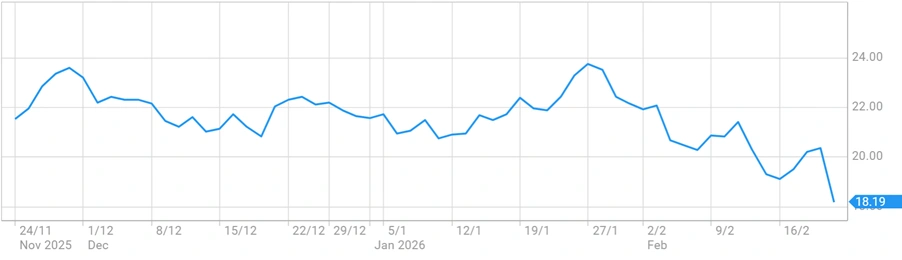

Guzman y Gomez Limited (ASX: GYG) hit a record low on Friday, 20th February 2026, after releasing its first-half FY26 results. Despite reporting a 45% jump in net profit, investors sent the stock plunging as deep as 16.5% in early trade, reacting to sluggish US sales, a missed revenue consensus, and widening losses in North America.

The GYG shares crashed to AUD 17.00 in morning trade before recovering slightly to AUD 18.31 – still a bruising 10.11% decline at midday AEDT. That intraday low marks a new record since the company’s IPO in June 2024, sitting approximately 23% below its listing price of AUD 22.00 and 63% off its all-time high of AUD 45.99 set a year ago.

GYG Price chart [ASX]

The Numbers Behind the Sell-Off

On paper, Guzman y Gomez delivered a solid half. For the six months to 31st December 2025:

- Group network sales rose 18% to AUD 681.8 million

- Revenue grew 23% to AUD 261.2 million

- Group underlying EBITDA climbed 23.3% to AUD 33.0 million

- Statutory net profit after tax (NPAT) jumped 44.9% to AUD 10.6 million, up from AUD 7.3 million a year earlier

The company also declared a fully franked interim dividend of 7.4 cents per share, with an ex-dividend date of 13th March 2026 and payment due 31st March 2026. Its balance sheet remains in good shape, with AUD 236.4 million in cash and no debt.

So why did investors run?

US Operations: The Sore Spot

The American segment remains the central point of concern. US network sales rose 67% to AUD 8.2 million, but that growth came entirely from new restaurant openings rather than any meaningful lift in underlying demand. The US segment underlying EBITDA loss widened sharply to AUD 8.3 million, up from a AUD 5.0 million loss in the prior corresponding period.

Management confirmed that US losses are expected to increase slightly through the full year to June 2026, compared with an AUD 13.2 million loss in FY25. The company is also navigating a transition in delivery partnerships, having ended its arrangement with DoorDash in favour of an exclusive deal with Uber Eats. Analysts flagged the short-term sales pressure this transition could create.

The US market is fiercely competitive,e and consumers are still pulling back on discretionary spending. Each American restaurant needs to generate at least USD 3 million in annual sales to be sustainable, according to co-CEO and founder Steven Marks – a bar that current US locations have yet to consistently clear.

Australia Holds Firm, But Comps Soften

Back home, Australia remains the engine. Australian network sales increased 17.5% to AUD 673.6 million, driven by new restaurant openings and extended trading hours, with 31 locations now operating around the clock.

Comparable sales growth came in at 4.4% for the half, an improvement over Q1 but still softer than some investors had anticipated. Corporate restaurant margins dipped slightly to 17.6% from 18.0%, which management attributed to newer stores still ramping up. Median franchise restaurant margins improved to 21.4%, and median return on investment hit 48%.

GYG opened 17 restaurants globally during the half, 14 in Australia, and finished the period with 272 restaurants across Australia, Asia and the United States. The development pipeline sits at 108 sites, with more than 85% in drive-thru format.

A Guzman y Gomez drive-thru location, a format the company is doubling down on across its Australian expansion. [Guzman y Gomez]

Market and Analyst Reaction

Despite the profitable result, Citi analysts captured the market’s mood well. “The company is executing well, but not as fast as the market is expecting,” Investing.com wrote, adding that it was hard to see what in the result would compel investors to chase the stock higher given the current valuation.

Group network sales of AUD 681.8 million also missed the Visible Alpha consensus of AUD 687.3 million, giving bears a concrete number to point to.

GYG shares have now fallen roughly 52% over the past 12 months, a stark underperformance against the S&P/ASX 200 Index, which has gained approximately 9% over the same period. The stock is now down around 15% in the 2026 calendar year alone.

As noted in an earlier report on GYG’s entry into the ASX 200, the company debuted with significant fanfare and an AUD 2.2 billion valuation when it listed in June 2024 – expectations that now clearly weigh on the share price.

Also Read: Alcoa Hit with Australia’s Largest Conservation Fine After Six Years of Illegal Forest Clearing

What’s Next

GYG maintained its FY26 guidance. In Australia, the Company expects to open 32 new restaurants for the full year, with around 85% in drive-thru format. Australian segment underlying EBITDA margins are forecast at 6.0% to 6.2% of network sales, up from 5.7% in FY25.

In the US, management says restaurant productivity and margins will improve over time as the network matures, though losses are forecast to rise slightly before the situation improves. The Company has also completed AUD 27 million of share repurchases under its AUD 100 million on-market buyback.

For investors, Friday’s result raises a simple question: Is the sell-off a reset opportunity in a fundamentally sound business, or does the market still have more multiple compression ahead? The answer likely depends on how quickly the US chapter develops – and whether that development comes fast enough for a market that has already waited long enough.