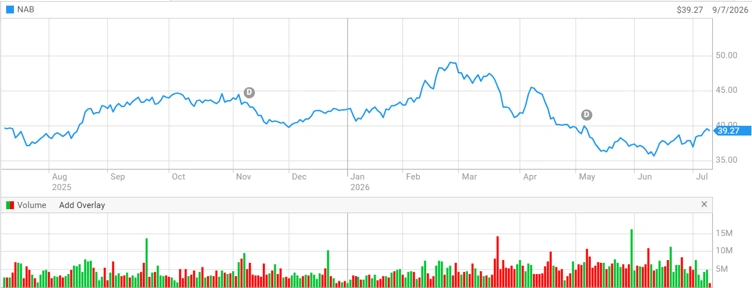

Anyone following the NAB outlook 2026 knows what a rollercoaster it has been. The stock of National Australia Bank Ltd (ASX: NAB) reached an all-time peak of $49.45 on 27 February.

By early June, it was down around 27% to an annual trough of around $35.86. As of 7 July it was trading around $38.83, about 9% off that low but still down roughly 8% for the year.

That round trip is the whole story. The market fell hard for the big banks, then got cold feet.

Here is the bit most people skip past. The script for 2026 was meant to be rate cuts. Cheaper money, happier borrowers, fatter bank margins. That script got torn up.

Meanwhile, the Reserve Bank took the opposite stance. It increased the cash rate to 4.10%, the second increase this year, as a reaction to inflation caused by high fuel costs and instability in the Middle East. Higher interest rates hurt people.

Squeezed households miss repayments. That shadow hangs over every bank stock right now. Any NAB stock prediction for 2026 has to start there, not with the balance sheet.

What NAB’s own numbers actually said

NAB handed down its half-year results on 4 May. On paper they looked grim. Statutory profit fell 18% to $2,750 million.

Dig one layer down and the mood shifts. That drop came almost entirely from a $949 million charge tied to how NAB books its software costs. Strip it out and cash earnings landed at $3,588 million, up 2.3% on the prior half, with underlying profit up 6.4%.

The dividend stayed put at 85 cents, fully franked. Held steady, not trimmed. Boards don’t hold a payout flat when they’re worried about the cash behind it.

One number said more than the rest. NAB lifted its forward-looking provisions by $300 million, with an overlay for sectors hit by fuel shortages. That is money parked aside for loans that might sour. Banks don’t stockpile for a rainy day when they reckon the sun is out.

NAB shares round-tripped from a February record to a June low before steadying in July 2026. [ASX]

Business banking is the reason to own NAB and the reason to fret

Every big four bank has a personality. NAB’s is business lending. It is the biggest business lender in the country, holding about 22% of the market and roughly 28% of the SME segment, banking around one in four small and medium firms.

That division did the heavy lifting. Business and Private Banking cash earnings jumped 9.9% on the prior half, and Australian business lending rose 5.6%.

The catch is plain once it’s said out loud. Small businesses are exactly the customers who wobble first when rates climb and fuel bills bite. NAB’s biggest strength doubles as its biggest exposure.

The NAB share price forecast for Australia in 2026 splits the experts

This is where it gets messy. The analysts are all over the shop.

| View | The Read |

|---|---|

| Market Index | Most on hold, average target near $39.17, barely above today. |

| TradingView | Eight holds, five sells, average target $37.78, a slight downgrade. |

| Goldman Sachs | Started coverage with a sell. |

| UBS | Buy, target as high as $48.50. |

The bears have names. Michael Gable at Fairmont Equities put a sell on NAB, pointing at margin pressure and business banking credit risk into FY27. Mark Gardner at MPC Markets is bearish on near-term earnings. Dylan Evans at Catapult Wealth flagged Federal Budget changes and stretched households.

The bulls have not left the building. UBS runs the cheeky-value case: NAB trades near 16 times forecast earnings while Commonwealth Bank sits near 26 times. On that maths NAB looks like the cheaper cousin.

One quiet move spoke louder than any broker note. AFIC, one of Australia’s oldest listed investment companies, trimmed its NAB position earlier this year and rotated into retail and tech names. When patient money like that steps back, it pays to notice.

What it comes down to for NAB in 2026

Strip away the noise and NAB is a solid bank wearing a full price tag in a jittery market.

The dividend is the anchor. Consensus tips $1.70 per share for FY26, a yield near 4.3%, or closer to 6.4% once franking credits are counted. For income hunters, that is the pitch.

The risk is timing. Pay a rich price for a decent bank just as rates lift and bad debts creep up, and the yield can get swallowed whole by a falling share price. That is the trap the sell ratings keep circling.

Management itself is guiding for low to mid single-digit cash earnings growth in FY26. Steady, not thrilling.

The honest take: NAB is neither a screaming bargain nor a wreck. It reads as a hold that pays income while the wait plays out, with the next real move likely hinging on where the RBA and fuel prices land through the second half.

That verdict is analysis, not a nudge to trade. The buy case rests on cheap-versus-CBA and yield; the sell case rests on rising rates chewing into the exact customers NAB leans on.

For a wider look at where the sector sits, we have broken down how analysts are splitting on the big four banks and what is driving the CBA share rally and what could derail it. The move by AFIC to rotate out of major banks is worth reading alongside this. Income-focused readers may also want our guide to building a dividend-led retirement portfolio.

FAQs

Q: What is the NAB dividend yield in 2026?

A: Approximately 4.3%, according to the consensus estimates, or roughly 6.4% franked.

Q: Why has the NAB share price fallen in 2026?

A: It has risen to a record in February but fell around 27% in June on concerns about banks’ overvaluation due to rising rates.

Q: What is the NAB share price outlook for Australia in 2026?

A: Analyst targets span a wide range, starting from around $29 at the low end up to roughly $48.50 at the high end.

Q: Is NAB cheaper than CBA?

A: Yes. The stock is trading at approximately 16 times forward earnings, whereas that of CBA stands at around 26 times.

Disclaimer:

This article is general information only and does not constitute financial or investment advice. It reflects analysis of publicly available data and analyst commentary as at 9 July 2026, not a recommendation to buy, hold or sell any security. Share prices, forecasts and ratings change quickly. Investors should verify all figures independently and consult a licensed financial adviser before making any investment decision. Colitco accepts no responsibility for any loss arising from reliance on this content.

Source:

https://www.asx.com.au/markets/company/NAB

Luke Carlino is a seasoned Copywriter, Content Strategist, and Social Media Manager specialising in Mining, Finance, and Business journalism. With more than a decade of industry experience, he brings rigorous editorial standards and commercial acuity to every project.