Amazon.com Inc. (NASDAQ: AMZN) CEO Andy Jassy outlined a striking possibility in his 2026 annual shareholder letter. The Company may begin selling its own Amazon AI chip racks directly to third-party customers, a move that would place it in more direct competition with Nvidia and AMD.

Figure 1: Amazon.com Inc. corporate branding [Courtesy: Mercury News]

The letter, released on 9 Apr 2026, also addressed the state of AWS, Amazon custom AI silicon demand, and the broader question of whether artificial intelligence investment is justified. Jassy argued clearly that it is.

AWS AI Revenue Has Already Crossed a US$15 Billion Annual Run Rate

Amazon Web Services is growing at a pace Jassy described as capacity-constrained, not demand-constrained. AWS AI revenue is now running at more than US$15 billion annually as of Q1 2026 and continues to rise.

Despite adding 3.9 gigawatts of capacity in 2025, Amazon says demand remains extremely strong. The Company plans to double that capacity by 2027, though supply is still struggling to keep pace.

Graviton and Trainium Both Facing Overwhelming Customer Demand

The scale of demand for Amazon’s custom AI silicon has become a strategic inflexion point. Two large AWS customers have separately asked whether they can acquire all of Amazon’s custom Graviton CPU capacity for 2026. Amazon cannot agree to that request, as it must preserve capacity for its broader customer base.

The Trainium picture tells a similar story. The current Trainium2 chip is sold out. AWS Trainium 3, which began shipping at the start of 2026, is described by Jassy as nearly fully subscribed. The AWS Trainium 3 price dynamic is being shaped by demand that arrived before supply could fully scale.

Jassy Quoted Directly on What Chip Demand Could Mean for AWS Economics

Jassy addressed the opportunity created by Amazon’s chip position in clear terms:

“Having our own hotly demanded AI chip opens up many possibilities, but perhaps none larger than the ability to lower costs for customers and secure better economics for AWS. At scale, we expect Trainium will save us tens of billions of capex dollars per year, and provide several hundred basis points of operating margin advantage versus relying on others’ chips for inference.”

Figure 2: Andy Jassy, Chief Executive Officer of Amazon [Courtesy: Yahoo Finance]

The Case for Selling Amazon AI Chip Racks to Third Parties

Amazon’s chip business currently carries an annual revenue run rate of US$20 billion, growing at triple-digit percentages year over year. Jassy acknowledged this figure is understated because the Company only monetises its chips through the AWS EC2 service.

If treated as a standalone business, Jassy said Amazon’s chip revenue would carry a run rate of approximately US$50 billion. That gap between the current figure and the potential standalone value is precisely what makes the case for direct Amazon AI chip rack sales to third parties compelling.

Jassy was direct about the possibility:

“There’s so much demand for our chips that it’s quite possible we’ll sell racks of them to third parties in the future.”

Amazon Custom AI Silicon as a Competitive Weapon Against Nvidia

Jassy took a pointed position on the competitive landscape while addressing the shareholder letter. Amazon continues to use Nvidia chips, but customers are actively seeking better price-performance outcomes. That demand, he argued, is what is driving uptake of Amazon’s custom AI silicon.

The Trainium line is positioned as a cost-efficiency tool, not simply a performance alternative. Amazon’s view is that its custom chips will save the Company tens of billions in capital expenditure annually at scale, while also improving operating margins by several hundred basis points compared to relying on external chip suppliers.

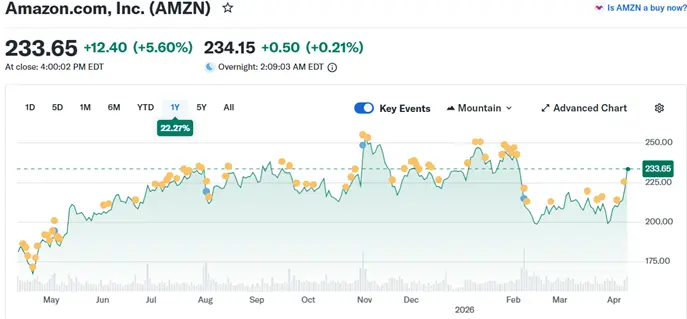

Wall Street analysts hold a Strong Buy consensus on AMZN stock, based on 43 Buy ratings and three Hold ratings assigned over the past three months. The average analyst price target stands at US$284.34 per share, implying approximately 23.9% upside from recent levels.

AMZN NYSE Share Price

Amazon.com Inc. (NASDAQ: AMZN) is currently trading at US$233.65 per share, with a market capitalisation of US$2.513 trillion. The 52-week range stands at US$165.29 to US$258.60 per share.

Figure 3: AMZN one-year share price performance[Courtesy: Yahoo Finance]

Industry Outlook

The global AI infrastructure buildout is driving unprecedented demand for custom silicon, with hyperscalers moving aggressively to reduce dependency on third-party chip suppliers. Amazon, Google, and Microsoft are all developing proprietary chip architectures designed to lower costs and improve performance at scale.

The US$200 billion Amazon has committed to capital expenditure in 2026 alone signals the scale of conviction behind AI infrastructure investment. For the broader semiconductor market, the entry of cloud providers as potential direct chip sellers represents a structural shift in how AI compute is sourced, priced, and distributed.

Future Direction and Impact on Amazon AI Chip Rack Investors

The next critical question for investors is whether Amazon formalises its Amazon AI chip rack sales strategy or keeps Trainium capacity within the AWS ecosystem. Jassy was careful to frame third-party sales as a possibility, not a confirmed direction.

For those tracking AWS Trainium 3 price dynamics, the near-full subscription of Trainium3 despite only beginning to ship in early 2026 suggests pricing power and strong institutional interest. If Amazon moves to sell racks externally, it would represent a new and material revenue stream sitting outside the current US$20 billion run rate.

Amazon custom AI silicon is already shaping AWS economics. The question investors are now asking is how far beyond AWS that influence could extend.

Frequently Asked Questions

Q1. What did Andy Jassy say about Amazon AI chip racks?

Ans. Jassy said that given the level of demand for its chips, Amazon may sell racks of them directly to third-party customers in the future.

Q2. What is the current AWS Trainium 3 price situation?

Ans. Trainium3 only began shipping at the start of 2026 and is already nearly fully subscribed, reflecting extremely strong demand ahead of full availability.

Q3. What is Amazon’s chip business revenue run rate?

Ans. The chip business currently runs at US$20 billion annually. Jassy said it could reach approximately US$50 billion if treated as a standalone business.

Q4. How does Amazon custom AI silicon compare to Nvidia?

Ans. Amazon says Trainium chips offer better price-performance and could save the Company tens of billions in annual capital expenditure at scale, with hundreds of basis points of margin advantage.

Q5. What is the Wall Street consensus on AMZN stock?

Ans. Analysts hold a Strong Buy consensus based on 43 Buy ratings and three Holds, with an average price target of US$284.34 per share, implying around 23.9% upside.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or investment advice. All content is based on reporting published on 9 Apr 2026 and 10 Apr 2026. Share price data reflects figures available at the time of publication. Investing in securities involves risk. Readers should conduct their own research and seek independent financial advice before making any investment decisions. Colitco does not hold any position in the companies or organisations mentioned.