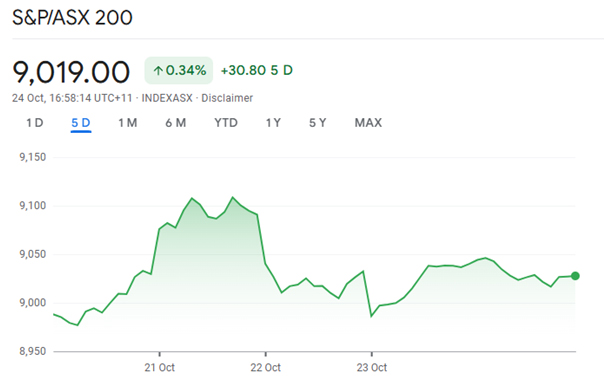

Australia’s main stock market index, the ASX 200, stands at 9,019 points after closing on Friday, October 24, 2025, losing 0.15% from the previous session. The index climbed 2.8% over the past month and is up 9.84% compared to this time last year. Investor sentiment is buoyed by strong macroeconomic factors and sector performance.

ASX 200 performance on 24th October

Banking Sector Turns Heads

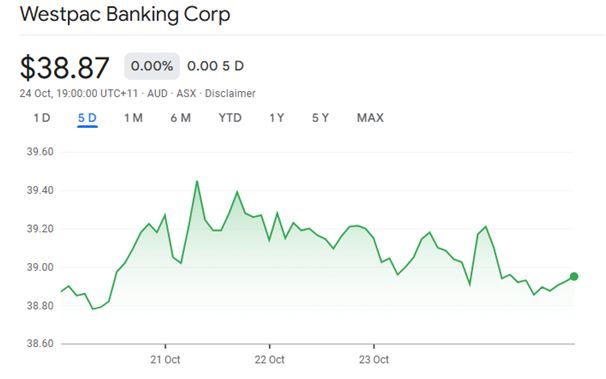

Major banks led gains in the banking sector during the previous week, fuelled by the Reserve Bank of Australia’s cautious approach to interest rates. Westpac and other bank shares rose following the release of September policy meeting minutes, which hinted at no immediate rate cut. This stable interest rate environment encouraged investor confidence, driving bank valuations higher.

Westpac’s share performance last week

Mining Sector Shows Strength

Mining stocks posted their strongest weekly gain in a year, driven by rising copper prices over supply concerns. BHP and Rio Tinto delivered positive performances, reflecting investor optimism in the materials sector. The minerals sector continues to attract attention, with the US-Australia critical minerals deal acting as a catalyst for growth and investment.

Energy Sector Rallies

The energy sector experienced a significant rally, contributing to the ASX 200’s rise to a record-high intraday reading of 9,115.2 points. Energy share price gains reflected optimism about global consumption and resource demand. Sanctions on major Russian oil producers fuelled the sector’s outperformance.

Volatility Remains Present

Volatility persists in the market. The ASX 200 fell by 0.8% or 73.1 points during the October 17 session, dropping to 8,995.3 points following earlier highs above 9,100 points. Political uncertainty and risk repositioning prompted broad sector rotation, with institutions increasing trading volume. Gold stocks gained up to 2.9% on that day, underscoring safe-haven demand amid uncertainty.

ASX 200’s last week’s performance

Consumer Confidence Index Drops

The Westpac-Melbourne Institute Consumer Sentiment Index declined by 3.5% to 92.1 in October, marking the steepest fall since April. Decreased consumer confidence signals possible pressure on companies reliant on domestic consumption. Sectors exposed to consumer demand may see potential earnings downgrades as a result.

Profit-Taking Influences The Market

Profit-taking in financial and gold stocks weighed on the index late in the week, tempering recent gains. Investors moved into a risk-averse stance ahead of critical inflation data releases from Australia and the United States. Sell-offs in these sectors highlight market vulnerabilities and suggest an evolving outlook for risk assets.

Inflation Figures Awaited

Investors will watch inflation data closely. The Australian interest rate market is pricing in a 17 basis point move, reflecting a 65% chance of a 25 basis point rate cut at the next RBA meeting. In the June quarter (Q2), headline inflation rose by 0.7%, as the annual rate eased to 2.1%, the lowest since March 2021. The RBA’s preferred trimmed mean inflation measure increased 0.6% QoQ, causing the annual trimmed mean to drop to 2.7%.

Market Forecasts For The Coming Week

Forecasts put the ASX 200 at 9,005 on Monday, October 27, with a possible maximum of 9,635 and a minimum of 8,375. By Wednesday, the index may reach 8,944, with projections ranging from 8,318 to 9,570. The ASX 200 is expected to trade at 8,882.03 points by quarter’s end and at 8,305.60 in 12 months. Analysts foresee continued gains if bond yields remain steady and global data do not prompt fresh volatility.

Sector-Specific Insights

- Materials: Investors should observe copper, lithium, and gold companies. Copper prices rose, boosting major miners, while gold stocks benefitted from safe-haven buying during uncertainty.

- Energy: Oil and gas stocks surged after sanctions on Russian producers and anticipation of increased global demand.

- Financials: Banks outperformed, reflecting stable policy signals and new consumer credit figures.

- Technology: Life360 and other tech stocks fell 8% in one session, underscoring volatility in growth-oriented sectors.

Undervalued Stocks and Opportunities

Analysts point to opportunities in undervalued stocks, such as Cyclopharm Limited and Nickel Industries, which trade at lower valuations amid market volatility. Elders and PolyNovo attract investor attention for their sector resilience and growth potential. The dynamic environment presents chances for growth for those who identify stocks with strong fundamentals.

Nickel Industries Ltd’s performance in the last week

Key Corporate Actions

- Litchfield Minerals seeks to raise $6 million from a private placement.

- Australian Strategic Minerals plans a $50 million institutional placement at $1.20 per share.

- White Oak Global Advisers moves to acquire Sanjeev Gupta’s manganese smelter in Tasmania with an $80 million restart plan.

- Infratil increases its stake in Contact Energy to 14.3%.

- Bank of America sets final bids for Westpac’s $30 billion RAMS loan book this week.

- Air T plans to acquire Rex Express after its administration period.

- BHP Group’s WA nickel assets may be sold to Gold Fields.

- Credit Clear launches a $14 million placement to fund its $11 million UK acquisition.

- LGI Ltd raises $40 million for growth opportunities.

- Macquarie Group intends asset platform changes, affecting fund managers with assets below $300 billion.

Political Developments Shape Sentiment

A successful meeting between Prime Minister Anthony Albanese and President Donald Trump brought renewed focus on critical minerals and AUKUS partnership, boosting overall market sentiment. Continued US-China diplomatic engagement, with leaders scheduled to meet in South Korea, may further ease geopolitical tensions.

Also Read: GPT Group Makes Bold Play for Sydney’s Crown Jewel: $860M Stake in Grosvenor Place

Broker Recommendations For Next Week

Top brokers name BHP Group Ltd and select other ASX stocks as prime buys, citing sector leadership and positive macroeconomic trends. These recommendations are informed by sectoral rotation, earning projections, and global commodity dynamics.

Investor Strategies Moving Forward

Institutional and retail investors are advised to remain vigilant in tracking upcoming inflation figures, central bank policy updates, and evolving global data releases. Portfolio rebalancing is likely to continue, with sector rotation favouring energy, banking, and materials, while technology stocks may remain volatile.

Conclusion

Australia’s ASX 200 enters the new week with underlying strength, supported by positive economic data, upbeat banking and mining sector performances, and encouraging international developments. The next week’s trading will reflect movements in inflation data, global political developments, and sector-specific trends, shaping investor strategies across Australia’s dynamic financial landscape.