there is a rise in the price of copper, it benefits the miners through their margins. The March 2026 quarter showed it.

Eloise mined 3,432 tonnes of copper and 1,692 ounces of gold at the very low all-in sustaining cost of AUD 4.18 per pound. Net mine cash flow hit AUD 27.7 million in three months, more than the company generated across all of the prior financial year.

But leverage runs in reverse too. If copper drops, a single-asset miner has nowhere to hide. Rio can lean on iron ore. AIC Mines cannot. That is the trade-off buried inside the bigger upside.

Copper’s record run in early 2026 and AIC Mines’ share price, January 2025 to June 2026.

What separates AIC Mines from the usual junior explorer punt

Plenty of ASX small-caps promise copper riches. Most are holes in the ground with a story attached. AIC Mines actually digs the metal up and sells it.

The track record backs that. The company has met its production and cost guidance for eleven straight quarters. For a single mine running through a rain-hit North Queensland wet season, that consistency is rare.

There is a growth pipeline behind the headline mine as well. The nearby Jericho copper deposit hit first ore production during the March quarter, ahead of schedule.

Combined mineral resources across the project rose 10% to 31.2 million tonnes, the largest resource base in Eloise’s 30-year history. And the expanded plant is physically sized for 1.5 million tonnes a year, leaving room for a cheap second-stage lift later without a fresh capital raise.

Cash sits at AUD 31.1 million. No headline debt drama. The expansion is funded.

None of this makes it a safe bet. It is a small miner with one revenue source, exposed to a volatile metal and the weather in a remote corner of Queensland.

Diesel costs were flagged as a cost pressure for the June quarter. The expansion still has to commission cleanly in December.

What it does make AIC Mines is a genuine alternative for an investor who wants copper exposure and thinks Rio has already had its run. Bell Potter’s $1.00 target is one broker’s view, not a guarantee.

The case rests on a simple idea. A small producer finishing an expansion into a tight copper market has more to gain from here than a giant trading near its ceiling.

Also Read: Worley class action heads to the High Court

FAQs

Q: Is AIC Mines a pure copper stock?

A: Mostly. It produces copper with a small gold by-product from the Eloise mine in Queensland.

Q: What is Bell Potter’s price target for AIC Mines?

A: AUD 1.00 per share on 29 June 2026.

Q: Why pick AIC Mines over Rio Tinto for copper?

A: Rio is seen as fully valued after a strong year. A smaller producer mid-expansion offers more leverage to the copper price.

Q: When does the Eloise expansion finish?

A: Commissioning is expected in December 2026 quarter.

Q: What is the main risk?

A: A single-mine company has no fallback if copper prices fall or the expansion runs into trouble.

Disclaimer:

This article is general information only and does not constitute financial product advice. COLITCO LLP accepts no responsibility for any claim, loss or damage arising from the information provided or its accuracy. The information is general in nature. Speak to a licensed financial adviser before making any investment decision.

Source:

https://www.fool.com.au/2026/06/29/forget-rio-tinto-and-buy-this-asx-copper-share-2/

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.