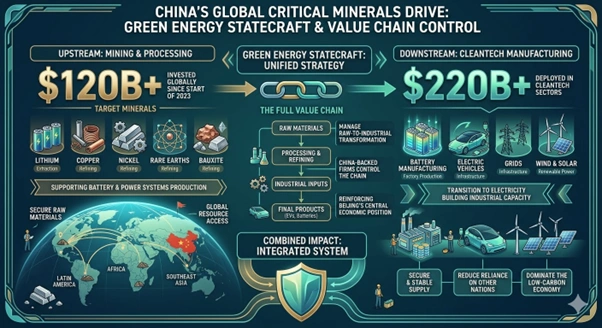

China spent more than $120 billion on mining and upstream processing in nations across the globe since the start of 2023. These funds target the extraction of lithium, copper, nickel, rare earths, and bauxite. This expenditure supports the production of batteries and power systems for the transition to electricity.

The nation pursues a strategy of green energy statecraft to manage the full value chain of these materials. This plan ensures that firms from China control the transformation of materials into inputs for industry. The scale of this movement reinforces the position of Beijing at the centre of the economy.

China also directs $220 billion toward downstream sectors, including the manufacture of batteries and vehicles. These investments fund the construction of grids and infrastructure for wind and solar power. The combination of these sectors creates a system that secures supply and reduces reliance on other nations.

Figure 1: China’s global critical mineral drive

Supply Chain Control Impacts International Economic Stability

Control over these materials allows Beijing to influence the pricing and availability of technology. Market participants monitor these developments as they affect the cost of energy and transport. The concentration of processing power in one nation creates risks for the stability of trade.

China currently manages 90% of the refining for rare earths and 60% of the processing for lithium. The nation also handles 70% of cobalt refining and produces half of the steel for the world. These figures demonstrate the reach of the industrial system built by the state.

Western governments realise the implications of this dominance for their own security. Leaders in the United States and Europe seek to build capacity to process materials within their borders. These efforts aim to provide alternatives to the current concentration of supply.

- China produces 90% of cathode and anode materials.

- The nation controls 70% of global cobalt refining.

- Firms manage 60% of lithium processing worldwide.

Climate Energy Finance Tracks State-Backed Industrial Strategy

The think tank Climate Energy Finance (CEF) from Australia released these findings in a report last week. Researchers from this organisation documented the flow of capital from firms into mines and factories. These experts describe the approach as a coordinated effort to secure resources for decades.

Tim Buckley co-authored the report and serves as the founder of CEF. He notes that the model of investment has changed to include collaboration with host governments. This shift addresses previous concerns regarding the extraction of wealth without local benefit.

State institutions provide the financing that allows private firms to operate with speed. This hybrid model combines the direction of the state with the efficiency of the market. These entities work together to implement the industrial goals of the nation.

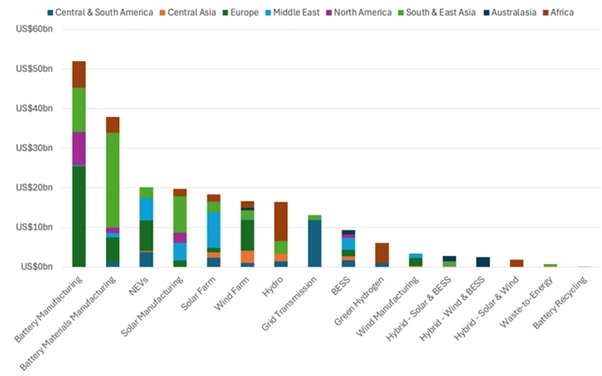

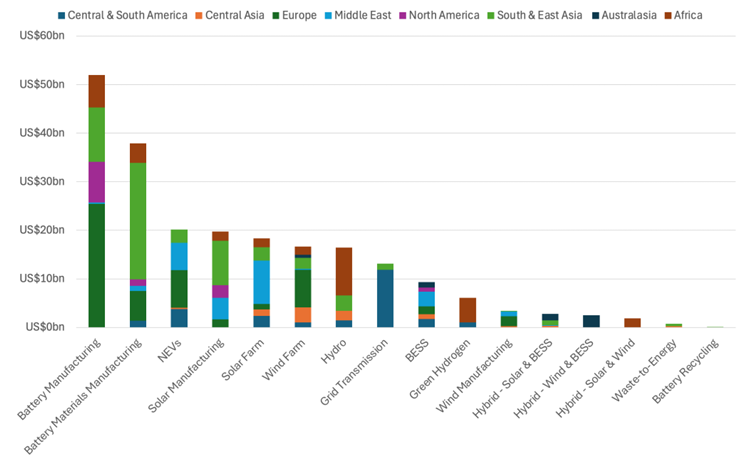

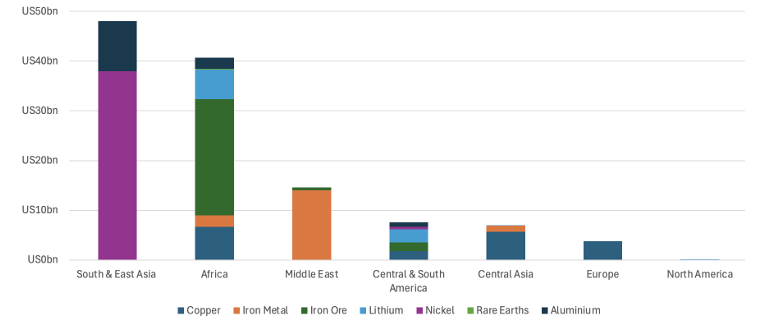

Figure 2: China’s cleantech OFDI by region (2023-2025) [CFE]

Resource Wealth Drives Investment in the Global South

The flow of capital targets regions in Africa, Latin America, and Southeast Asia. The Democratic Republic of Congo hosts projects that expand the production of copper and cobalt. Firms from China maintain a presence in these areas to ensure access to these minerals.

Indonesia serves as a primary location for the production and processing of nickel. Investment from China helped this nation become the largest producer of this metal. Zimbabwe also sees the development of the capacity to mine and process lithium.

- Democratic Republic of Congo: Copper and cobalt extraction.

- Indonesia: Nickel production and processing facilities.

- Zimbabwe: Lithium mining developments.

Firms build railways and ports to move materials from mines to the coast. They also establish power systems to support the operation of industrial facilities. These projects enable nations to develop their own industrial capacity while providing a supply to China.

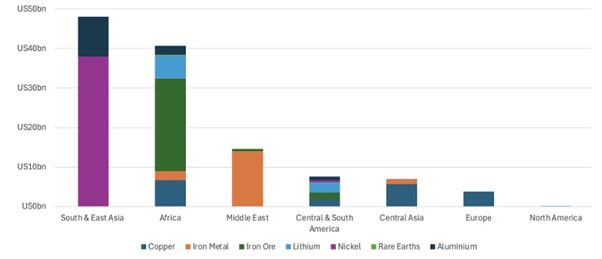

Figure 3: China’s FDI into mining and upstream processing (2023-2025) [CFE]

Strategic Acceleration Commences Following 2023 Policy Shift

The current wave of spending began in early 2023 and continues through 2026. This period marks a transition away from the earlier methods used in the Belt and Road Initiative. The strategy now focuses on deep integration within the industrial sectors of partner nations.

Beijing adapts its plans to meet the changing conditions of the politics and the economy. The trajectory shows a movement toward expansion rather than a retreat from the market. This timing allows the nation to stay ahead of competitors who seek to diversify their supply.

The speed of execution remains a factor in the success of these projects. Firms reach agreements and begin construction faster than their counterparts in the West. This advantage ensures that the supply of materials meets the demand of the factories in China.

Also Read: Gas Prices in Europe Rise 35 Per Cent After Strike on Hub in Qatar

Collaborative Infrastructure Models Secure Long-Term Supply Agreements

China secures supply by building facilities that process materials before they leave the host nation. This approach allows host countries to capture more value from their own resources. These governments sign agreements that guarantee the delivery of materials to China for years.

“This approach aligns China’s resource security goals with host countries’ ambitions to capture more value domestically and accelerate their own industrial development,” says Tim Buckley.

The US-led Minerals Security Partnership seeks to create different pathways for the trade of minerals. The European Union uses the Critical Raw Materials Act to encourage the mining of materials in Europe. These initiatives aim to reduce the influence of Beijing on the global market.

The competition for these resources will shape the development of technology for the next decade. Nations that control the processing of minerals will hold the power in the transition to power. This strategy ensures that China remains the primary source of the inputs for the energy of the future.

Disclaimer: This article provides information for general purposes only. It does not constitute financial or investment advice. Market conditions and critical mineral supply chains change rapidly. Readers should consult official government reports or qualified advisors for the most current data.

Sources

- https://www.mining.com/china-spent-120b-to-lock-down-critical-minerals-dominance-report

- https://climateenergyfinance.org

{kind=link}

{kind=link}