In its Qube Holdings half-year results for FY 26, Qube Holdings Limited recorded a good momentum due to higher volumes and focused implementation in its logistics and ports.

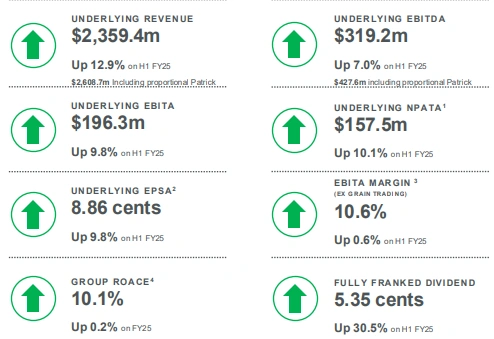

Underlying revenue increased to $2,359.4m, which rose by 12.9% on H1 FY25, with underlying EBITDA also rising by 7.0% to 319.2m. Underlying EBITA rose by 9.8 to $196.3m and underlying NPATA rose by 10.1 to $157.5m. Bertha EPSA increased to 8.86 cents, 9.8 per cent.

The performance was attributed to organic growth and recent acquisitions by the management. Sector headwinds and weather upheavals in certain areas were also offset through diversifying the portfolio.

Qube has a national logistics and port network that helps to sustain growth in earnings. [Qube Holdings]

Strong Revenue And Margin Expansion Across Divisions

Logistics and Infrastructure contributed the most revenue and were associated with the Infrastructure, as it gained 24.4 with revenue of $1,360.3m and EBITA of 158.9m, respectively. Expansion was in grain dealing, rail, and a full period in Webb Dock West.

Ports and Bulk revenue was 0.3% increased to reach $998.9m but the EBITA dropped 5.2% because of timing of the contracts and project postponement. In Group EBITA margins without grain trading, margins went up 0.6 to 10.6.

Return on capital improved, with ROACE of 10.1, and 10.1 and 0.2 on FY25. The mix depicts that Qube Holdings’ profit and revenue strength remain, with bulk volumes turning soft.

How Did Patrick And Associates Contribute?

Qube Holdings again supported earnings on the basis of higher volumes and increased productivity due to Patrick Stevedoring’s business.

Patrick’s revenue has increased by 6.2 per cent to reach $498.5m, whilst EBITA has increased by 12.1 per cent to reach $178.6m. Qube increased its NPAT share to $44.0m, 18.7%. The cash payments to Qube went up by 29.2% to $77.5m.

The market share stood at close to 41% with contract renewals and efficiency of operations. The associate will still be at the core of stable cash flow and flexibility of funding throughout the group.

Patrick terminals were capable of compensating for increased container volumes more efficiently. [Qube Holdings]

Dividend Lift And Balance Sheet Strength Confirm Confidence

The board announced a fully franked interim dividend of 5.35 cents per share, which is 30.5 per cent higher than H1 FY25 and which is a 60 per cent payout ratio.

Good operating cash flow and asset sale turned into a cut of net borrowings to $1,567.1m. The gearing was 31.6 which is almost within the 30%-40% range of target.

Qube also sold approximately 152 million assets in the half, which comprised excess property and rolling stock. Such steps financed capex growth and retained financial strength.

What Does The Scheme Offer Mean For Shareholders?

One of the significant changes that came with the Qube Holdings half-year results was the development. The company concluded a Scheme Implementation Deed with a group headed by Macquarie Asset Management.

According to the proposal, other shareholders other than UniSuper would get cash per share of the amount of 5.20, less the amount of dividends paid. The scheme is still open to approvals and a shareholder vote that is likely to take place circa June 2026.

The offer was now unanimously recommended by the board, awaiting independent expert review. Shareholders are now considering operational expansion as well as the certainty of takeovers.

The business strategy alters when Qube considers a consortium acquisition bid. [The Exchange Asia]

FY26 Outlook Signals Continued Earnings Momentum

The management anticipates good growth in EBITA in Logistics and Infrastructure, and a general flat in Ports and Bulk earnings. Associates are also predicted to contribute approximately a 20m NPATA growth as compared to FY25.

Net interest will be more by $1015m than FY25, and gross capex is at 400450m. Net capex is forecast at $250–$300m.

According to the present circumstances, Qube is aiming at a growth of between 6.0%-10.0% in NPATA and EPSA in FY26. The prognosis favours further growth in Qube Holdings profit and revenue and discipline on returns.

Also Read: QUB ASX Announcement: Macquarie Maintains Exclusivity in Qube Review

FAQs

Q1: What were Qube Holdings half year results, revenue figures?

A1: Underlying revenue totalled $2,359.4m, up 12.9% on H1 FY25.

Q2: How much did Qube Holdings earnings grow?

A2: Underlying NPATA rose 10.1% to $157.5m, while EPSA reached 8.86 cents.

Q3: What dividend did shareholders receive?

A3: A fully franked interim dividend of 5.35 cents per share, up 30.5%.

Q4: What is the FY26 earnings outlook?

A4: Management expects 6.0%-10.0% growth in NPATA and EPSA for the year.