The Australia mining outlook for 2026 starts with an odd fact. Rio Tinto, Fortescue and BHP all went backwards last month, even as the wider market crept higher. The S&P/ASX 200 added 0.5% in June. The big miners did the opposite.

Here is how the month ended:

- BHP: down 4.7%, closing June at $59.40

- Fortescue: down 4.2%, at $19.15

- Rio Tinto: down 7.1%, at $172.51

None of that spells trouble on its own. Over the past year BHP is still up around 60%, Rio about 57%, and Fortescue near 19%. The June dip was small. What sits behind it is the interesting part.

Iron ore slipped from US$108 a tonne at the end of May to US$100 by 30 June. Copper eased too. For three companies that still earn most of their money digging red dirt out of the Pilbara, a softer iron ore price gets felt fast.

Here is the twist. The company doing the most to push iron ore prices down is Rio Tinto itself.

Simandou changes the maths for the Australia mining outlook

The mine pushing prices lower is one Rio Tinto helped build.

Simandou sits in Guinea, West Africa. First ore left the country in December 2025. By the end of 2026 it should ship around 10 million tonnes, then climb toward 60 million over five years. Paired with its Chinese-backed neighbour, the two operations aim for 120 million tonnes a year.

The ore is the catch. Simandou grades about 65.8% iron. Pilbara ore usually sits near 62%. High-grade material at that scale arrives right as China’s steel mills make less steel, not more.

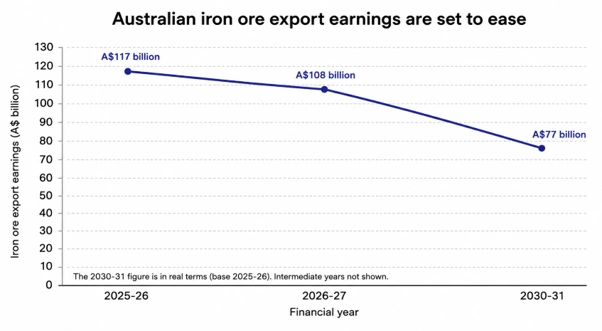

Australia’s own forecaster spelt it out this month. The government’s June Resources and Energy Quarterly sees iron ore export earnings falling from $117 billion this financial year to $108 billion next, and down near $77 billion by 2030-31 in today’s dollars.

Iron ore earnings are tipped to slide from A$117 billion to about A$77 billion by 2030-31. [Source: Department of Industry, Science and Resources.]

The benchmark price is tipped to average about US$91 a tonne across 2026 and drift toward US$64 by 2031.

There is a second layer. China set up a single state buyer, the China Mineral Resources Group, to press harder on price. It has already had a public stoush with BHP. Canberra now names it as a real risk to the benchmark.

BHP’s future strategy leans on copper, not the Pilbara

June was Mike Henry’s last month running BHP. Brandon Craig took the top job on 1 July.

Craig did not build his name on iron ore. He ran the Americas, where BHP became the world’s largest copper producer. Copper already brought in 51% of the company’s first-half profit. Iron ore, the old engine, now rides shotgun.

The plan is more copper. BHP digs around two million tonnes a year now and wants close to 2.5 million tonnes of copper equivalent by the mid-2030s.

Its Jansen potash mine in Canada is due to start in mid-2027, adding a crop nutrient to the mix.

Craig has been blunt about where the money chases growth. “There is a shift in the gravity of the business. Australia has to compete,” he said at an industry conference.

That line lands hard for a company built on Western Australian dirt. BHP’s future strategy points north and east, toward Chile, Peru, Canada and the United States.

Rio Tinto’s growth outlook now runs through Guinea and Mongolia

Rio carries the same iron ore worry and a stranger spot. It owns the mine cutting into its own Pilbara premium.

Under chief executive Simon Trott, Rio leans on breadth. Copper production rose 9% in the first quarter as the giant Oyu Tolgoi mine in Mongolia kept ramping up. Aluminium held firm. A small lithium stream even started to flow.

The Pilbara is not going quiet. In May, Rio shipped its 8 billionth tonne of iron ore from Western Australia, six decades after the first cargo sailed for Japan.

The milestone load left Cape Lambert on a ship called the Juno Horizon, bound for Nippon Steel. Rio is still pouring billions into replacement mines, including its $250 million Brockman build in the Pilbara.

But the Rio Tinto Australia growth outlook is really a copper and grade story now. Cheaper, higher-grade tonnes from Guinea plus copper from Mongolia is the hedge against a falling Pilbara price.

Fortescue stays the iron ore purist, with a power twist

Fortescue has nowhere to hide. Almost all its revenue is iron ore, and lower-grade iron ore at that, so it feels every price swing harder than the other two.

The company shipped a record haul last year and guides to 195 to 205 million tonnes for FY2026, including the newer Iron Bridge product. C1 costs sit near $17.50 to $18.50 a wet tonne. Cash stood at $4.3 billion at the last count.

The green hydrogen dream has cooled. Fortescue shelved its Arizona and Gladstone electrolyser plans and took a writedown.

Andrew Forrest, still executive chair, has swung the energy arm toward something with a buyer today: powering data centres. In April the company signed a $680 million deal to build an off-grid renewable grid for exactly that.

It is a neat pivot. Sell green power to the server farms that everyone is racing to build, rather than wait for a hydrogen market that keeps not arriving.

What the numbers are really saying

Iron ore is still Australia’s biggest export and stays that way for years. Nobody is calling a collapse.

The shift is slower and quieter. More supply from Africa and Brazil, flatter Chinese demand, and a tougher buyer all press on the price at once.

Australian output is tipped to plateau within two years near 958 million tonnes. The early signs are already showing up in trade, from China’s state buyer reshaping BHP’s shipments to last year’s move to restrict Australian ore.

So the three giants pick different roads. BHP and Rio buy diversity, mostly copper. Fortescue doubles down on iron ore and sells clean power on the side.

Even the way they run their ports splits them, as their Port Hedland strategies show. The next year tests which bet reads the market right.

Also Read: Perpetual Fund Changes 2026: Why Aboud Is Walking

FAQs

Q: Why did BHP, Rio Tinto and Fortescue shares fall in June 2026?

A: A softer iron ore price, down from US$108 to US$100 a tonne, weighed on all three.

Q: What is Simandou?

A: A huge high-grade iron ore mine in Guinea, part-owned by Rio Tinto, now shipping and set to grow.

Q: Which miner is most exposed to iron ore?

A: Fortescue, which earns nearly all its money from it and sells a lower grade.

Q: What is BHP’s future strategy?

A: More copper and potash abroad, with iron ore as the cash base rather than the growth story.

Q: Is iron ore still Australia’s biggest export?

A: Yes, and government forecasts keep it there for years, even as earnings ease.

Disclaimer:

This article is general information only and not financial advice. It does not account for your personal circumstances. Commodity prices and share prices move quickly and past performance does not predict future returns. Speak to a licensed financial adviser before making any investment decision.

Source:

https://www.fool.com.au/2026/07/04/how-rio-tinto-fortescue-and-bhp-shares-stacked-up-in-june/

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.