Americans hoping for relief from stubborn price pressures received mixed signals from the latest inflation data. The December Consumer Price Index report released Tuesday morning showed headline inflation holding firm at 2.7% annually, defying predictions of easing costs and placing fresh scrutiny on President Trump’s economic stewardship ahead of the 2026 midterms.

Core inflation, which strips out volatile food and energy costs, delivered the silver lining. It rose just 0.2% monthly and 2.6% annually, matching the slowest pace since March 2021.

The report arrives at a politically sensitive moment. Trump faces mounting criticism over affordability challenges, with tariff-related price increases expected to intensify throughout early 2026 despite White House assurances that costs are “coming down tremendously.”

December CPI Data: What the Numbers Reveal

The Bureau of Labor Statistics report showed consumer prices rose 0.3% in December from November, meeting economists’ expectations but offering little comfort to households grappling with accumulated inflation since 2020.

Key December inflation metrics:

- Headline CPI: 2.7% year-over-year (unchanged from November)

- Core CPI: 2.6% annually (matching November’s rate)

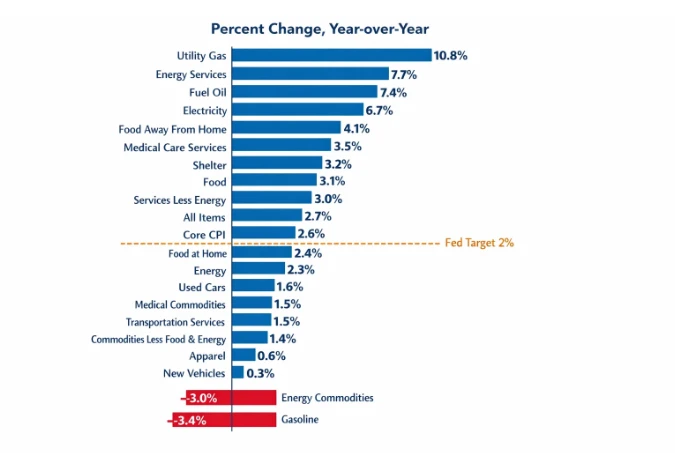

- Food prices: Jumped 3.1%, accelerating from November’s 2.6%

- Energy costs: Fell 2% monthly, with gasoline down 5.3%

- Used vehicle prices: Dropped 1.7%

The data paints a picture of an economy where inflationary pressures persist well above the Federal Reserve’s 2% target, even as some categories show improvement. Food inflation’s acceleration particularly concerns economists, given its outsized impact on consumer sentiment.

Stephen Brown, economist at Capital Economics, noted the report contained “genuine signs” that underlying inflation pressures have moderated in recent months. However, this comes after statistical issues with October and November data clouded earlier readings due to the federal government shutdown.

Consumer Price Index trends showing persistent elevation above Fed target [Bureau of Labor Statistics]

Political Fallout: Trump’s Affordability Challenge

The stubborn inflation figures compound political headaches for Trump as the 2026 midterm elections loom. Despite White House claims of rapidly cooling inflation, the data tells a different story that resonates with voters’ daily experiences at grocery stores and gas stations.

Recent polling reveals the depth of public frustration. Nearly half of Americans report struggling to afford basic necessities, while 74% characterise the economy as “mostly poor” or “at best fair,” according to a Politico/Public First survey.

Trump’s approval rating has sunk to 36%, the lowest of any president at the end of their first year in five decades.

The administration has attempted to shift blame to predecessor Joe Biden while highlighting selective achievements. White House spokesman Kush Desai stated: “President Trump inherited the worst inflation crisis in a generation from Joe Biden’s incompetence, and his Administration has rapidly cooled inflation to a 2.5% annualised rate.”

However, this narrative faces challenges. Inflation stood at 3% in January 2025 when Trump took office and has since climbed back to 2.7%, with economists attributing much of the uptick to the administration’s aggressive tariff policies.

Tariff Impact: The Bill Comes Due in 2026

Perhaps no factor looms larger over future inflation prospects than Trump’s expansive tariff regime. While 2025 saw businesses absorb roughly 80% of tariff costs, that dynamic is shifting rapidly as inventories deplete and price increases flow through to consumers.

Goldman Sachs economists estimate tariffs added 0.5 percentage points to inflation in 2025. They project an additional 0.3 percentage point increase in just the first six months of 2026 as businesses increasingly pass costs to customers.

JPMorgan warns the business-consumer split could flip to 20%-80% this year, meaning shoppers will bear the brunt of tariff-inflated prices.

Projected tariff impact on consumer prices:

- Clothing: Men’s apparel faces 30.4% tariffs, women’s 36.5%

- Beverages: Foreign beer 36.4%, wine 14.4%

- Overall cost: Total tariff costs could reach $1.2 trillion in 2026

- Consumer share: Rising from 55% currently to potentially 70%

Kyle Peacock, principal at Peacock Tariff Consulting, told CNN: “A lot of our clients really didn’t want to pass the costs on, but now they’re really having to.”

The timing creates political vulnerability. As businesses implement price increases in early 2026, voters will directly feel the pinch ahead of crucial midterm contests that could reshape Congressional control.

Also Read: Why United States Antimony Corporation Could Be Your Next Strategic Play

Federal Reserve’s Dilemma: Pause Button Pressed

Tuesday’s CPI data effectively cemented market expectations that the Federal Reserve will hold interest rates steady at its January 27-28 meeting. CME Group data shows 95% probability of no change to the current 3.5%-3.75% range.

Fed Chair Jerome Powell faces a classic central bank conundrum. The labour market shows resilience, with unemployment recently retreating from a four-year high. Yet inflation persists stubbornly above target, limiting the Fed’s ability to provide further rate relief.

The central bank cut rates three times in late 2025 to support employment, bringing the benchmark down from its 5.25%-5.5% peak. However, those cuts came despite inflation running hot, reflecting Powell’s assessment that labour market risks outweighed price pressures.

“You have one tool,” Powell said at December’s press conference. “You can’t do two things at once.”

Federal Reserve headquarters in Washington [Federal Reserve]

Ellen Zentner, chief economic strategist for Morgan Stanley Wealth Management, observed: “Today’s inflation report doesn’t give the Fed what it needs to cut interest rates later this month.”

The pause marks a shift from expectations earlier in 2025 when markets anticipated an extended easing cycle. Now, with inflation sticky and tariff pressures building, further cuts appear unlikely until clear progress emerges toward the 2% target.

Sector-by-Sector: Where Prices Are Moving

The December CPI report revealed divergent trends across consumer spending categories, with notable pressure points in everyday essentials:

- Food and groceries: The 3.1% annual increase in food prices represents a concerning acceleration. Five of six major grocery categories saw monthly gains, with only meat prices declining 0.2%. The Bureau of Labor Statistics noted widespread increases across cereals, dairy, fruits, and beverages.

- Housing and shelter: Shelter inflation reached a four-year low, offering some relief to renters and prospective homebuyers. However, monthly progress remains glacially slow, and housing costs still consume outsized portions of household budgets.

- Transportation: Used vehicle prices fell 1.7% in December, continuing a welcome downtrend. Airline fares dropped 0.5%, providing seasonal relief to holiday travellers. Overall transportation services declined 0.5% monthly.

- Energy: Gasoline prices plunged 5.3% in December amid broader oil market weakness. Total energy costs fell 2% monthly, providing the most significant disinflationary contribution.

- Healthcare: Medical care services continue creeping higher, though the pace remains moderate compared to other categories.

The mixed picture illustrates why inflation feels different to different households. Families allocating larger budget shares to groceries experience intensifying pressure, while those benefiting from lower gas prices find modest relief.

What Economists Predict for 2026

Forward-looking assessments paint an uncertain picture for the year ahead. Most forecasters expect inflation to remain elevated in the first half before potentially moderating, though tariff uncertainty clouds all projections.

Deloitte forecasts average CPI growth around 2.9% for 2025, then accelerating to approximately 3.2% in 2026 if tariffs remain elevated. This would represent a reversal of the disinflationary trend seen through much of 2024.

Mark Zandi, chief economist at Moody’s Analytics, expects “lagged effects of higher tariffs” to quicken inflation’s pace. He told Newsweek: “Businesses have been slower to pass through the higher tariffs, given the uncertainty regarding where the tariffs will ultimately land and worries about getting caught up in the political buzz saw.”

Federal Reserve projections released in December showed policymakers expecting inflation to cool to 2.4% by year-end 2026, down from 2.9% in 2025. However, this assumes tariff impacts prove temporary rather than persistent.

Stephen Smith, partner at Deloitte Access Economics, forecast “moderate growth of 1.6% in 2025, before things pick up to 2.3% and 2.7% in 2026 and 2027, respectively” for Australia’s economy, noting similar global pressures affecting developed economies.

The consensus suggests Americans should brace for continued price pressure through at least mid-2026, with relief dependent on tariff policy evolution and whether businesses complete their price adjustments.

Political Manoeuvring: Trump’s Affordability Push

Facing mounting political pressure, Trump has unveiled several initiatives aimed at demonstrating action on cost-of-living concerns:

- Credit card interest rate cap: Trump proposed a temporary one-year limit of 10% on credit card interest rates, targeting fees that often exceed 20%. The proposal revives a campaign promise but lacks implementation details or clear enforcement mechanisms.

- Housing affordability measures: The administration announced plans to ban large Wall Street banks from purchasing single-family homes, arguing “people live in homes, not corporations.” Trump also pushed for regulatory changes to lower mortgage barriers for middle-class families.

- Tax relief: The “One Big Beautiful Bill” tax cuts are taking effect, with administration officials promising larger refunds and lower paycheck deductions for millions of Americans.

These moves represent reactive policymaking aimed at blunting Democratic attacks on affordability. However, critics note they don’t address underlying inflationary pressures or the tariff regime driving future price increases.

Cassandra Goldie, chief executive at ACOSS, captured the sentiment of many struggling households: “Raising the cash rate has dramatically increased financial stress among people on low and modest incomes. It’s time to finally give people some desperately needed relief.”

Global Context: How Other Nations Compare

While US inflation remains stubbornly above target, Australia and New Zealand offer contrasting economic pictures. Both nations successfully reduced inflation below 3%, but their paths diverged sharply.

Australia avoided recession entirely, recording steady quarterly growth with record employment levels. The Reserve Bank of Australia held rates steady longer before beginning cuts in February 2025, prioritising employment alongside price stability.

New Zealand entered technical recession with six consecutive months of negative growth. The Reserve Bank of New Zealand raised rates earlier and higher than Australia, peaking at 5.5% compared to the RBA’s 4.35%. The more aggressive approach crushed inflation but devastated employment, with 32,000 fewer jobs than a year prior.

The divergent outcomes illustrate how central banks navigate the inflation-employment trade-off. Australia’s more gradual approach preserved jobs while still bringing prices under control. New Zealand’s shock therapy achieved faster inflation reduction but at severe economic cost.

Looking Ahead: Key Factors to Watch

Several variables will determine whether US inflation finally breaks below the Fed’s 2% target in 2026:

- Tariff policy evolution: Will Trump maintain current tariff levels, escalate further, or quietly scale back to ease political pressure? Business pricing decisions hinge on this uncertainty.

- Labour market strength: Continued job growth supports household incomes but also risks wage-driven inflation if unemployment falls further.

- Energy prices: Oil market dynamics, influenced by geopolitics and production decisions, significantly impact headline inflation readings.

- Housing market: Shelter costs constitute roughly one-third of CPI. Progress toward normal rent growth is essential for overall inflation reduction.

- Federal Reserve independence: Perceptions that Trump is pressuring the Fed could undermine inflation expectations, making price stability harder to achieve.

Economists emphasise the Fed’s credibility remains paramount. If markets believe political influence is compromising monetary policy, that alone could fuel inflation regardless of actual rate decisions.

Also Read: Why Niobium Could Be Australia’s Next Critical Minerals Goldmine

Final Analysis

The December CPI report delivered a sobering message: inflation’s decline has stalled, and the path to the Fed’s 2% target looks increasingly uncertain. Core inflation’s drop to a four-year low offers hope, but headline figures remain stubbornly elevated.

Trump faces a political tightrope walk. His tariff policies threaten to reignite price pressures just as voters head to 2026 midterm polls. The administration’s affordability initiatives may provide optical relief, but they don’t address underlying structural forces driving costs higher.

For American households, the reality is clear. After years of accumulated inflation, prices remain painfully elevated compared to pre-pandemic levels. A slower rate of increase doesn’t translate to actual price relief, leaving many families feeling the squeeze despite economic growth and low unemployment.

The Fed’s pause on rate cuts reflects these tensions. Powell and colleagues recognise they cannot solve affordability concerns through monetary policy alone, particularly when fiscal policy choices actively push prices higher through tariffs.

As 2026 progresses, inflation’s trajectory will depend less on the latest monthly data points and more on policy choices and economic fundamentals. Trump’s handling of the tariff regime, the Fed’s credibility maintenance, and global economic conditions will all play crucial roles.

For now, Americans must navigate an economy where inflation persists above target, interest rates remain elevated by historical standards, and political rhetoric clashes with economic reality. The December CPI report suggests that navigation will remain challenging for months to come.