Treasury Wine Estates Ltd (ASX: TWE) has come under renewed investor focus after a steep decline erased roughly half its market value over the past year. The sharp pullback has been driven largely by weaker demand in key international markets, particularly China, raising questions about near-term earnings visibility. Yet, despite the downturn, analysts and market watchers are assessing whether the selloff has created a potential entry point for long-term investors seeking exposure to a global premium wine business.

TWE Share Price Decline: How Far Has the ASX Wine Stock Fallen?

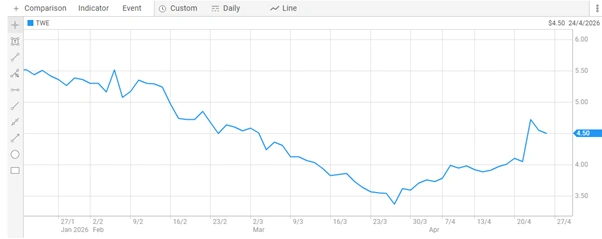

Treasury Wine Estates Ltd (ASX: TWE) shares have experienced a steep fall over the past year. The stock currently trades at AU$4.50, down roughly 51% from its 52-week high of AU$9.18. That places it among the worst-performing large-cap stocks on the ASX over the same period.

Treasury Wine Estates Ltd Share Price [ASX]

Data shows the share price has dropped 43% below its 200-day moving average. Over the past year, TWE underperformed the broader ASX All Ordinaries Index by more than 65%. That is a significant gap, even by the standards of cyclical consumer stocks.

The decline has drawn attention from investors looking for beaten-down opportunities. A 50% price fall does not always mean a broken business. For TWE, the question is whether the selloff has gone too far.

What Triggered the TWE Stock Selloff? Penfolds China Sales Disappoint

The central trigger for the selloff was a profit warning tied to weak Penfolds sales in China. In late 2025, TWE pulled its full-year earnings guidance for fiscal 2026. Alongside that, the company paused a AU$200 million share buyback program.

China had been a key growth market for Penfolds, TWE’s premium wine division. Beijing lifted its tariffs on Australian wine in March 2024, reopening a valuable export channel. However, consumer spending in China has remained uneven, which has weighed on Penfolds volumes.

Morningstar analysts cut their fair value estimate for TWE by 26% in December 2025. Yet Morningstar also noted that the market reaction appeared to overshoot the fundamental impact. That assessment suggests the stock may have priced in a more severe outcome than the data supports.

Treasury Wine Estates Business Overview: Premium Brands Drive Revenue

TWE operates as one of the world’s top five wine producers by volume. The company owns more than 70 brands across multiple price segments and geographies. Its portfolio includes Penfolds, DAOU Vineyards, 19 Crimes, Wolf Blass, Wynns, Lindeman’s, and Beringer.

Treasury Wine Estates owns more than 70 brands globally, including Wolf Blass and 19 Crimes, spanning entry-level to premium price points. (Image: Wbmonline)

In fiscal year 2025, TWE reported revenue of AU$2.99 billion, up 6.47% from the prior year. Earnings reached AU$436.9 million, reflecting a 341.76% increase on the previous period. Much of that earnings growth came from the integration of DAOU Vineyards, acquired for up to US$1 billion.

TWE sells wine to distributors, wholesalers, retail chains, and directly to consumers. The company also provides contract bottling services and holds vineyard assets across key wine regions. That diversified asset base gives it multiple levers to manage margins across different market conditions.

ASX Dividend Stock Profile: TWE Dividend History and Current Yield

TWE has paid dividends every year since its ASX listing in May 2011. The company typically distributes dividends twice a year, in April and October. It also offers shareholders a dividend reinvestment plan (DRP) to reinvest payouts into new shares.

However, the dividend yield has compressed alongside the earnings decline. Stockopedia data shows a trailing dividend yield of 1.15%, based on total dividends of AU$0.04 over the past twelve months. That is well below the yields investors associated with TWE during stronger earnings periods.

The low yield reflects a period of capital preservation rather than distribution. If earnings recover toward analyst forecasts, dividends could increase substantially. For income-focused investors, the yield today may not reflect the income potential over a two- to three-year horizon.

Analyst Consensus on TWE: Target Price and Broker Recommendations

Broker coverage on TWE remains active, with 23 analysts tracking the stock according to Simply Wall St. The analyst consensus recommendation sits at Hold, reflecting uncertainty about the near-term recovery timeline. However, the consensus price target tells a different story.

Stockopedia reports a consensus analyst price target of AU$5.40 for TWE. That represents approximately 48% upside from the last closing price of AU$3.64. A gap of that size between the current price and analyst targets is not common among large-cap ASX stocks.

Morningstar describes the stock as trading at a meaningful discount to its assessed intrinsic value. The consensus EPS forecast for the next financial year sits at AU$0.32. That implies a price-to-earnings ratio well below TWE’s historical average if the share price remains near current levels.

China Reentry and Premium Wine Trends: Key Growth Catalysts for TWE

Analysts at Simply Wall St identify TWE’s China market recovery as a primary growth catalyst. Penfolds holds strong brand recognition among Chinese consumers of premium wine. A sustained improvement in Chinese consumer confidence could drive meaningful volume recovery for the division.

Beyond China, TWE benefits from a broader global shift toward premium wine categories. The premiumisation trend means consumers in key markets tend to trade up to higher-margin products. TWE’s portfolio, anchored by Penfolds and DAOU, sits directly in this higher-margin segment.

DAOU Vineyards in California’s Paso Robles region adds a premium US asset to TWE’s global portfolio following its acquisition for up to US$1 billion. (Image: DAOU Vineyards)

The company has also introduced a new divisional operating model to improve efficiency. TWE CEO Tim Ford presented the restructured model to investors and analysts in June 2025. Management framed the reorganisation as a step toward stronger margin performance and more focused capital deployment.

Risks Facing Treasury Wine Estates: What Investors Should Monitor

Despite the potential recovery case, several risks remain relevant for TWE investors. Simply Wall St notes that shifting consumer preferences pose a structural challenge to the wine category. Younger consumer cohorts in key markets show lower engagement with traditional wine brands compared to prior generations.

Climate change also presents an operational risk for vineyard-dependent businesses. Extreme weather events and changing growing conditions can affect grape quality and yields. TWE’s cost base and product quality could face pressure if these trends accelerate.

Regulatory risk remains elevated given TWE’s reliance on the China market. Trade policy between Australia and China has shifted more than once over the past decade. Any deterioration in diplomatic or trade relations could quickly affect the Penfolds sales pipeline.

Stock Price Stability and Volatility: What the Data Shows for ASX: TWE

Despite the sharp annual decline, TWE’s share price volatility has stabilised in recent months. Simply Wall St reports that the stock has not shown significant price swings in the past three months. Weekly volatility of around 6% has remained consistent over the past year.

That pattern of stabilisation can indicate that selling pressure has eased. It may also reflect a base of investors who bought the stock at lower prices and hold it with conviction. Reduced volatility after a sharp drawdown is often a precursor to a more sustained directional move.

Is TWE a Dividend Stock Worth Buying at Current ASX Prices?

Treasury Wine Estates presents a case study in a quality business facing a cyclical headwind. The Penfolds brand carries genuine pricing power and global recognition. The DAOU acquisition adds a growing premium US wine asset to offset geographic concentration risk.

The current share price reflects significant pessimism around China volumes and near-term earnings. Yet the 48% gap between the current price and the analyst consensus target suggests the market may have overcorrected. Morningstar’s own analysis points to the same conclusion.

Income investors will note that the current dividend yield of 1.15% is not compelling in isolation. However, the long-term dividend track record and the potential for earnings recovery change the calculation. Investors willing to accept near-term uncertainty in exchange for a discounted entry point may find TWE worth examining. As always, investors should conduct their own research and consider their personal financial circumstances before making any investment decision.

Also Read: Auric Mining Names Gareth Solly CEO and Director

FAQS

Q1: Why has the Treasury Wine Estates Ltd (ASX: TWE) share price fallen sharply?

A1: The drop is mainly due to weaker sales of its premium Penfolds wines in China, which led the company to withdraw earnings guidance and pause its share buyback, reducing investor confidence.

Q2: Is Treasury Wine Estates Ltd still a dividend-paying stock?

A2: Yes, TWE has maintained dividend payments since 2011. However, the current yield is low due to weaker earnings and a focus on conserving capital.

Q3: What is the current analyst outlook for TWE shares?

A3: Analysts generally rate TWE as a “Hold,” but consensus price targets indicate potential upside of around 40–50% from current levels.

Q4: What are the key growth drivers for TWE?

A4: A recovery in China’s demand for Penfolds, expansion of DAOU Vineyards, and the global shift toward premium wine consumption are key growth drivers.

Q5: What risks should investors consider with TWE?

A5: Risks include weak consumer demand in China, shifting preferences among younger consumers, climate impacts on vineyards, and potential trade or regulatory disruptions.

Q6: Is TWE considered undervalued right now?

A6: Some analysts, including Morningstar Inc., believe TWE may be undervalued, though uncertainty around earnings recovery remains.

Disclaimer

This article is published by Colitco for informational purposes only and does not constitute financial, investment, or professional advice. The content is based on publicly available information and sources believed to be reliable at the time of writing. However, Colitco makes no representations or warranties regarding the accuracy, completeness, or timeliness of the information. Readers should conduct their own independent research and consult a licensed financial advisor before making any investment decisions. Colitco and its affiliates shall not be held liable for any loss or damage arising directly or indirectly from the use of, or reliance on, the information provided in this article.

Sources

https://www.stockopedia.com/share-prices/treasury-wine-estates-ASX:TWE/

https://www.fool.com.au/tickers/asx-twe/

https://finance.yahoo.com/quote/TWE.AX/

https://www.morningstar.com.au/investments/security/ASX/TWE

https://www.asx.com.au/markets/company/TWE

Last modified: April 27, 2026