BHP Group Limited (ASX: BHP) has wiped more than 20% off its value in less than a month. Here’s what drove the selloff, who’s feeling the pain, and what investors should do next.

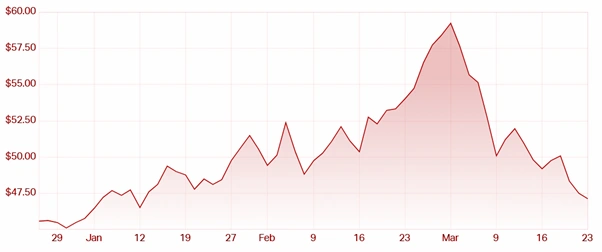

Australia’s largest mining company opened in March at an all-time high of $59.25 and has since tumbled to $47.11, a gut-wrenching reversal for anyone holding shares right now. If you’re watching the BHP share price Australia and asking yourself whether to cut your losses or stay the course, you’re not alone.

Figure 1: BHP Share price performance [Market Index]

From Record Highs to a Sharp Reversal

BHP’s Blockbuster Start to March

The BHP share price Australia investors track so closely surged to an all-time peak of $59.25 on 2 March 2026. The trigger was a standout half-year earnings result that sent the market into a buying frenzy.

BHP reported a 22% jump in underlying net profit after tax. It also hiked its fully-franked interim dividend to 73 US cents (AU$1.03) per share, up 30% in Australian dollar terms and a remarkable 46% in US dollar terms.

The record-breaking earnings result that pushed BHP shares to an all-time high sent the stock surging nearly 18% in a matter of days. Investors were euphoric.

That euphoria didn’t last long.

What Drove the BHP Share Price Down So Hard?

Several Headwinds Struck in Quick Succession

The crash wasn’t the result of one bad announcement. A cluster of negative developments hit BHP throughout March, and the market responded by selling aggressively.

Here’s what knocked the stock down:

- Ex-dividend pricing: BHP shares went ex-dividend in the first week of March. Once the entitlement date passes, buying demand typically cools — and that’s exactly what happened.

- Queensland mines losing ground: Reports surfaced that BHP’s Queensland coal operations can no longer compete for new capital investment, with the company generating little return from those assets.

- Geopolitical pressure: Escalating tensions in the Middle East — driven by the continuing US and Israeli conflict with Iran — rattled commodity markets and raised serious concerns about the global demand outlook for metals and coal.

- CEO transition: In mid-March, BHP confirmed that Chief Executive Mike Henry would step down. Brandon Craig will step into the CEO role on 1 July 2026. You can read more about what the BHP CEO change from Mike Henry to Brandon Craig means for the company’s future direction.

Any one of these factors alone would have rattled investor confidence. All four landings in the same month created a perfect storm.

Who Is Feeling the Most Pain?

Long-Term Holders vs Recent Buyers

The damage is unevenly distributed. Investors who entered BHP more than 12 months ago are still comfortably ahead, the stock has delivered +19.15% over the past year and still sits 13.66% above ASX 200 levels from this time last year.

But investors who chased the post-earnings momentum near $59.25 are sitting on deep losses. Those buyers bought at peak excitement, and March has been brutal for them.

Despite the monthly rout, the broader picture still reflects a formidable company:

- 2026 year-to-date performance: +3.56%

- Market capitalisation: $239.27 billion

- ASX rank: 2nd out of 2,315 listed companies

- Sector rank: 1st out of 1,106 Basic Materials companies

This is not a company in structural decline. But the near-term risks are real and shouldn’t be dismissed.

Should Investors Sell, Hold, or Buy More?

What the Analysts Are Saying Right Now

Despite the savage month, most analysts covering the BHP share price Australia have not turned bearish.

TradingView data shows that of 20 analysts, 11 rate BHP as a hold and 7 carry a buy or strong buy rating. Only two analysts have a sell recommendation.

The average price target sits at $52.94, implying roughly 14% upside from the current $47.11. The broker consensus from ASX data also leans Buy, with 5 buying recommendations and 4 holds, and zero sell ratings.

The bull case is compelling: some analysts tip BHP to climb as high as $68.22, a 47% gain from today’s levels. Bears put downside risk at $34.11.

The Fundamentals Still Stack Up

BHP’s core financial metrics continue to hold up well:

- EPS: $2.866

- DPS: $1.9577

- Book Value Per Share: $14.031

- Bid/Ask: $46.99 – $47.11

The underlying business that produced record earnings hasn’t changed overnight. The selloff looks more like a sentiment-driven correction than a fundamental collapse.

How Does BHP Stack Up Against Its Rivals?

Sector Context Matters

BHP isn’t suffering in isolation. The broader resources sector has struggled throughout March as geopolitical uncertainty weighs on commodity demand forecasts across iron ore, copper, and coal.

Rival Rio Tinto (ASX: RIO) has also felt the pressure, though BHP’s exposure to underperforming Queensland coal assets adds a layer of complexity that Rio doesn’t face to the same degree. For a detailed look at how these two mining giants compare on infrastructure strategy and operational efficiency, our breakdown of <arel=”nofollow” href=”https://colitco.com/bhp-vs-rio-tinto-port-hedland-expansion-efficiency/”>BHP vs Rio Tinto at Port Hedland is worth a read.

The Bottom Line: Stay Calm and Look at the Long Game

The 21% crash in the BHP share price Australia investors are watching is alarming on the surface. But the numbers tell a more nuanced story.

BHP holds a $239 billion market cap, sits second on the ASX, and carries analyst consensus that still points firmly to buy-to-hold territory. The triggers behind the March crash, ex-dividend mechanics, a CEO transition, Queensland asset concerns, and geopolitical noise, are legitimate headwinds, but they don’t signal a break in the company’s fundamental strength.

For long-term investors, panic selling rarely pays off with blue-chip miners. For those who bought near the peak, waiting for a recovery toward the analyst consensus of $52.94 looks more sensible than locking in a loss right now.

For investors watching from the sidelines, the current level may offer a genuine entry point, provided you’re approaching it with a multi-year horizon and an understanding of the risks involved.

Disclaimer: This article is for general informational purposes only and does not constitute financial, investment, or legal advice. The information provided reflects publicly available data and analyst commentary at the time of publication. Past performance is not a reliable indicator of future results. Always consider your personal financial situation and consult a licensed financial adviser before making any investment decisions. The author holds no position in any of the securities mentioned.

Frequently Asked Questions (FAQs)

Q: Why did the BHP share price Australia drop so sharply in March 2026?

Ans: Several factors hit BHP in quick succession — the stock went ex-dividend in early March, reports emerged that Queensland coal mines were no longer attracting capital investment, geopolitical tensions in the Middle East weighed heavily on commodity markets, and BHP announced that CEO Mike Henry would step down in July. Together, these events wiped over 21% off the share price in under a month.

Q: Should I sell my BHP shares after the March 2026 crash?

Ans: Most analysts say no. Of 20 analysts tracked by TradingView, 11 rate BHP as a hold and 7 carry a buy or strong buy rating. The average price target sits at $52.94 — around 14% above the current price of $47.11. The broker consensus also leans buy. Unless your personal financial situation demands liquidity, panic selling a blue-chip miner after a sentiment-driven correction rarely works in an investor’s favour.

Q: Is the BHP share price likely to recover in 2026?

Ans: The underlying fundamentals remain solid. BHP holds a $239 billion market cap, ranks second on the ASX, and delivered record earnings just weeks before the selloff. The 2026 year-to-date return is still positive at +3.56%, and the stock sits nearly 20% above where it traded this time last year. While short-term headwinds remain — including the CEO transition and commodity demand uncertainty, the analyst consensus points to meaningful upside over the medium term.

Sources

- https://www.fool.com.au/2026/03/23/bhp-shares-crash-21-in-march-so-far-time-to-sell-up/

- https://www.tradingview.com/symbols/ASX-BHP/forecast/

- https://www.asx.com.au/markets/company/bhp