Latitude Group Holdings (ASX: LFS) wrapped up a landmark financial year in 2025, posting a 59% surge in cash net profit after tax (NPAT) and crossing $7.2 billion in gross receivables. The Latitude annual report 2025 highlights a business that has quietly reinvented itself — yet its share price tells a more cautious story.

What the Numbers Actually Say

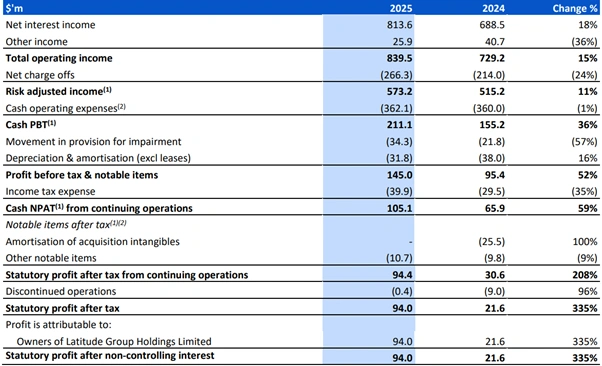

The headline figures from Latitude’s full-year results are hard to ignore.

The company reported:

- Cash NPAT of $105.1 million, up 59% year-on-year

- Statutory NPAT (continuing operations) of $94.4 million, compared to $30.6 million in 2024

- Total new volumes of $9.1 billion, up 10%

- Gross receivables of $7.2 billion, up 7% — the highest in five years

- Operating income of $839 million, up 15%

- Cash cost-to-income ratio of 43.1%, improved by approximately 800 basis points

Net interest margin expanded to 11.75%, up 104 basis points year-on-year. Return on tangible equity reached 22.4%, a 702-basis-point improvement.

CEO Bob Belan called it a year of “disciplined execution,” pointing to volume growth, margin expansion and a sharper focus on core markets, personal loans, credit cards and auto finance across Australia and New Zealand.

Figure 1: Latitude Group FY25 Results [Latitude Group]

The Team Behind the Turnaround

Leadership Steering the Ship

Belan, who took the top job in April 2023, has led Latitude through what the company calls its “Path to Full Potential” strategy. Under his watch, Latitude shed non-core activities and doubled down on its twin Pay and Money divisions.

Chairman Mike Tilley credited the company’s recovery to a focus on “building capability, discipline and focus.” He also welcomed new CFO Guillaume Leger during the year, whose global finance experience has already made an impression across the executive team.

The board added Ilfryn Carstairs as a non-executive director in January 2025 — a Partner at Värde Partners and a key voice on credit and consumer finance matters.

How It Serves Its Customers

Latitude now supports more than 1.8 million customers across Australia and New Zealand. Its business operates through two engines:

- Pay Division — credit cards, interest-free plans and retail partner finance through over 5,500 merchant outlets

- Money Division — personal and auto loans, directly and through a broker network of 5,500+

The Money Division drove receivables growth of 10% to a record $3.3 billion. New personal and auto loan originations reached $1.6 billion for the year. Latitude now ranks as the second-largest personal loan lender in Australia, second only to one of the Big Four banks, and holds the number-one position in New Zealand.

Where Growth Is Coming From

New Partnerships and Adjacent Categories

The Latitude annual report 2025 highlights a push beyond traditional retail finance. During FY25, Latitude added new merchants, including E&S Trading and Adairs Retail Group, renewed major deals with Harvey Norman, and realised the full-year benefit of its David Jones store card partnership.

It also moved into adjacent sectors, signing partnerships with Webjet (travel) and Dental Boutique (health), flagging a clear intent to follow consumer spending into new categories.

In February 2026, Latitude launched an Enterprise Growth Division to lead this expansion, starting with health, wellness and home services.

How the Balance Sheet Got Stronger

Latitude raised $3 billion in new funding during the year. Its institutional debt investor base grew to 62, with 60% based offshore. The Tangible Equity Ratio closed at 7.1%, sitting at the top end of its 6–7% target range. This gave the board enough confidence to declare a total dividend of 9 cents per share for the year, 4 cents unfranked in 1H25, followed by 5 cents fully franked in 2H25.

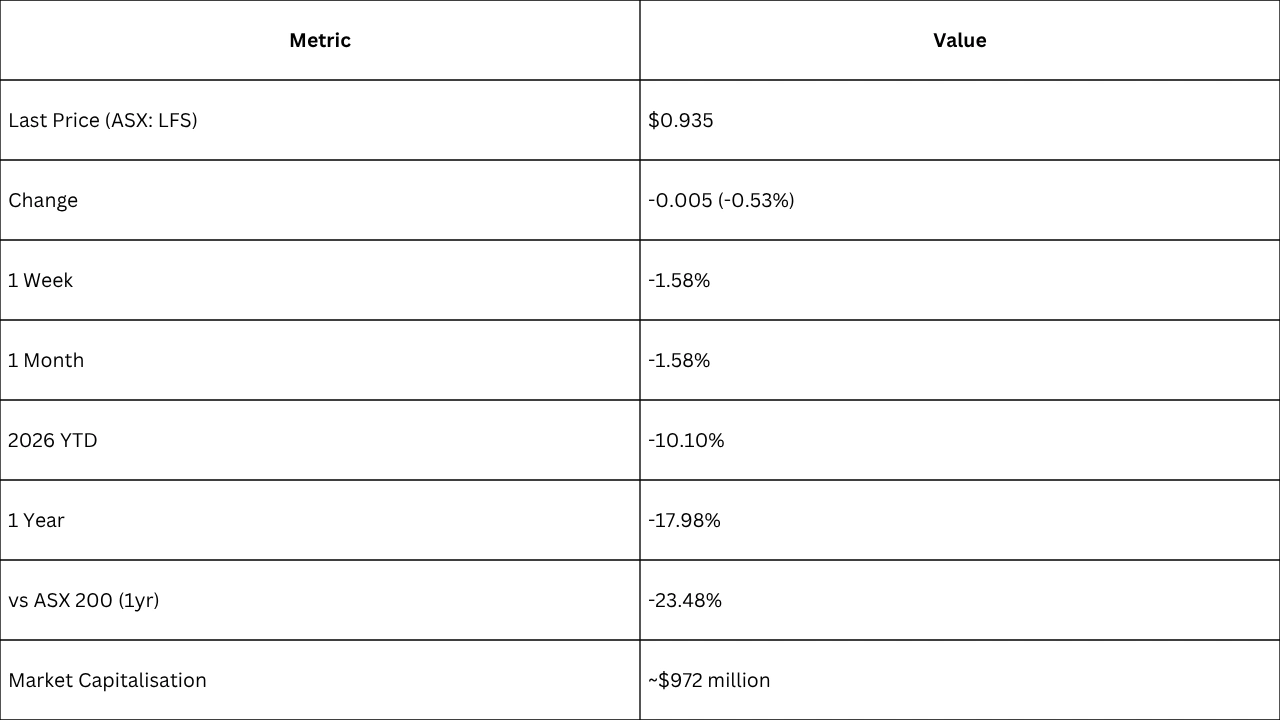

Why Shareholders Aren’t Celebrating (Yet)

Despite the strong Latitude annual report 2025 highlights, the market hasn’t fully rewarded the result.

LFS shares have fallen roughly 18% over the past year and have underperformed the ASX 200 by more than 23 percentage points. Macro headwinds, including household budget pressures, ongoing cost-of-living strain and lingering uncertainty about rate direction, appear to be weighing on sentiment.

The RBA’s household outlook and investor reaction in 2026 remains a key variable for consumer lenders like Latitude. Any deterioration in credit quality or consumer confidence could quickly eat into the earnings momentum Belan’s team has worked hard to build.

For investors reading the share price alongside the operating result, the divergence is worth noting. It raises questions that echo broader debates around ASX share market corrections in 2026 and defensive positioning strategies.

What Comes Next

Latitude’s second strategic phase, which it calls Bridge to the Future, rests on five pillars:

- Extend and embed the fundamentals

- Deliver sustained asset growth

- Eliminate legacy technology

- Enhance productivity and customer experience through AI

- Drive operational and risk management excellence

The company has already begun modernising its credit card platform and deploying AI across servicing and credit operations. Belan flagged that the rate of technology advancement is accelerating, and Latitude intends to move with it, not against it.

For investors watching the fintech and consumer lending space, Latitude’s story sits alongside broader market movements in growth-stage financial services. It’s worth comparing how the sector as a whole is being valued — including what analysts have made of Citigroup and Nebius stock positioning in 2025 and early 2026.

Whether Latitude’s operational momentum eventually closes the gap with its share price remains the central question heading into 2026.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The information presented is based on publicly available sources, including Latitude Group Holdings Limited’s FY25 Annual Report and ASX announcements. Past performance is not a reliable indicator of future results. Share prices and financial data are subject to change. Readers should conduct their own research and consult a licensed financial adviser before making any investment decisions. The author and publisher hold no positions in ASX: LFS at the time of publication.

Frequently Asked Questions

1. What were Latitude Group’s key financial results for FY25?

Ans: Latitude Group delivered a strong FY25 performance, growing its cash NPAT by 59% to $105.1 million and statutory NPAT from continuing operations to $94.4 million — up from just $30.6 million the previous year. Total new volumes hit $9.1 billion, gross receivables climbed to $7.2 billion (a five-year high), and operating income rose 15% to $839 million. The board declared a full-year dividend of 9 cents per share, with the second-half portion fully franked.

2. Why has Latitude’s share price fallen despite strong profit growth?

Ans: Markets tend to price in expectations, not just results. While the Latitude annual report 2025 highlights impressive earnings momentum, the share price has dropped roughly 18% over the past year and underperformed the ASX 200 by more than 23 percentage points. Investors remain cautious about ongoing household budget pressures, cost-of-living stress, and uncertainty around interest rate direction — all of which directly affect consumer lending businesses like Latitude.

3. What is Latitude’s strategy heading into 2026 and beyond?

Ans: Latitude has transitioned into the second phase of its growth strategy, called Bridge to the Future. This builds on its Path to Full Potential program and focuses on five priorities: embedding operational fundamentals, driving sustained asset growth, eliminating legacy technology, deploying AI to improve customer experience, and strengthening risk management. The company also launched a new Enterprise Growth Division in February 2026 to expand into health, wellness and home services — moving beyond its traditional retail finance roots.

Sources

- https://data-api.marketindex.com.au/api/v1/announcements/XASX:LFS:3A689871/pdf/inline/fy25-annual-report

- https://announcements.asx.com.au/asxpdf/20250822/pdf/06n5t2c6ldwfl7.pdf

- https://finance.yahoo.com/news/latitude-group-holdings-ltd-asx-070106743.html

- https://www.tipranks.com/news/company-announcements/latitude-schedules-fy25-full-year-results-briefing-for-20-february