The United States has extended a strategic invitation to Australia and India to join G7 discussions on critical minerals, marking a decisive shift in global supply chain policy. The move comes as Western nations scramble to reduce dependence on China’s stranglehold over rare earth minerals essential for defence, clean energy, and advanced technology.

US Treasury Secretary Scott Bessent confirmed the development, signalling Washington’s intent to build a robust alternative supply network. The decision positions Australia as a key partner in securing minerals that power everything from electric vehicles to fighter jets.

Why Australia and India Matter for Critical Minerals Security

Australia’s inclusion in the G7 critical minerals partnership stems from its massive reserves of lithium, rare earths, and other strategic resources. The country ranks among the world’s top producers of lithium and holds significant deposits of cobalt, graphite, and nickel.

India’s invitation reflects its growing manufacturing base and commitment to processing critical minerals domestically. The South Asian giant has been actively investing in refining capacity to support its clean energy ambitions and electronics industry.

Key factors driving the partnership:

- Australia produces approximately 52% of the world’s lithium supply

- India aims to process 25% of global rare earth minerals by 2030

- Both nations maintain strong democratic governance and regulatory transparency

- Geographic diversification reduces single-source dependency risks

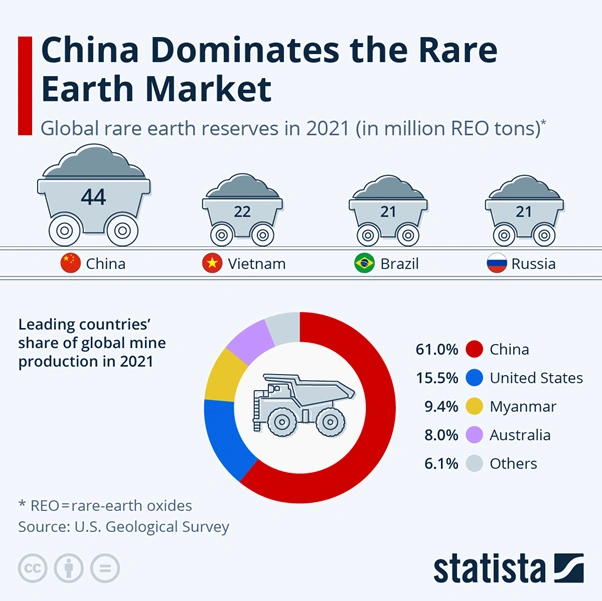

The collaboration directly challenges China’s dominance, which currently controls over 70% of rare earth processing capacity globally.

China’s dominance in the rare earth market [Statista]

G7 Framework: Building a Western-Led Supply Chain

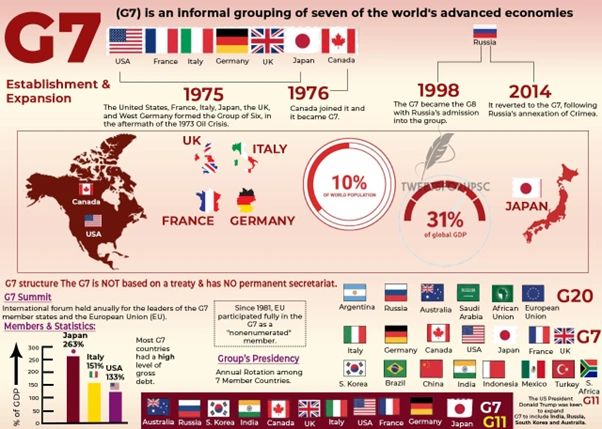

The G7 critical minerals initiative launched in 2023 to coordinate investment, technology sharing, and supply agreements among member states. Originally comprising the US, Canada, Japan, Germany, France, Italy, and the UK, the group now expands its reach into the Indo-Pacific.

Australia’s existing bilateral agreements with the US under the Australia-United States Ministerial Consultations (AUSMIN) provide a foundation for deeper cooperation. The countries already share defence technology and intelligence, making minerals collaboration a natural extension.

India’s participation adds manufacturing muscle and a massive domestic market. The country’s processing infrastructure development could transform raw materials from Australian mines into finished products without routing through Chinese facilities.

Treasury officials indicated the expanded partnership would facilitate:

- Joint exploration and mining ventures

- Coordinated stockpiling strategies

- Technology transfer for mineral processing

- Financing mechanisms for critical infrastructure

- Common standards for environmental and labour practices

Seven advanced economies coordinating on global economic, political, and strategic challenges [@factsforupsc on X]

Market Implications: Rare Earth Minerals Supply Chain Shift

The rare earth minerals supply chain has been a geopolitical flashpoint for years. China’s quasi-monopoly has allowed Beijing to weaponise access during trade disputes, most notably restricting exports to Japan in 2010.

Western nations recognise this vulnerability acutely. Defence systems like F-35 fighter jets require rare earth magnets. Wind turbines and electric vehicle motors depend on neodymium and dysprosium. Solar panels need tellurium and indium.

Australia’s critical minerals sector stands to benefit substantially:

- Lynas Rare Earths (ASX: LYC) operates the sole Western rare earths processing facility outside China

- Pilbara Minerals (ASX: PLS) supplies lithium to major battery manufacturers globally

- Mineral Resources (ASX: MIN) has expanded production capacity to meet surging demand

Industry analysts project global critical minerals demand could triple by 2030 as clean energy transitions accelerate. The G7 partnership aims to capture this growth opportunity while insulating member nations from supply disruptions.

Australia’s lithium production capacity positions the nation as a cornerstone of the G7 critical minerals strategy. [Statista]

Strategic Timing: Trade Tensions and Tech Competition

The invitation arrives amid heightened US-China tensions over technology and trade. Washington has implemented export controls on advanced semiconductors and manufacturing equipment to China. Beijing responded by restricting exports of gallium and germanium, both critical for chip production.

Australia’s relationship with China remains complex. Beijing imposed informal trade sanctions on Australian coal, wine, and barley starting in 2020, though many restrictions have since eased. Critical minerals represent a sector where Australia can leverage its natural advantages while maintaining economic pragmatism.

India’s participation balances concerns about Russian energy dependence with Western alignment on technology standards. New Delhi has positioned itself as a reliable partner for democratic nations seeking to diversify supply chains.

The expanded G7 critical minerals group sends a clear message: Western nations are serious about building alternative supply networks that bypass authoritarian control points.

What Officials Are Saying

Treasury Secretary Bessent emphasised the strategic importance of the partnership during his announcement. He noted that critical minerals are “the building blocks of the 21st-century economy” and that securing diverse supply sources is “a matter of national security.”

Australian Trade Minister Don Farrell welcomed the development, stating that the country’s minerals sector is “ready to meet the challenge of responsible resource development.” He highlighted Australia’s commitment to high environmental standards and indigenous consultation processes.

India’s Minister of Mines and Metals Pralhad Joshi called the invitation “recognition of India’s growing capabilities in mineral processing and value addition.” He pledged to accelerate refining capacity development and establish strategic reserves.

Investor Outlook: Opportunities in Critical Minerals Sector

Australian mining companies with critical minerals exposure are positioned for sustained growth as G7 nations commit funding and policy support. The partnership is expected to accelerate project approvals, facilitate financing, and guarantee off-take agreements.

Investors should watch for:

- Government-backed loan guarantees for mining projects

- Joint venture announcements between Australian and US/Indian firms

- Technology collaboration agreements for processing innovation

- Infrastructure investments in ports and rail serving mining regions

- ESG frameworks are becoming prerequisites for partnership participation

The shift in global supply chain strategy represents a multi-decade trend rather than a short-term policy fluctuation. Companies that establish early positions in the expanded G7 framework stand to capture significant value.

However, challenges remain. Developing new mines takes 7-10 years from discovery to production. Processing capacity requires substantial capital investment and technical expertise. Environmental approvals in democratic nations involve extensive consultation periods.

Despite these hurdles, the strategic imperative driving the G7 critical minerals partnership ensures policy support will persist across election cycles. National security concerns transcend partisan politics.

Looking Ahead: The Road to Supply Chain Sovereignty

The expanded partnership faces immediate tasks including establishing governance structures, defining membership criteria, and setting investment priorities. Working groups will need to coordinate across seven original G7 members plus Australia and India, each with distinct regulatory frameworks and commercial interests.

Practical cooperation could include:

- Creating a critical minerals investment fund pool

- Standardising environmental and social governance criteria

- Establishing commodity price stabilisation mechanisms

- Coordinating strategic reserves and emergency protocols

- Sharing geological survey data and exploration technology

Australia’s geological survey agencies possess world-leading expertise in mineral mapping and assessment. India’s rapidly expanding manufacturing sector offers downstream integration opportunities. The US brings financial resources and military procurement commitments.

Japan and South Korea, though not formal G7 members, will likely participate given their advanced manufacturing sectors and complete dependence on imported raw materials.

The partnership’s success ultimately depends on execution. Previous initiatives have foundered on insufficient funding, conflicting national interests, and private sector hesitation to invest without guaranteed returns.

This time appears different. The Russia-Ukraine conflict demonstrated how resource dependence creates strategic vulnerabilities. China’s willingness to restrict critical exports during disputes reinforced the lesson. Western nations finally recognise that supply chain security deserves the same attention as military capabilities.

Also Read: Meta’s Massive Nuclear Bet Sends Oklo Stock Rocketing as Tech Giant Chases AI Power

The Bottom Line

Australia’s invitation to join G7 critical minerals discussions represents a watershed moment for the nation’s resources sector. The partnership elevates critical minerals from a trade issue to a strategic imperative backed by the world’s largest economies.

For Australian miners, processors, and technology companies, the expanded G7 framework offers unprecedented opportunities. Government backing, guaranteed markets, and coordinated investment remove many traditional barriers to project development.

For global markets, the initiative signals a fundamental restructuring of mineral supply chains. China’s dominance will face sustained, coordinated challenge from nations with comparable resources, superior technology, and deeper capital markets.

The rare earth minerals supply chain stands at an inflection point. The next decade will determine whether Western nations successfully diversify away from Chinese dependency or whether Beijing’s first-mover advantage proves insurmountable.

Australia’s geological endowment and democratic governance position the country as an indispensable partner. India’s processing ambitions and massive domestic market add scale. Together with G7 members, they possess the resources, technology, and political will to reshape global mineral supply architecture.

The question is no longer whether change will come, but how quickly the new system can be built.