Australia digs up more lithium than any country on Earth. It ranks among the top five producers of cobalt, rare earths, and manganese. Yet here’s the catch: over 90% of this treasure gets shipped straight to Chinese refineries.

The nation sits on a goldmine that powers electric vehicles, wind turbines, and defence systems worldwide. But it captures only a fraction of the value chain. This disconnect between geological wealth and economic leverage defines Australia’s critical minerals paradox.

Recent developments suggest the country might be at a turning point. The question is whether this moment represents genuine transformation or just another missed opportunity.

The Strategic Minerals Australia Supplies to the World

Critical minerals aren’t actually rare in the traditional sense. The term describes materials essential for modern technology, national security, and clean energy transitions that face supply chain vulnerabilities.

Australia’s official list includes 31 minerals. The most strategically important for the energy transition include lithium, nickel, cobalt, graphite, rare earths, and copper. These materials form the backbone of renewable energy infrastructure and electric vehicles.

Lithium enables rechargeable batteries. Rare earths create powerful magnets for wind turbines and EVs. Cobalt and nickel enhance battery performance. Graphite serves as a critical component in battery anodes. Copper connects everything together.

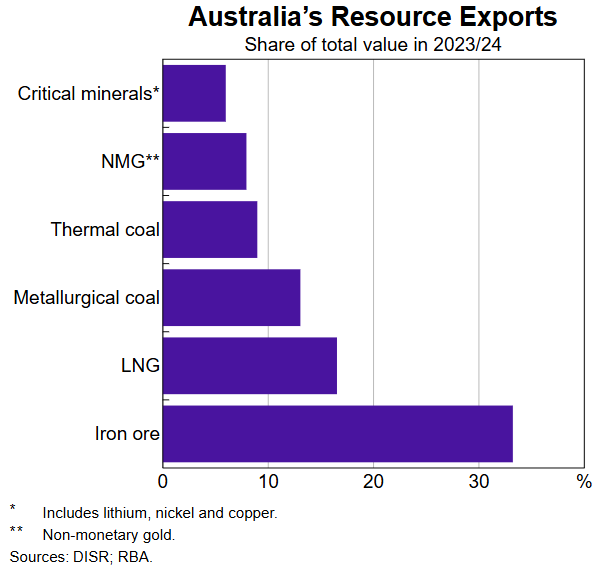

The Reserve Bank of Australia notes that critical mineral exports currently comprise just 6% of the nation’s resource exports. However, projections suggest this could reach 10% by 2030 as global demand surges.

Australia Resource Exports

Record Investment Signals Major Shift

October 2025 marked a watershed moment for Australia’s critical minerals sector. The United States and Australia signed a framework committing approximately USD 8.5 billion to critical minerals projects over the next six months.

This represents the largest critical minerals partnership in Western history. The US Export-Import Bank issued Letters of Interest totalling over USD 2.2 billion across seven strategic Australian developments. Projects include rare earth separation facilities, graphite purification plants, and titanium refinement operations.

The European Investment Bank followed suit, exploring significant investment opportunities across Australia’s critical minerals landscape. This dual interest from major Western economies reflects growing urgency around supply chain security.

These investments target a specific vulnerability. China currently controls over 90% of rare earth processing globally and refines the bulk of Australia’s lithium output. Beijing’s dominance extends beyond mining to the midstream processing that transforms raw ore into battery-grade chemicals.

The strategic risk became apparent when China recently tightened export restrictions on critical minerals. This move prompted immediate concern from Western governments reliant on Chinese processing capacity.

The Processing Gap That Costs Billions

Australia excels at digging things out of the ground. The country’s mining expertise, technical capability, and geological surveys remain world-class. What it lacks is downstream processing capacity.

Consider lithium. Australia produces more lithium than any other nation. Yet the country processes less than 1% of global lithium into battery-grade chemicals. The economic implications are stark.

Raw lithium concentrate sells for a fraction of the price commanded by processed lithium hydroxide or lithium carbonate. This value gap represents billions in forgone revenue annually. The same pattern repeats across rare earths, cobalt, and other critical minerals.

The RBA’s October bulletin identified several factors constraining processing development:

- High input costs: Energy expenses in Australia significantly exceed those in competitor nations like Indonesia and Malaysia. Electricity represents a major operational cost for refineries, which require substantial power for high-temperature chemical processes.

- Workforce shortages: Downstream processing operations require specialised skillsets in chemical engineering, metallurgy, and advanced manufacturing. These capabilities remain scarce in the Australian labour market.

- Long development timelines: Critical mineral projects typically require 10-15 years from exploration to production. Even brownfield expansions need 2-4 years to reach commercial operation.

- Environmental approval complexity: New mining projects face 3-5 year approval processes. Some projects experience substantially longer timelines due to complex consultation requirements and environmental considerations.

- Capital intensity: Lithium refining facilities typically require 2-3 years for construction once approvals are obtained, with capital costs reaching hundreds of millions for a single facility.

Government Policy Response Accelerates

Recognition of these challenges has prompted a wave of policy initiatives. The Australian Government’s Critical Minerals Strategy 2023-2030 sets out a framework for growing the sector beyond simple extraction.

Key policy measures include:

- The Critical Minerals Facility provides AUD 4 billion in financing capacity through Export Finance Australia. This facility aims to support projects aligned with strategic priorities.

- The Critical Minerals Production Tax Incentive offers a 10% production credit on relevant processing and refining costs. This incentive applies for up to 10 years per project, covering production between 2027-28 and 2039-40.

- The Major Projects Facilitation Agency assists developers with projects exceeding AUD 20 million, streamlining regulatory pathways.

- Geoscience Australia received AUD 566.1 million over 10 years from 2024-25 to deliver exploration data, maps, and tools for the resources industry.

- The Critical Minerals Strategic Reserve announced in 2025 creates buffer stocks for high-risk materials. This provides resilience against short-term supply disruptions while signalling long-term government commitment.

These policies form a strong foundation. Whether they prove sufficient to overcome Australia’s comparative disadvantages in processing remains an open question.

Price Volatility Creates Investment Uncertainty

Recent market dynamics illustrate the sector’s cyclical challenges. In 2021, accelerated EV adoption globally contributed to sharp increases in critical mineral prices. Lithium prices soared. Nickel followed.

Producers responded by scaling up investment and supply faster than anticipated. By 2024, increased supply overwhelmed demand expectations. Prices collapsed. This correction had immediate consequences.

Several late-stage lithium projects were delayed in 2024. Operating mines postponed investment plans, waiting for sustained price recovery. Production at facilities including BHP’s Nickel West operation and Mineral Resources’ Bald Hill lithium mine was paused due to profitability concerns.

BHP’s Nickel West operation

This volatility creates a chicken-and-egg problem. Refineries require long-term feedstock agreements at viable prices. Miners need offtake certainty to justify development. Price uncertainty makes both parties hesitant to commit capital.

The recent US-Australia framework addresses this through price floors and offtake guarantees. These mechanisms aim to de-risk investment decisions that would otherwise stall due to commodity price uncertainty.

The Window May Be Closing

Industry analysts warn that a two-year window exists before global battery supply chains solidify. After that point, establishing new processing relationships becomes substantially harder.

China hasn’t stood still. State-backed companies continue acquiring critical mineral assets globally. In May 2025, Shenghe Resources announced a binding agreement to acquire Peak Rare Earths’ Tanzanian project for AUD 158 million, nearly 200% above the market price.

This aggressive acquisition strategy aims to maintain China’s processing dominance. Beijing understands that controlling midstream processing provides more leverage than owning mines.

Western efforts to diversify supply chains face formidable challenges. Building alternative processing capacity requires massive capital investment, technical expertise, and time. Even with accelerated timelines, new refineries won’t reach full production for years.

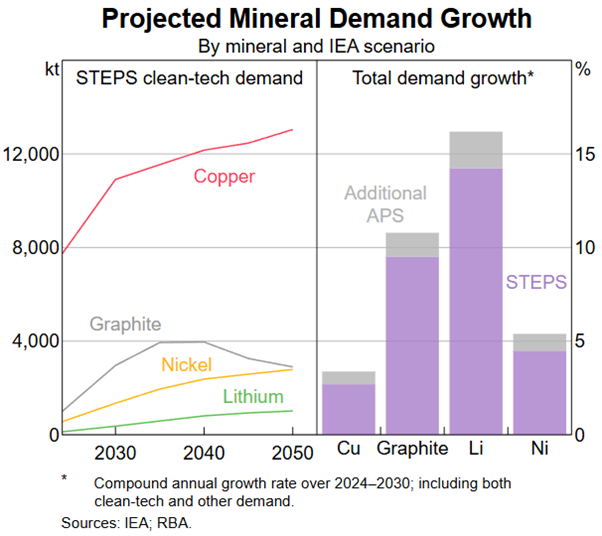

The International Energy Agency projects potential supply shortfalls for copper and lithium by 2035 based on current project pipelines. These projected shortfalls could drive prices higher, improving investment economics. Alternatively, they might indicate that current energy transition scenarios are unrealistic given supply constraints.

Projected Mineral Demand Growth

Success Stories Emerge Despite Obstacles

Despite the challenges, several projects demonstrate processing can work in Australia.

Arafura Resources‘ Nolans Project received AUD 840 million in federal funding. This combined rare earths mine and refinery will pioneer rare earth separation technology in Australia. The project expects to supply approximately 4% of global demand for neodymium and praseodymium beginning in 2032.

Iluka Resources‘ Eneabba Rare Earths Refinery in Western Australia secured a AUD 1.25 billion government loan. The facility will produce separated oxides including neodymium, praseodymium, dysprosium, and terbium. Commissioning is expected in 2026.

Lynas Corporation achieved a historic milestone in May 2025, becoming the first company outside China to produce commercial quantities of dysprosium oxide at its Malaysian facility.

These projects required substantial government support to proceed. Their success or failure will shape the viability of future processing investments.

What Comes Next

Australia’s critical minerals sector stands at a crossroads. The geological endowment is undeniable. Global demand projections support long-term optimism. Strategic imperatives favour diversified supply chains away from China.

Yet success isn’t guaranteed. High costs, workforce constraints, and entrenched competition create formidable barriers. Government support provides necessary but insufficient conditions for transformation.

The next five years will determine whether Australia captures more value from its mineral wealth or continues shipping raw materials for processing elsewhere. Current momentum suggests progress, but the gap between ambition and execution remains wide.

For investors, the sector offers leveraged exposure to global decarbonisation trends with geopolitical tailwinds. For policymakers, it represents an opportunity to reshape Australia’s economic future beyond fossil fuel exports.

The critical question isn’t whether Australia has the resources. It’s whether the nation can build the processing capacity before the window closes.

Also Read: Thousands of Australians Paid Back Centrelink Debts They Never Actually Owed

Frequently Asked Questions

Q: What are critical minerals and why do they matter?

A: Critical minerals are materials essential for modern technologies, clean energy systems, and national security with vulnerable supply chains. They power electric vehicles, renewable energy infrastructure, smartphones, and defence systems. Australia possesses significant deposits of lithium, rare earths, cobalt, and other strategic minerals.

Q: Why doesn’t Australia process its own critical minerals?

A: Australia faces high energy costs, workforce shortages, long approval timelines, and intense competition from established Chinese processors. Processing requires specialised chemical engineering expertise and substantial capital investment. Government policies now aim to overcome these barriers through tax incentives and financing support.

Q: How large is the US-Australia critical minerals deal?

A: The October 2025 framework commits approximately USD 8.5 billion to critical minerals projects over six months. The US Export-Import Bank issued Letters of Interest totalling over USD 2.2 billion across seven strategic Australian developments.

Q: What percentage of global lithium processing does China control?

A: China refines over 90% of Australia’s lithium output and controls approximately 85% of global lithium processing capacity. This dominance extends across most critical mineral processing, creating strategic vulnerabilities for Western supply chains.

Q: What’s the timeline for new critical minerals projects in Australia?

A: Typical progression from discovery to production for new mining projects ranges from 10-15 years. Brownfield expansions of existing operations can achieve production within 2-4 years. Lithium refining facilities require 2-3 years for construction once approvals are obtained.

Q: Are critical mineral investments risky?

A: The sector faces commodity price volatility, long development timelines, regulatory complexity, and established competition. Recent price collapses paused several projects. However, strategic government support and growing global demand create favourable long-term conditions. Investors should evaluate management capabilities, project economics, and strategic positioning carefully.