The Westpac Corporation (WBC: ASX) has provided an update on the Business and Wealth division’s performance for the first half of 2025, with clear progress evident.

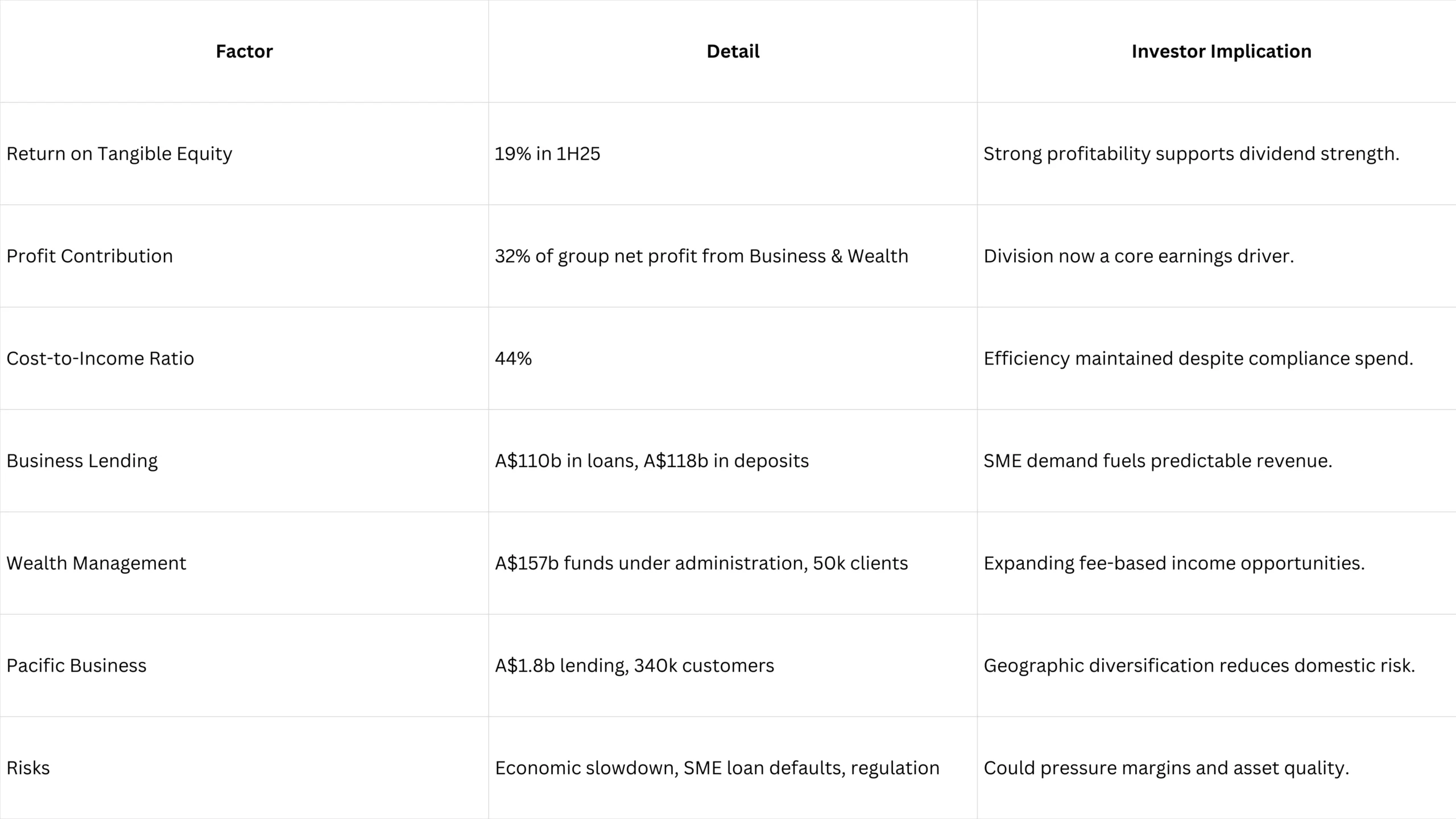

A return on tangible equity (ROTE) of 19% was achieved, which strongly supports the division’s profitability for the entire group.

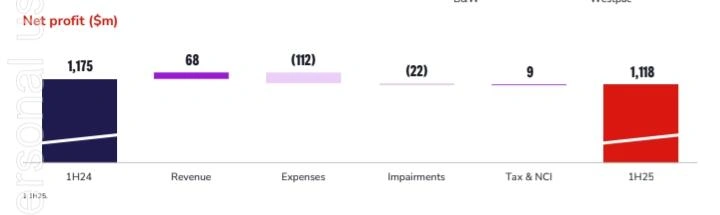

Westpac’s net profit increased by 32%, further boosting the division’s weight in overall earnings. A cost-to-income ratio of 44% showed compliance and technology investments paid off, contributing to operating efficiency.

The results assume greater significance in the context of increased competition in the ASX financial sector.

While competitors reduce margins, Westpac’s ability to maintain solid returns remains comforting for investors. It demonstrates that the Westpac Business and Wealth division is being strategically developed, not merely maintained.

Westpac Business Banking Update: Loans, Deposits & SME Lending

Investors’ Takeaway

What is driving growth in Westpac’s business banking?

Business banking remains the core driver of Westpac’s overall performance. Net loans hit A$110 billion, driven by strong demand from small and medium-sized enterprises.

Deposits rose to A$118 billion, signalling customer confidence in Westpac’s balance sheet. Westpac maintained its lead in commercial and SME lending, while also securing second place in multi-financial institution relationships and third place in small business lending.

These standings illustrate Westpac’s strong position within Australia’s corporate finance sector.Westpac’s digital initiatives, along with lending process improvements, are worthy of mention.

They have shortened response times for SMEs, which is essential for preserving client trust. Westpac’s business update highlighted more hiring in frontline banking, indicating a continued effort to strengthen client engagements.

How is the wealth segment expanding?

Westpac’s strategic focus on wealth management means funds under administration (FUA) now stand at A$157 billion, bolstering the bank’s position within the competitive Australian wealth market. Furthermore, Westpac Private Bank’s clientele has expanded to 50,000, accentuating its reach among high-net-worth clients.

The accelerated growth of the Wealth segment is attributable to increasing demand for retirement solutions, superannuation, and investment diversification products. Westpac leverages the country’s ageing population, as continued investments in wealth products persist.

The Westpac business update issued information regarding the investments committed to digital advice and customer platforms. Digital advice and customer platform investments are being modernised to keep pace with the rising expectations of digital investors, while preserving high-touch private banking services. The ability to offer both sets of services is a strength when compared to smaller wealth managers.

Pacific business supports regional diversification

Even though Westpac’s Pacific operations are small, they still assist in diversifying the group’s earnings margins. Westpac’s customer base grew to 340,000 clients across regional markets with a lending amount of A$1.8 billion.

Having operations in the Pacific region gives Westpac a layer of protection from shocks stemming from the Australian market. Having business in the regional economies, especially dealing with trade and remittances, gives the company other businesses to earn from.

The Pacific operations remain profitable despite currency issues. This bolsters Westpac’s image as a regional bank with cross-border services.

Westpac share price outlook strengthens

Ever since the update, Westpac shares have attracted new investors. Investors appear to associate the 19% ROTE and growing business lending with an ability to withstand setbacks.

Westpac benefits from a well-diversified earnings base, which is reflected in the fact that 32% of the group’s profits come from Business and Wealth. Westpac is still one of the most watched stocks on the ASX financial sector index among the Australian banks’ blue-chip group.

Further expansion in SME lending and wealth management, as noted by analysts, could be the reason for medium-term gains. The outlook for Westpac shares has been positively impacted by the speculation that its dividends will remain stable, supported by strong underlying earnings.

Investors tracking WBC ASX shares see the update as a positive step toward long-term value creation.

Investors weigh opportunities and risks

Although sentiment is in the green, there is caution with respect to the macroeconomic concerns. There is the risk of SME loan defaults, to which loan funding costs, regulatory oversight, and loan performance could shift. Investor outlook:

- Expanding SME lending supports stable income streams.

- Fee income diversification is supported by wealth growth.

- A 19% ROTE points to strong dividend capacity.

- A cost-to-income ratio of 44% indicates operational efficiency.

- Risks include decelerating domestic growth and regulatory tightening.

Fundamentals are consistent with the steady sector-relative performance, so the outlook on the Westpac share price is prudent.

Also Read: ASX Short Sale Trends – Week 36: Who’s Being Shorted & Who’s Gaining or Falling

FAQs

- What was Westpac’s return on tangible equity in 1H25?

Westpac announced a 19% ROTE for its Business and Wealth division for the first half of 2025.

- What were the loan book and deposit balances of Westpac’s Business division?

The division posted A$110 billion in loans and A$118 billion in deposits.

- What is the value of funds under administration in Westpac’s Wealth segment?

Funds under administration hit A$157 billion in 1H25.

- How does Westpac rank in SME and business banking?

It is the top-ranked institution in commercial and SME lending throughout Australia.