The Reserve Bank of Australia has raised the cash rate by 25 basis points to 4.10 per cent, marking the second rate increase in 2026 following an earlier hike at its 3 Feb 2026 meeting. For Australian homeowners and investors, the decision has reignited the ASX vs mortgage calculator question: is it better to direct surplus cash toward paying down a mortgage or continuing to invest in the sharemarket?

Figure 1: Reserve Bank building in Sydney [Courtesy: MBC Group]

As covered in Colitco’s earlier report on the RBA’s 17 Mar 2026 decision, the Board cited rising inflation pressures, a tightening labour market, and the global energy price shock linked to the conflict in the Middle East as the key drivers behind the move. Here, leading market analysts break down what the hike means for mortgage holders and those weighing the best ASX dividend stocks against the certainty of debt reduction.

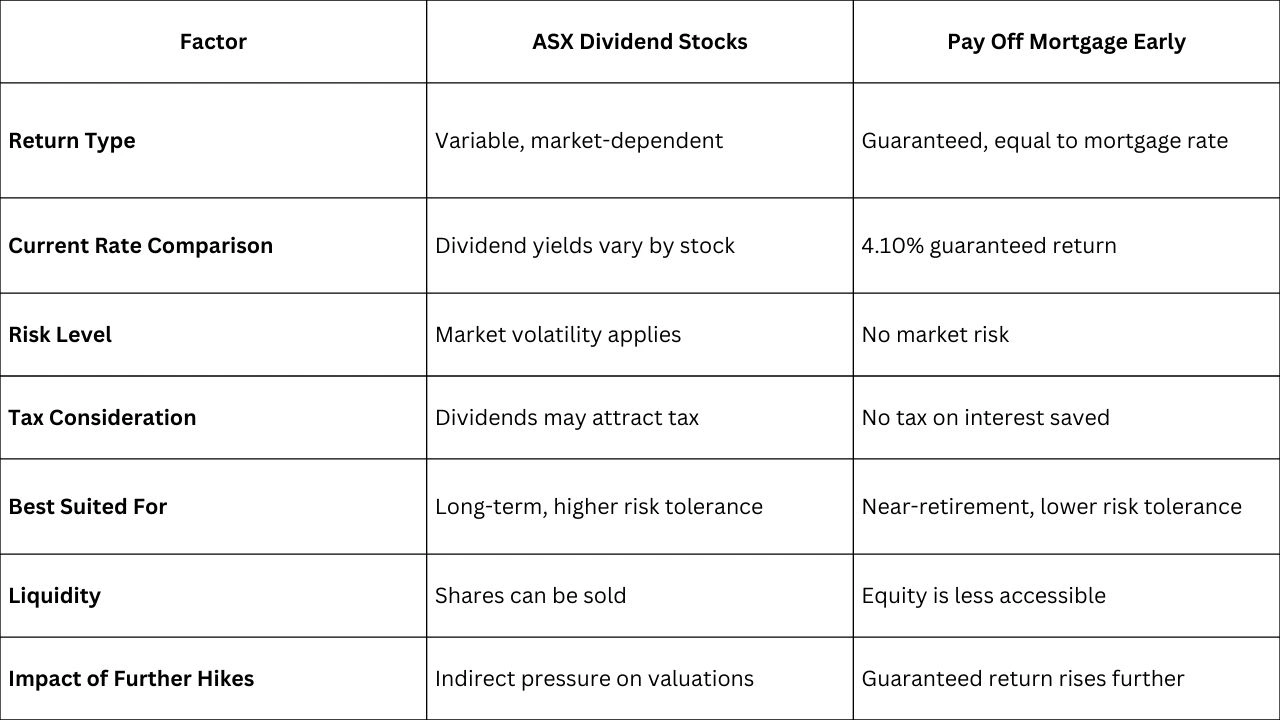

ASX vs Mortgage Calculator: Where Does the Balance Lie?

Best ASX Dividend Stocks Offer Income but Carry Market Risk

For investors who have historically used the best ASX dividend stocks as a source of reliable income, the rising rate environment changes the comparison. As the guaranteed after-tax return of paying down a mortgage rises with each rate increase, the hurdle that sharemarket investments must clear to justify the risk also rises.

The ASX vs mortgage calculator debate does not have a single answer. It depends on individual loan rates, investment time horizons, tax positions, and risk appetite. However, the broad direction of expert commentary following the 17 Mar 2026 hike points toward mortgage holders prioritising debt reduction in the near term, particularly those on variable rates absorbing the full impact of both 2026 hikes.

Pay Off Mortgage Early or Stay Invested: What the Data Suggests

The decision to pay off mortgage early carries a guaranteed return equal to the borrower’s mortgage interest rate. At 4.10 per cent and potentially higher, that guaranteed return is increasingly competitive with the income yield available from even the best ASX dividend stocks, without the associated market volatility.

For investors with longer time horizons and higher risk tolerance, continuing to hold quality dividend-paying shares alongside a mortgage remains a defensible strategy. However, for those closer to retirement or with limited cash buffers, the current rate environment strengthens the case for prioritising debt reduction before re-entering the sharemarket with fresh capital.

Expert Reaction to the Second RBA Rate Hike of 2026

eToro’s Josh Gilbert on Why the RBA Had No Choice

eToro market analyst Josh Gilbert described the decision as one the RBA was effectively forced into. He noted that while geopolitical tensions did not create Australia’s current inflation problem, they have significantly worsened it, with the Board itself acknowledging that inflation risks have tilted further to the upside.

Mr Gilbert stated, “Mortgage repayments are going up at the same time fuel and grocery bills are surging, and that squeeze is going to hit hard and fast.”

He added that the rate relief many Australians had been counting on in 2026 no longer appears to be merely delayed. For those using an ASX vs mortgage calculator to weigh their options, the calculus has shifted materially with each successive hike.

Wealth Within’s Filip Tortevski on the RBA’s Difficult Balancing Act

Filip Tortevski, senior analyst at Wealth Within, highlighted the structural challenge facing the RBA as it tightens policy in the current environment. He noted that higher rates can slow spending and economic activity but do little to directly control the price of oil.

Mr Tortevski stated, “That leaves the RBA walking a fine line, trying to contain inflation without pushing an already fragile economy into a deeper slowdown.”

For investors evaluating the best ASX dividend stocks against the guaranteed return of paying down debt, this uncertainty around the rate path adds another layer of complexity to the decision.

The Rate Hike is Pushing Mortgage Repayments Higher

An Extra A$116 Per Month for the Average Borrower

David Koch, economic director at Compare the Market, put a direct dollar figure on the impact of the latest hike. He noted that inflation remains too pressing an issue to leave unaddressed, and that every month without action risks allowing grocery, power, and insurance costs to climb further.

Figure 2: David Koch, economic director at Compare the Market [Courtesy: Compare the Market]

Mr Koch stated: “Nobody wants another rate hike. We have already had one this year, and that means millions of homeowners are spending thousands more on their repayments.”

For those weighing whether to pay off mortgage early or redirect funds towards the sharemarket, the key figures from Mr Koch’s analysis are:

- The 25 basis point hike adds approximately A$116 to monthly repayments

- Homeowners with a loan of A$736,000 will pay A$1,392 more per year

- Millions of Australian homeowners are now spending thousands more annually on repayments

- Rising grocery, power, and insurance costs are compounding the mortgage pressure

Further Hikes Cannot Be Ruled Out in 2026

Mr Koch warned that the current rate cycle may not yet be over. With no RBA meeting scheduled for April, the Board sits again in May and a further six times across the remainder of 2026. He encouraged homeowners to prepare for the possibility of additional hikes and to review whether their current rate remains competitive.

Mr Gilbert echoed this caution, noting that if oil prices remain elevated, the case for another hike will only gain momentum. He added that a resolution to the Middle East conflict and a return of crude prices to lower levels could make the 17 Mar 2026 hike the last of the cycle but flagged that this outcome feels more like wishful thinking than a base case at present.

Industry Outlook

The ASX vs mortgage calculator question is likely to remain a live debate for Australian households through 2026. With the RBA signalling it will remain data-dependent and additional hikes possible if oil prices stay elevated, the cost of carrying variable rate debt will continue to rise in worst-case scenarios. The best ASX dividend stocks continue to offer attractive income streams for long-term investors, but the risk-adjusted appeal of debt reduction has grown considerably since the rate-cutting cycle of 2025 went into reverse. Financial advisers are likely to see increased demand for personalised guidance as households navigate this shifting environment.

Future Direction and Impact

The second RBA rate hike of 2026 has drawn a clear line between those who entered the year expecting further rate relief and those now adjusting their financial plans to absorb continued tightening. Whether to pay off mortgage early or maintain sharemarket exposure through the ASX stocks is a question with no universal answer, but one that is becoming more urgent for millions of Australian households.

For ongoing coverage of the RBA rate path, mortgage impacts, and the ASX vs mortgage calculator debate, readers can follow Colitco’s dedicated coverage of Australian markets and personal finance developments through 2026.

ALSO READ: Two ASX Blue-Chips Are Bleeding Quietly as Oil Blows Past US$100 a Barrel

Frequently Asked Questions

Q1. What is the current RBA cash rate?

Ans. The RBA increased the cash rate to 4.10% on 17 Mar 2026, marking the second hike this year.

Q2. How much more will mortgage holders pay?

Ans. The latest hike adds around A$116 per month, or about A$1,392 annually, on an average A$736,000 loan.

Q3. Should I use an ASX vs mortgage calculator?

Ans. Yes, it helps compare the guaranteed return from paying down debt with potential returns from investing, based on your situation.

Q4. Are ASX dividend stocks still attractive?

Ans. They can still provide a steady income, but rising interest rates make mortgage repayment a more competitive option.

Q5. Is it better to pay off a mortgage or invest right now?

Ans. Many experts suggest prioritising debt reduction in the short term, while long-term investors may still benefit from staying invested.

Sources

The Motley Fool Australia — Buying ASX shares or paying off a mortgage? Here’s what the experts are saying about RBA interest rate hikes in 2026, published 18 Mar 2026 https://www.fool.com.au/2026/03/18/buying-asx-shares-or-paying-off-a-mortgage-heres-what-the-experts-are-saying-about-rba-interest-rate-hikes-in-2026/

Reserve Bank of Australia — Cash Rate Decision Statement, 17 Mar 2026 https://www.rba.gov.au

{kind=link}

{kind=link}