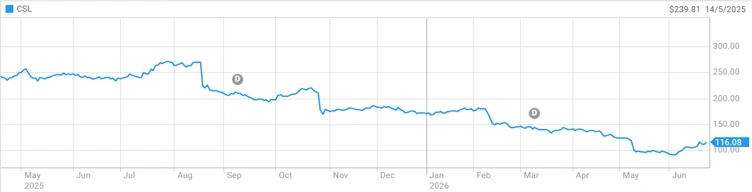

Search for a CSL share price prediction 2026 Australia and the first thing that turns up is a stock chart that looks like a cliff. CSL Limited (ASX: CSL) traded above $275 a year ago. It now sits around $112, after touching a low of $90 earlier in 2026.

That is not a typo. Australia’s old “never sell CSL” blue chip has lost more than half its value in eighteen months.

A Stock That Has Lost Two Thirds Of Its Peak Value

CSL’s all-time high was near $343 back in 2020. The current price puts the stock roughly two thirds below that peak.

Market cap has dropped to approximately $55.7 billion. The 52-week range stands at $90.00-$269.15, and that pretty much sums up the volatility of movements experienced.

A few numbers worth sitting with:

- Trailing revenue: roughly $15.4 billion

- Price to earnings ratio: around 13.3 times

- Dividend yield: about 2.7%, with $2.92 per share paid out

That PE ratio is the strange part. CSL traded on multiples in the high twenties and thirties for years. A stock priced at 13 times earnings is either deeply unloved or deeply broken.

The CSL stock forecast 2026 ASX analysts are publishing right now is really an argument over which one it is.

CSL share price performance [ASX]

What Triggered The Slide, From Plasma Margins To A CEO Exit

The first real crack appeared on 19 August 2025. CSL dropped its long-standing promise that plasma gross margins would climb back to pre-COVID levels of around 57%.

On the same day, management announced job cuts of up to 15% of staff, roughly 3,000 positions worldwide. Twenty-two plasma collection centres, about 7% of the US footprint, were marked for closure.

CSL also flagged a plan to spin off CSL Seqirus, its flu vaccine arm, as a standalone ASX listing by the end of FY26. That timeline has since slipped.

Seqirus had posted a 9% revenue decline in FY25, and a volatile US flu vaccine market made the original deadline look optimistic.

October’s annual meeting brought another downgrade. NPATA growth guidance for FY26 was cut to 4 to 7%, down from 7 to 10%, with Seqirus revenue now expected to fall in the mid-teens percentage range.

That led to another event – the leadership change. CEO Paul McKenzie left, and Gordon Naylor, who formerly served as the Seqirus president, became the new interim CEO in February 2026.

Naylor spent his first 90 days doing a full review. The result of all this was rather rough.

The FY26 revenue guidance was cut to approximately $15.2 billion, with CSL expecting about $5 billion of impairments for both FY26 and FY27 periods, mainly relating to CSL Vifor.

Most of that Vifor writedown traces back to VENOFER, the iron deficiency therapy, after generic competition hit its China sales harder than modelled.

CSL paid US$11.7 billion for Vifor in 2022. A chunk of that price tag is now being written off the books.

CSL Stock Forecast 2026 Splits Wall Street And Bridge Street

Here is where the picture gets genuinely interesting, because the brokers do not agree.

Table: CSL Broker Price Targets vs Current Share Price (as at June 2026)

| Source | Rating | Price Target | Date Issued | Upside/Downside vs $112 |

|---|---|---|---|---|

| Macquarie | Neutral | $188 | December 2025 | +68% |

| Jefferies | Buy | $237 | December 2025 | +112% |

| Canaccord | Buy | $225 (revised from $230) | November 2025 | +101% |

| Simply Wall St (Analyst Consensus) | Buy | $137.97 | June 2026 | +23% |

| Simply Wall St (DCF Fair Value Model) | — | ~$199–$211 | June 2026 | +78% to +88% |

Macquarie cut its price target to $188 from $275 in December 2025, citing weaker plasma economics and a longer path to margin recovery.

Jefferies, looking at the same data, kept a buy rating with a $237 target, arguing the China albumin hit looks temporary.

Simply Wall St’s valuation models have bounced between $140 and roughly $210 depending on which quarter’s guidance gets plugged in.

One recent screen put the consensus broker target at $137.97, which is still a meaningful gap above the current $112 price.

A pattern worth flagging here, because it matters more than any single number. Every time CSL cuts guidance, fair value estimates fall too, but they keep landing well above where the stock actually trades.

That gap is either the market overreacting, or analysts underestimating how long Vifor and Seqirus stay a drag.

There is a genuine bull case sitting underneath the headlines.

The CSL Behring, the major plasma segment, showed revenue growth of about 6% during the period of turmoil.

HEMGENIX, the gene therapy for hemophilia B, presented five-year durability results in the New England Journal of Medicine in December 2025, where 94% of treated patients did not require further therapy.

Privigen received European approval for the use against measles infection.

Privigen picked up European approval for measles prophylaxis. None of that made headlines the way the job cuts did.

For investors weighing CSL against other best Australian shares to buy in 2026, the comparison usually comes down to patience versus certainty. CSL offers scale and a near-monopoly style plasma network. It does not currently offer predictability.

Income investors scanning ASX dividend shares for passive income should also note the payout ratio sits above 100% of earnings, though it remains covered by cash flow for now. That is a yield worth watching rather than relying on.

The August Date That Could Settle The Argument

CSL reports full-year FY26 results on 18 August 2026. That date matters more than any broker note published between now and then.

Simply Wall St’s most recent CSL coverage put it bluntly, recommending investors defer any new position until that result lands.

The logic is simple. Everything about the bull case rests on one question: is Behring’s margin pressure temporary, or has the business permanently re-rated to a lower growth profile?

That question gets answered with real numbers in August, not forecasts. A $750 million buyback running through to 30 June 2026 has been chewing through shares in the meantime, which props up the price without fixing the underlying earnings story.

The honest answer to whether CSL is a strong buy for 2026 sits somewhere between the bulls and the bears.

The stock is cheap against its own history and against consensus targets. It is also cheap because the business broke several of its own promises in under a year, and a 13% rebound off the lows does not undo that trust gap.

Anyone tracking the weekly ASX market prediction already knows healthcare has been a rotation casualty in 2026, with capital favouring defensive and resources names instead. CSL needs to prove Behring’s recovery is real before that rotation reverses in its favour.

Also Read: WiseTech Shares Sink as Richard White Faces AFP Probe

FAQs

Q: Is CSL a buy in 2026?

A: Opinions are split. Brokers see upside to consensus targets, but the FY26 result on 18 August is the real test.

Q: What is CSL’s 2026 price target?

A: Broker targets range roughly from $138 to $237, depending on the firm and date.

Q: Why has CSL stock fallen so much?

A: A plasma margin guidance reversal, 15% job cuts, a delayed Seqirus demerger, and a CEO exit all hit within twelve months.

Q: Does CSL still pay a dividend?

A: Yes. The trailing yield sits around 2.7%, though the payout ratio is above 100% of reported earnings.

Disclaimer:

This article is general information only and does not constitute financial advice. Share prices and figures referenced are accurate as at the time of writing and are subject to change. Investors should conduct independent research and consult a licensed financial adviser before making investment decisions.

Sources:

https://investors.csl.com/investors/asx-announcements

https://www.asx.com.au/markets/company/CSL

Elizabeth Jones is a finance and mining content specialist with over 10 years of experience creating clear, SEO-driven content across fintech, investing, banking, insurance, cryptocurrency, and resource markets. She transforms complex financial data and industry trends into engaging, reader-focused articles that improve understanding and audience engagement.