The SKS Technologies data centre contract announced on 14 July 2026 is worth $28 million. That number is the least interesting thing about it.

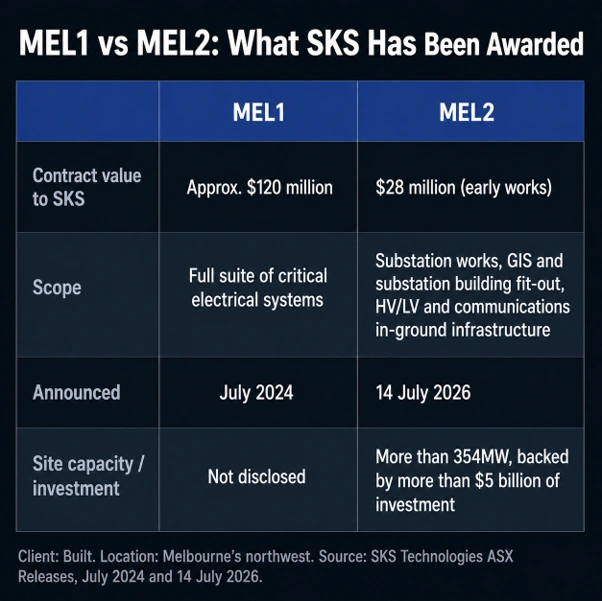

Here is what matters. SKS Technologies Group Limited (ASX: SKS) is doing the early works for Built on a site called MEL2. The same company did roughly $120 million of work on MEL1, including the full suite of critical electrical systems, first flagged back in July 2024. Built came back. That is the whole story in one line.

Early works is the plumbing before the plumbing. Conduits. Underground pits. High-voltage cabling running into the gas insulated switchgear. Internal fit-out of the switchgear and substation buildings. It is the stuff that has to be right before anyone pours a slab, and it is almost never the last cheque a builder writes to the contractor doing it.

Why $28 million is the wrong number to focus on

The MEL2 site is planned for more than 354MW of capacity. Total investment is pegged at more than $5 billion.

So SKS has been handed $28 million of a $5 billion job. That is about half a percent.

Now think about MEL1. SKS did $120 million there. If MEL2 follows the same shape, and the client is the same builder, and the early works are already in SKS’s hands, then the $28 million looks less like a contract and more like a deposit.

Nothing in the announcement promises that. Management did not claim it either, which is to their credit. But a contractor does not lay the underground infrastructure for a hyperscale campus and then hand the switchboards to someone else. Not usually.

MEL1 versus MEL2 scope as disclosed by SKS Technologies.

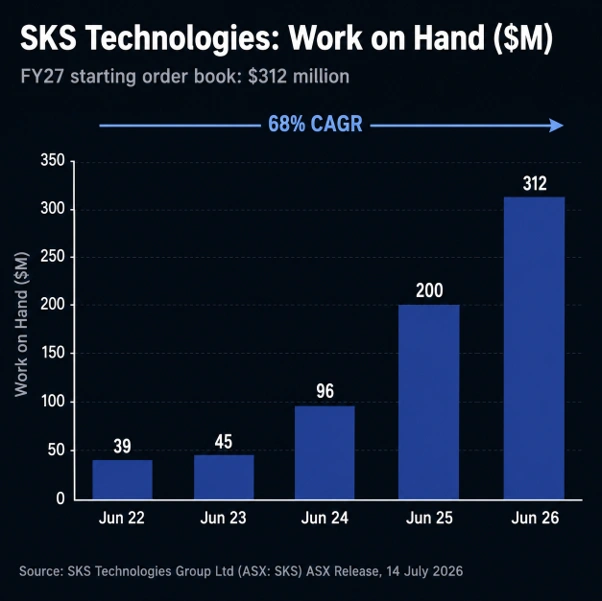

The order book chart is doing all the talking

Buried in the release is a small bar chart. Work on hand, financial year by financial year.

- June 2022: $39 million

- June 2023: $45 million

- June 2024: $96 million

- June 2025: $200 million

- June 2026: $312 million

That is 68% compound growth, and a seven-fold jump since June 2023.

Do the arithmetic that the release does not do for readers. SKS guided to about $340 million of FY26 revenue after a guidance upgrade in February 2026. It is now starting FY27 with $312 million already on the books.

Roughly 92% of a full year’s revenue, booked before the year begins. Most contractors would take that and go home.

SKS Technologies work on hand has grown from $39 million in June 2022 to $312 million in June 2026.

The tender pipeline has one very obvious hole in it

Since February 2026, the pipeline of work under tender has climbed from $572.26 million to $1,254.02 million. Almost 120% in five months.

Data centre tenders make up just over $1 billion of that. In February the figure was $423.56 million.

Read that again. Better than four-fifths of what SKS is currently bidding on is a data centre.

That is not a diversified engineering firm. That is a data centre business with an audio-visual arm attached. Chief Executive Matthew Jinks said the company is “now an established provider to the data centre market in Australia”, pointing to a forecast pipeline of 44 Sydney projects at 11.4GW and 30 Melbourne projects at 9GW.

He is right. That is also the risk.

Australian data centre capacity is forecast to expand 128.6%, from 1.4GW in 2025 to 3.2GW by 2030. Every one of those halls needs high-voltage infrastructure and someone competent to install it. Very few Australian contractors have done it at hyperscale and lived to tender again.

But a bet this concentrated cuts both ways. If hyperscaler capital expenditure slows, or if a single build gets deferred, SKS does not have a mining division or a health portfolio big enough to absorb the hit. The company does serve defence, mining, health and retail. Those sectors are no longer where the money is.

What a shareholder should actually watch from here

Not the $28 million. Watch for the follow-on MEL2 package.

Watch whether the FY27 order book keeps converting at the margins management promised. The February 2026 upgrade lifted forecast profit before tax to $34 million on a 10% margin. Growing revenue is easy when the sector is on fire. Holding a 10% margin while doing it, on jobs this technically nasty, is the hard part.

Watch the balance sheet too. Bank guarantee facilities were expanded in May 2026 for a reason. Contractors do not fail because work dries up. They fail because they run out of working capital in the middle of a boom.

The share price already reflects a lot of optimism. SKS was trading near record levels in May 2026 after a run of more than 300% across twelve months. Investors have priced in flawless execution. There is not much room left for a bad quarter.

Readers tracking this theme can compare the SKS $28 million data centre win against the capacity story at NEXTDC’s $1.5 billion capital raise, which lays out where the megawatts are actually going. The power problem behind all of it is covered in our look at Microsoft and Chevron’s Texas gas plant. For the wider sector picture, see our ranking of Australia’s largest listed technology companies and our view on ASX growth names built for the long haul.

Project works on MEL2 start immediately. The next number to arrive will tell everyone whether $28 million was a contract or a handshake.

Also Read: Australia Interest Rate Forecast 2026: The RBA’s Long Game

FAQs

Q: What is the SKS $28 million data centre contract for?

A: Early works on the MEL2 hyperscale data centre in Melbourne’s northwest, awarded by Built.

Q: Who is the client?

A: Built, the construction company delivering the MEL2 facility.

Q: How big is the MEL2 site?

A: More than 354MW of planned capacity, backed by more than $5 billion of investment.

Q: What is SKS Technologies’ order book now?

A: $312 million as at June 2026, a seven-fold increase since June 2023.

Q: Did SKS work on MEL1?

A: Yes. It completed about $120 million of works there, including the full critical electrical systems.

Q: When does work start?

A: Immediately, per the 14 July 2026 ASX release.

Disclaimer:

This article is general information only and does not constitute financial product advice. It does not take into account any individual’s objectives, financial situation or needs. Investing in listed securities carries risk, including loss of capital. Readers should seek advice from a licensed financial adviser and refer to the original ASX announcements before making any investment decision. Colitco accepts no responsibility for any loss arising from reliance on this content.

Source:

https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-03110778-3A697106

Elizabeth Jones is a finance and mining content specialist with over 10 years of experience creating clear, SEO-driven content across fintech, investing, banking, insurance, cryptocurrency, and resource markets. She transforms complex financial data and industry trends into engaging, reader-focused articles that improve understanding and audience engagement.