Shares Lift After Long-Awaited IPO

Virgin Australia shares surged over 8 per cent to $3.15 on Tuesday after its ASX return. The listing follows a $439 million IPO at $2.90 per share. The float marks one of the most anticipated listings of 2025. Trading under the code VGN, Virgin’s listing caps five years since entering administration in April 2020.

Figure 1: Virgin Australia makes ASX return with a bang

Bain Capital, Qatar Airways Retain Stakes

Bain Capital’s holding dropped to 40 per cent post-IPO. Qatar Airways retained about 23 per cent. Public investors now hold 30 per cent. Management and other stakeholders comprise the remaining 7 per cent.

COVID Collapse To Recovery

Virgin collapsed during the COVID-19 pandemic in 2020. With no federal bailout, the airline entered administration. Bain Capital acquired the business for $3.5 billion. The airline delisted shortly after. Virgin grounded its budget brand Tiger Airways and refocused on mid-market services. It returned to profitability in 2023, reporting a $129 million statutory profit.

Mid-Market Strategy and Leaner Model

Virgin Australia targets business and leisure flyers with a mid-market offering. Analyst Peter Harbison said, “It’s a leaner airline than it was, say, six or seven years ago.” Lounges and inclusions are fewer than Qantas, but broader than Jetstar. “Its product is really very much tailored to the mid-market, which does suggest quite a lot,” Harbison added.

Qatar Airways Boosts Global Reach

Qatar Airways invested 25 per cent in Virgin earlier this year. The airline now offers 28 weekly services to Doha. These operate under a wet-lease pact, enabling global expansion without capital expenditure.

Figure 2: Virgin Australia staff gathered for the company’s listing, including chief executive Dave Emerson

IPO Structure and Key Details

Virgin issued 236.2 million shares, representing 30.2 per cent of capital. The IPO raised $685 million, all going to existing holders. The listing implies a $2.3 billion market capitalisation. Deferred settlement will run until 27 June.

Virgin’s Financial Rebuild

Virgin forecasts $330 million underlying net profit after tax (NPAT) for FY25. FY23 marked its first statutory profit in a decade. The fleet now consists solely of Boeing 737-800 and MAX 8 aircraft. Simplified maintenance and training have cut costs. Virgin controls 31.2 per cent of the domestic market as of June 2025, up from 21 per cent pre-COVID.

Golden Triangle Drives Revenue

Routes between Sydney, Melbourne, and Brisbane account for 45 per cent of revenue. These core routes form the airline’s financial base. The Velocity loyalty program now has 13 million members and 80 commercial partners.

Four Structural Tailwinds Identified

Virgin management outlined four key advantages over rivals. These include a cleaner balance sheet with net leverage below 1× EBITDA. The domestic duopoly strengthens pricing amid the exit of Rex and Bonza. Qatar’s partnership offers international scale without aircraft on Virgin’s books. Virgin’s IPO valuation is lower at 7× forecast FY25 earnings versus Qantas at 10×.

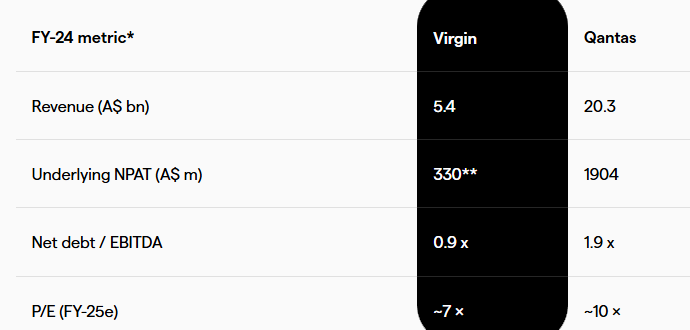

Valuation Highlights Scale Gap With Qantas

Qantas remains Australia’s largest airline, with FY24 revenue of $20.3 billion. Virgin posted $5.4 billion, showing the gap in size. Qantas reported $1.9 billion NPAT in FY24. Virgin’s $330 million forecast highlights margin differences despite recovery. Virgin’s net debt-to-EBITDA ratio is 0.9×, better than Qantas at 1.9×. This gives Virgin more financial flexibility during shocks.

Figure 3: Virgin vs Qantas

Caution Urged Despite Discount Valuation

Some brokers value Virgin shares at $2.40–$2.60. Five key risks were cited. The FY24 profit includes a one-off $278 million windfall from cancelled credits. IPO proceeds go to Bain Capital, not Virgin itself. Growth must be funded from cash flow. Virgin’s mid-market position may be pressured by mispricing from Jetstar or Qantas. Net debt of $1.31 billion equals $0.54 per share in enterprise value.

Also Read: ASX 200 Set to Climb as Wall Street Rallies and Middle East Tensions Ease

Airlines Remain Exposed To Shocks

Airlines remain vulnerable to fuel prices, wages, and macroeconomic shocks. Virgin’s previous stint on the ASX saw a 90 per cent fall from peak to trough. Analysts advise caution given the cyclical nature of the sector.

IPO Offers Promise With Realistic Constraints

Virgin’s new business model features lower cost structures, simplified operations and loyalty-driven revenue. However, none of the IPO funds will support expansion or innovation. Long-term gains depend on Virgin’s ability to grow profit without one-off boosts.

Investors Face Mixed Signals

Virgin Australia offers a leaner, restructured version of its past operations. It holds a 31 per cent domestic share and enjoys global reach via Qatar. Yet, competition, thin margins and cyclicality temper enthusiasm. Investors must weigh potential against structural risk. Post-listing performance will depend on sustained profitability and market confidence.